It’s Not Easy Being Green

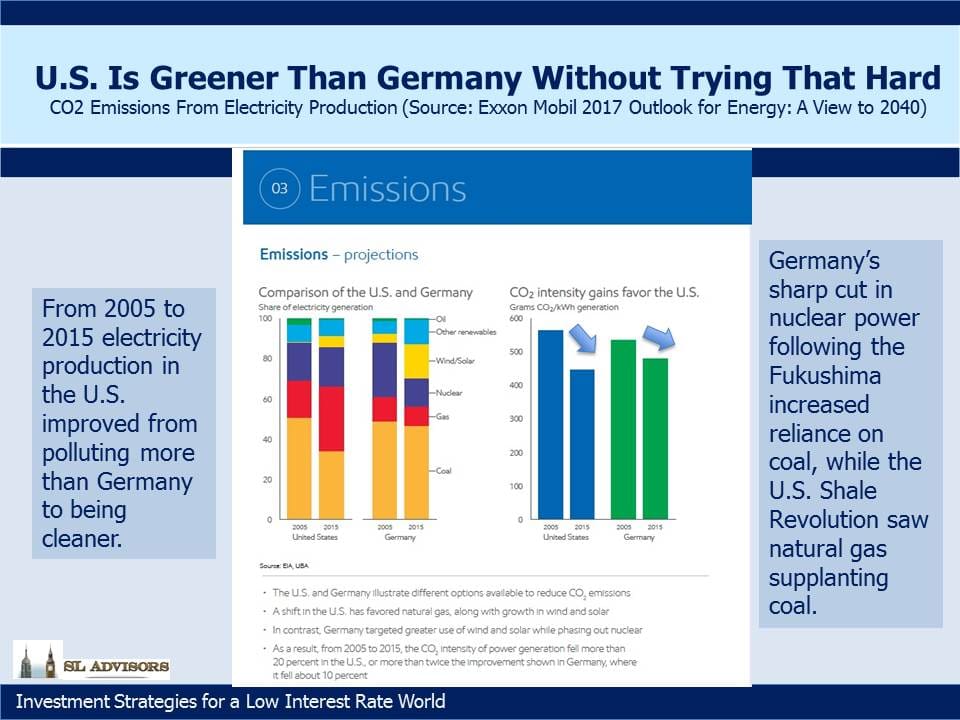

Recently in A Few Thoughts on Long Term Energy Use we included the striking chart shown again below comparing CO2 emissions from power generation in the U.S. and Germany. It elicited quite a few comments from readers because it showed that Germany is now lagging behind the U.S. on this metric. Germany has set out to be a global leader in the use of renewables. By 2050 they aim to generate 80% of their electricity from renewables and to cut their greenhouse gas emissions by up to 95%. Until 2015, Germany had the world’s largest installed solar capacity, which reflects quite a commitment because there are plenty of sunnier places on the planet than northern Europe. The push to renewables (dubbed “Energiewende”, or Energy Transition, in German) enjoys widespread public support, which extends as far as surcharges on household electricity. German consumers pay among the highest prices for electricity in the world, largely due to taxes and other charges in support of renewables.

By contrast, the U.S. has a more ambivalent view. Strong opinions are not hard to find on both sides of the debate over whether global warming is man-made. Some states, notably California, have implemented policies to reduce emissions as they became frustrated with inaction by the U.S. Congress. President Obama sought to impose stricter regulation on emissions through executive actions, but President Trump has said the U.S. will withdraw from the Paris Agreement on Climate Change. American public opinion doesn’t reflect the same concern about the issue as Germany. And yet, measured by CO2 output per unit of electricity, we’re doing better. Lower U.S. emissions come with cheaper electricity which stimulates economic growth.

The Shale revolution is certainly part of the reason. Abundant, cheap, clean-burning natural gas has been steadily replacing dirtier coal as the fuel of choice for power plants. In October (the most recent figures available) 33% of U.S. electricity produced came from natural gas, about 1% ahead of coal. Renewables were 15%, of which hydroelectric is just over a third. The rivers and waterfalls whose flows can be harnessed have long been identified, so don’t expect hydro to grow much. Solar and wind were 7.5%, up from 5.9% a year ago. Germany’s solar and wind contributed 18.2% of their power generation, although by consumption it was less because they export some of this clean electricity (see below).

Germany’s Energiewende faces two problems. The first is common to solar and wind everywhere – it’s not always sunny and windy. Since it’s still not currently possible to store large amounts of electricity cheaply for later use, conventionally powered baseload electricity capacity is required. Germany’s shutting down many of their nuclear reactors following Japan’s 2011 Fukushima disaster increased their reliance on coal to ensure a certain minimum amount of electricity is available. Around 12% of Germany’s electricity is generated by natural gas, and while it might make sense to increase this, Russia is their biggest supplier. Greater reliance on Russia’s Gazprom would synchronize disruptive pipeline maintenance with periods of policy disagreement between the two countries.

Their second problem is that wind power comes from the northern part of the country and Baltic Sea, while it’s needed in the south. Today’s north-south transmission capability is inadequate to move what’s generated.

A further unexpected consequence of the move to renewables has been distortions in Germany’s electricity market. At times the operators of windfarms have been paid to stop electricity generation since the spot price has gone negative. At other times Germany has exported cheap electricity to neighboring countries such as Poland, Czech Republic and Austria, which some claim has impeded those countries’ ability to develop local renewable energy sources.

The German government has taken steps to moderate near term growth of renewable capacity while the transmission network is brought into better alignment with output. None of the problems Germany is facing seem insurmountable over the long term, and America’s relatively greener credentials will probably be challenged. But given the political support for current policies in Germany, it’s notable how challenging they’re finding it to execute successfully.

Important Disclosures

The information provided is for informational purposes only and investors should determine for themselves whether a particular service, security or product is suitable for their investment needs. The information contained herein is not complete, may not be current, is subject to change, and is subject to, and qualified in its entirety by, the more complete disclosures, risk factors and other terms that are contained in the disclosure, prospectus, and offering. Certain information herein has been obtained from third party sources and, although believed to be reliable, has not been independently verified and its accuracy or completeness cannot be guaranteed. No representation is made with respect to the accuracy, completeness or timeliness of this information. Nothing provided on this site constitutes tax advice. Individuals should seek the advice of their own tax advisor for specific information regarding tax consequences of investments. Investments in securities entail risk and are not suitable for all investors. This site is not a recommendation nor an offer to sell (or solicitation of an offer to buy) securities in the United States or in any other jurisdiction.

References to indexes and benchmarks are hypothetical illustrations of aggregate returns and do not reflect the performance of any actual investment. Investors cannot invest in an index and do not reflect the deduction of the advisor’s fees or other trading expenses. There can be no assurance that current investments will be profitable. Actual realized returns will depend on, among other factors, the value of assets and market conditions at the time of disposition, any related transaction costs, and the timing of the purchase. Indexes and benchmarks may not directly correlate or only partially relate to portfolios managed by SL Advisors as they have different underlying investments and may use different strategies or have different objectives than portfolios managed by SL Advisors (e.g. The Alerian index is a group MLP securities in the oil and gas industries. Portfolios may not include the same investments that are included in the Alerian Index. The S & P Index does not directly relate to investment strategies managed by SL Advisers.)

This site may contain forward-looking statements relating to the objectives, opportunities, and the future performance of the U.S. market generally. Forward-looking statements may be identified by the use of such words as; “believe,” “expect,” “anticipate,” “should,” “planned,” “estimated,” “potential” and other similar terms. Examples of forward-looking statements include, but are not limited to, estimates with respect to financial condition, results of operations, and success or lack of success of any particular investment strategy. All are subject to various factors, including, but not limited to general and local economic conditions, changing levels of competition within certain industries and markets, changes in interest rates, changes in legislation or regulation, and other economic, competitive, governmental, regulatory and technological factors affecting a portfolio’s operations that could cause actual results to differ materially from projected results. Such statements are forward-looking in nature and involves a number of known and unknown risks, uncertainties and other factors, and accordingly, actual results may differ materially from those reflected or contemplated in such forward-looking statements. Prospective investors are cautioned not to place undue reliance on any forward-looking statements or examples. None of SL Advisors LLC or any of its affiliates or principals nor any other individual or entity assumes any obligation to update any forward-looking statements as a result of new information, subsequent events or any other circumstances. All statements made herein speak only as of the date that they were made. r

Certain hyperlinks or referenced websites on the Site, if any, are for your convenience and forward you to third parties’ websites, which generally are recognized by their top level domain name. Any descriptions of, references to, or links to other products, publications or services does not constitute an endorsement, authorization, sponsorship by or affiliation with SL Advisors LLC with respect to any linked site or its sponsor, unless expressly stated by SL Advisors LLC. Any such information, products or sites have not necessarily been reviewed by SL Advisors LLC and are provided or maintained by third parties over whom SL Advisors LLC exercise no control. SL Advisors LLC expressly disclaim any responsibility for the content, the accuracy of the information, and/or quality of products or services provided by or advertised on these third-party sites.

All investment strategies have the potential for profit or loss. Different types of investments involve varying degrees of risk, and there can be no assurance that any specific investment will be suitable or profitable for a client’s investment portfolio.

Past performance of the American Energy Independence Index is not indicative of future returns.

Simon – nice piece, as usual. My only caveat is that there is no “debate” about whether climate change in man made, there are simply those that refuse to accept overwhelming empirical evidence because it would harm their immediate economic interests to do so. Germany is confronting the issue of matching the production of renewable energy (when it’s sunny and windy) with demand sooner than other countries. I wonder if that will then allow them to take the lead in the solution – which will undoubtedly come, and probably sooner than we expect.

Kevin, thanks for the feedback.

?exactly Kevin there is no “ debate” on a ecological crisis among most ( 97%) experts & thinking persons ; maybe only in US minds the United States of Hedonism & Climate Denial . Good analysis but