The GOP House Tax Bill Implications

Yesterday we received the first details on tax reform as the House Republicans unveiled their plan. To residents of high-tax states (including your blogger in NJ) it looks like the Republican Tax Hike Plan. Putting aside the impact on some individuals, our thoughts on the investment consequences are as follows:

MLP investors should benefit, because the structure is untouched and we interpret the plan as allowing the 25% business owner pass-through rate to apply to taxable income, rather than ordinary income tax rates. This is more valuable the higher your income. Around 80% of MLP distributions are tax-deferred, and many long-time MLP holders are familiar with receiving a large tax bill when they sell, since taxes on distributions that were deferred are owed at that point. Former Kinder Morgan Partners (KMP) investors are acutely aware of the unwelcome tax bill they received back in 2014 when Kinder Morgan Inc (KMI) acquired KMP’s assets, simplifying their corporate structure but triggering the above mentioned tax event. Under the House proposal, if that was to happen in 2018 the KMP tax bill would be based on the 25% pass-through rate. This will be a consideration for those MLP businesses considering simplification transactions in which the GP buys the MLP, since the acquiring GP won’t have to offer as much consideration to the MLP holders given the likely reduced tax burden.

We didn’t see anything else that was negative for MLPs, notwithstanding the weakness in the sector following release of the plan.

The other items related to corporate taxes affect most corporations, not just those in energy infrastructure. The lower tax rate is obviously good – how good depends on your tax rate. Energy infrastructure businesses generally pay a lower rate than 35% because they have substantial non-cash depreciation charges. By contract, companies in the Consumer Staples sector (which figures prominently in our Low Vol strategies) are generally paying corporate taxes at close to the 35% rate. Those taxed at higher rates will obviously benefit more from a new, lower 20% corporate rate.

Interest expense is capped at 30% of EBITDA (Earnings Before Interest, Taxes, Depreciation and Amortization). So a company with $1MM of EBITDA could deduct up to $300K of interest expense. Assuming they were borrowing at 5%, this would allow them to borrow up to $6MM (i.e. 5% interest on $6MM is $300K) and still deduct the expense. A Debt:EBITDA leverage ratio of 6:1, as in this example, is higher than most energy infrastructure businesses, where 4X-5X is more typical and is coming down. Clearly, if rates were higher this would reduce the amount of tax-deductible debt. A 10% cost of borrowing would impose a 3X Debt:EBITDA tax-deductible leverage limit – probably not a bad idea at such high rates anyway. Faster depreciation schedules may further reduce taxes for some companies, and energy infrastructure businesses are likely beneficiaries.

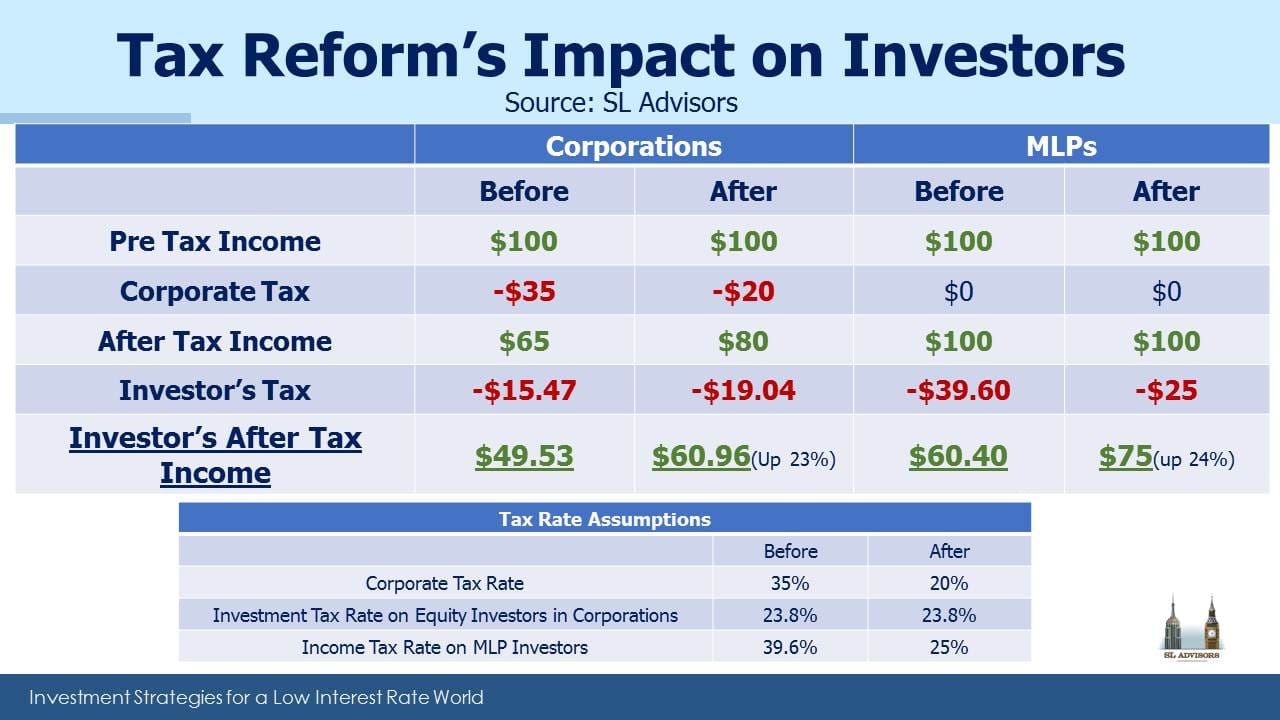

In April we offered our thoughts on proposed tax reform (see MLPs and Tax Reform). Below is an updated table comparing the impact on energy infrastructure C-corps and MLPs. Tax reform is beneficial to both classes of investment.

The lower corporate tax rate on its own reduces the tax advantage of MLPs versus C-corps. But the pass-through 25% tax rate on distributions when taxable is an improvement for investors. So we don’t see anything here that renders the MLP structure less attractive. C-corps in the energy sector today aren’t anywhere near the 35% rate. Since taxes on investment income (qualified dividends and capital gains) aren’t changing, a lightly taxed C-corp might be less tax-efficient (since its dividends are taxable) than an MLP where the investor can benefit more than the corporation from the tax-deductible depreciation. In short, MLPs can still be advantageous.

The main problem for the structure this year has been an evident unwillingness of traditional MLP investors to provide growth capital (see The Changing MLP Investor and More on the Changing MLP Investor). Maybe the more attractive tax treatment to investors will help.

We are invested in KMI

Important Disclosures

The information provided is for informational purposes only and investors should determine for themselves whether a particular service, security or product is suitable for their investment needs. The information contained herein is not complete, may not be current, is subject to change, and is subject to, and qualified in its entirety by, the more complete disclosures, risk factors and other terms that are contained in the disclosure, prospectus, and offering. Certain information herein has been obtained from third party sources and, although believed to be reliable, has not been independently verified and its accuracy or completeness cannot be guaranteed. No representation is made with respect to the accuracy, completeness or timeliness of this information. Nothing provided on this site constitutes tax advice. Individuals should seek the advice of their own tax advisor for specific information regarding tax consequences of investments. Investments in securities entail risk and are not suitable for all investors. This site is not a recommendation nor an offer to sell (or solicitation of an offer to buy) securities in the United States or in any other jurisdiction.

References to indexes and benchmarks are hypothetical illustrations of aggregate returns and do not reflect the performance of any actual investment. Investors cannot invest in an index and do not reflect the deduction of the advisor’s fees or other trading expenses. There can be no assurance that current investments will be profitable. Actual realized returns will depend on, among other factors, the value of assets and market conditions at the time of disposition, any related transaction costs, and the timing of the purchase. Indexes and benchmarks may not directly correlate or only partially relate to portfolios managed by SL Advisors as they have different underlying investments and may use different strategies or have different objectives than portfolios managed by SL Advisors (e.g. The Alerian index is a group MLP securities in the oil and gas industries. Portfolios may not include the same investments that are included in the Alerian Index. The S & P Index does not directly relate to investment strategies managed by SL Advisers.)

This site may contain forward-looking statements relating to the objectives, opportunities, and the future performance of the U.S. market generally. Forward-looking statements may be identified by the use of such words as; “believe,” “expect,” “anticipate,” “should,” “planned,” “estimated,” “potential” and other similar terms. Examples of forward-looking statements include, but are not limited to, estimates with respect to financial condition, results of operations, and success or lack of success of any particular investment strategy. All are subject to various factors, including, but not limited to general and local economic conditions, changing levels of competition within certain industries and markets, changes in interest rates, changes in legislation or regulation, and other economic, competitive, governmental, regulatory and technological factors affecting a portfolio’s operations that could cause actual results to differ materially from projected results. Such statements are forward-looking in nature and involves a number of known and unknown risks, uncertainties and other factors, and accordingly, actual results may differ materially from those reflected or contemplated in such forward-looking statements. Prospective investors are cautioned not to place undue reliance on any forward-looking statements or examples. None of SL Advisors LLC or any of its affiliates or principals nor any other individual or entity assumes any obligation to update any forward-looking statements as a result of new information, subsequent events or any other circumstances. All statements made herein speak only as of the date that they were made. r

Certain hyperlinks or referenced websites on the Site, if any, are for your convenience and forward you to third parties’ websites, which generally are recognized by their top level domain name. Any descriptions of, references to, or links to other products, publications or services does not constitute an endorsement, authorization, sponsorship by or affiliation with SL Advisors LLC with respect to any linked site or its sponsor, unless expressly stated by SL Advisors LLC. Any such information, products or sites have not necessarily been reviewed by SL Advisors LLC and are provided or maintained by third parties over whom SL Advisors LLC exercise no control. SL Advisors LLC expressly disclaim any responsibility for the content, the accuracy of the information, and/or quality of products or services provided by or advertised on these third-party sites.

All investment strategies have the potential for profit or loss. Different types of investments involve varying degrees of risk, and there can be no assurance that any specific investment will be suitable or profitable for a client’s investment portfolio.

Past performance of the American Energy Independence Index is not indicative of future returns.

Typo on your table. $15 should be $25 for MLP taxes paid.

But really outstanding article Simon. Why you are the best blog writer on the MLP space, bar none.

Many thanks for your kind feedback, and also for spotting the typo.