Change and Uncertainty

As I watched President Trump’s inauguration speech on January 20th, I was reminded of Paul Kennedy’s 1987 book, The Rise and Fall of the Powers. Kennedy charts the arc of many great empires over the last couple of millennia. He finds a repeated cycle of geographic enlargement through technological and economic dominance followed eventually by what he calls “Imperial Overstretch”, as maintaining control exceeds the resources available. It’s a big topic well beyond the scope of a monthly newsletter to adequately address; many will challenge the notion of the U.S. as an empire, and will reject that decline in any form is imminent. But America’s share of global GDP is shrinking simply because other countries are catching up. Greater geopolitical competition makes staying ahead ever more costly.

What prompted this thought was the vision of an America more ready to examine the payback from neighborly interactions. The post-World War II period began with America investing in rebuilding a broken Europe and Japan out of an unquestioned faith that benefits would accrue back. Perhaps we are now acknowledging that if the world doesn’t bother us we’ll leave it to its own devices; a more transactional approach will govern sovereign relations. Other countries have plenty of resources too. The wars in Iraq and Afghanistan following 2001 have cost up to $5TN by some estimates, echoing Kennedy’s warning about foreign entanglements ultimately exhausting resources.

“We do not seek to impose our way of life on anyone, but rather to let it shine as an example. We will shine for everyone to follow.” If you focus on the words and not the speaker, this is not a radical statement. While not soaring rhetoric, many could agree with the sentiment. Support for a more inward-looking America is not a new phenomenon, and finds adherents across the political spectrum.

Public policy is likely to shift in ways that will impact investment returns, more so than in many years. The great challenge in writing on such topics is to be non-partisan. Following the most divisive election in living memory, strength of feeling on both sides has not obviously weakened. Considering the investment impact of, or even support for, Trump Administration policy moves doesn’t imply endorsement of the candidate. We are just trying to allocate capital thoughtfully.

To pick one current example, on the first business day following his Inauguration Trump formally withdrew the U.S. from the Trans-Pacific Partnership (TPP). Obama had long pushed for the TPP as a way to bind the countries of Asia more closely together through trade and therefore shared prosperity. The European Union was originally conceived as the European Coal and Steel Community to end the string of three successive military defeats France had suffered against Germany by increasing trade links, making conflict prohibitively costly.

Trump’s assessment of the TPP was that the U.S. should negotiate bilateral trade agreements with other TPP countries. It may not appear quite so visionary, but there’s a certain industrial logic to a series of one-off deals. They’re simpler to negotiate, and the U.S. must enjoy a stronger position in any one-on-one discussion than as the largest in a room of twelve.

More broadly, if you’re looking for reasons to worry about the future there is plenty of material. Trump’s negotiating style rests on making demands that invite failure before agreement; how else to ensure the best terms have been achieved? Uncertainty is fuelled by the absence of prior government experience and unpredictability. These are positives or negatives depending on how you voted. Holding extra cash as protection against a negative surprise is understandable; it’s a comfortable, highly defensible posture and if worst fears aren’t realized the subsequent deployment of a lot of this cash will likely push stocks higher.

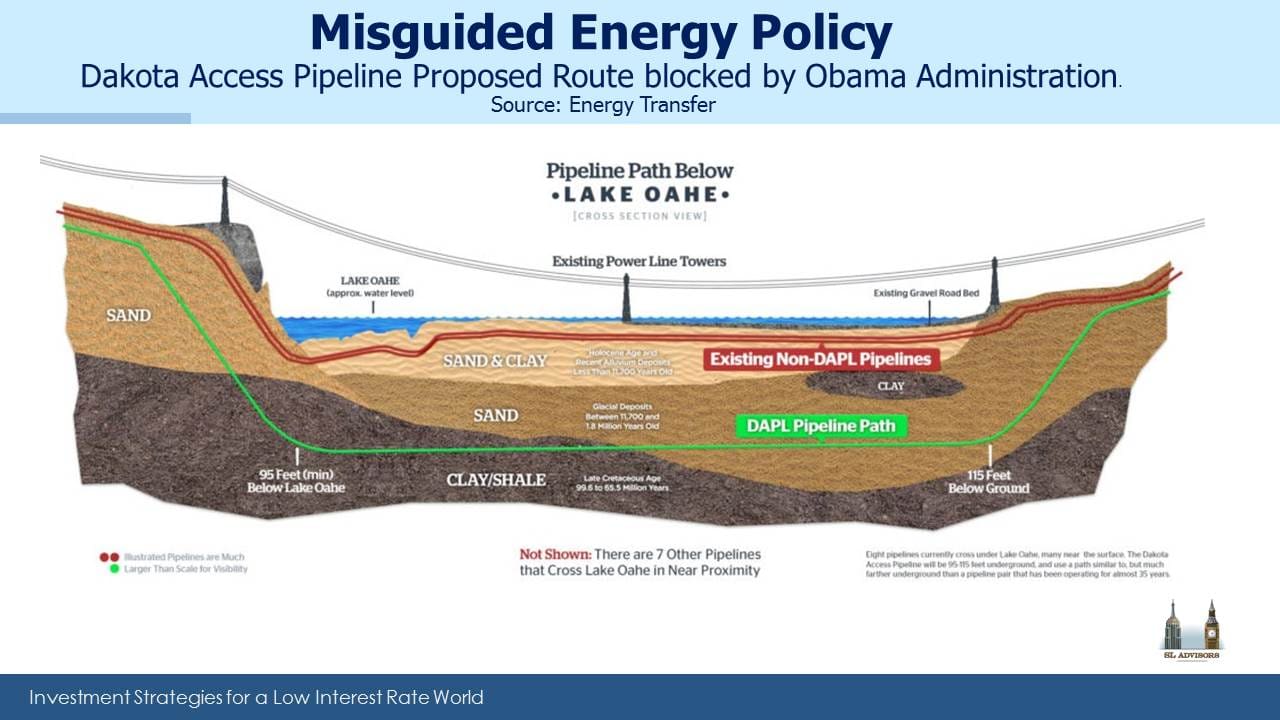

For investors in the energy sector, Trump has provided much to cheer and little of concern. Support for American Energy Independence and a renewed focus on infrastructure can only be good for the businesses that own the pipelines, storage facilities, fractionation plants and related properties that get hydrocarbons where they need to go. The sorry saga of the Dakota Access Pipeline (DAPL) built by Energy Transfer Partners (ETP) reflected poorly on President Obama’s capricious decision making. Having been properly approved by the U.S. Army Corps of Engineers and virtually completed, this $3.8BN project was delayed by the outgoing Administration, which in effect rescinded prior approvals without ever finding fault with the process ETP had followed.

The proposed pipeline under Lake Oahe in North Dakota passes below an existing pipeline. When completed, DAPL will move crude oil to market in the Midwest and reduce reliance on Crude by Rail (CBR), which is more expensive and more prone to accidents. The Washington Post, not exactly a stridently Conservative mouthpiece, noted that crude spills were significantly more likely with CBR than by pipeline when adjusted for volumes and distance traveled. The 2013 disaster in Lac-Megantic, Quebec when a trainload of crude oil exploded and killed 47 people led some to refer to CBR as “bomb trains.”

Meanwhile, $3.8BN in capital was kept waiting to produce a productive return while government policy was changed with little regard for the chilling impact on future projects or even basic fairness. This is a narrow issue and not an election-deciding one for most people. But few can be surprised at Energy Transfer Equity (ETE, ETP’s General Partner) CEO Kelcy Warren’s happiness at Obama’s departure – a sentiment shared by many energy industry executives. Trump’s swift approval of this project and the Keystone pipeline (another political hostage) were encouragingly pragmatic and certainly cheered MLP investors.

Most of the bad scenarios the concerned investor can imagine should not impact domestic energy infrastructure much at all. The likely thrust of policy will be supportive. Many equity sectors and individual stocks are close to all-time highs, exposed to the commensurate downside that can accompany lofty valuations. MLPs retain plenty of upside.

We are invested in ETE

Important Disclosures

The information provided is for informational purposes only and investors should determine for themselves whether a particular service, security or product is suitable for their investment needs. The information contained herein is not complete, may not be current, is subject to change, and is subject to, and qualified in its entirety by, the more complete disclosures, risk factors and other terms that are contained in the disclosure, prospectus, and offering. Certain information herein has been obtained from third party sources and, although believed to be reliable, has not been independently verified and its accuracy or completeness cannot be guaranteed. No representation is made with respect to the accuracy, completeness or timeliness of this information. Nothing provided on this site constitutes tax advice. Individuals should seek the advice of their own tax advisor for specific information regarding tax consequences of investments. Investments in securities entail risk and are not suitable for all investors. This site is not a recommendation nor an offer to sell (or solicitation of an offer to buy) securities in the United States or in any other jurisdiction.

References to indexes and benchmarks are hypothetical illustrations of aggregate returns and do not reflect the performance of any actual investment. Investors cannot invest in an index and do not reflect the deduction of the advisor’s fees or other trading expenses. There can be no assurance that current investments will be profitable. Actual realized returns will depend on, among other factors, the value of assets and market conditions at the time of disposition, any related transaction costs, and the timing of the purchase. Indexes and benchmarks may not directly correlate or only partially relate to portfolios managed by SL Advisors as they have different underlying investments and may use different strategies or have different objectives than portfolios managed by SL Advisors (e.g. The Alerian index is a group MLP securities in the oil and gas industries. Portfolios may not include the same investments that are included in the Alerian Index. The S & P Index does not directly relate to investment strategies managed by SL Advisers.)

This site may contain forward-looking statements relating to the objectives, opportunities, and the future performance of the U.S. market generally. Forward-looking statements may be identified by the use of such words as; “believe,” “expect,” “anticipate,” “should,” “planned,” “estimated,” “potential” and other similar terms. Examples of forward-looking statements include, but are not limited to, estimates with respect to financial condition, results of operations, and success or lack of success of any particular investment strategy. All are subject to various factors, including, but not limited to general and local economic conditions, changing levels of competition within certain industries and markets, changes in interest rates, changes in legislation or regulation, and other economic, competitive, governmental, regulatory and technological factors affecting a portfolio’s operations that could cause actual results to differ materially from projected results. Such statements are forward-looking in nature and involves a number of known and unknown risks, uncertainties and other factors, and accordingly, actual results may differ materially from those reflected or contemplated in such forward-looking statements. Prospective investors are cautioned not to place undue reliance on any forward-looking statements or examples. None of SL Advisors LLC or any of its affiliates or principals nor any other individual or entity assumes any obligation to update any forward-looking statements as a result of new information, subsequent events or any other circumstances. All statements made herein speak only as of the date that they were made. r

Certain hyperlinks or referenced websites on the Site, if any, are for your convenience and forward you to third parties’ websites, which generally are recognized by their top level domain name. Any descriptions of, references to, or links to other products, publications or services does not constitute an endorsement, authorization, sponsorship by or affiliation with SL Advisors LLC with respect to any linked site or its sponsor, unless expressly stated by SL Advisors LLC. Any such information, products or sites have not necessarily been reviewed by SL Advisors LLC and are provided or maintained by third parties over whom SL Advisors LLC exercise no control. SL Advisors LLC expressly disclaim any responsibility for the content, the accuracy of the information, and/or quality of products or services provided by or advertised on these third-party sites.

All investment strategies have the potential for profit or loss. Different types of investments involve varying degrees of risk, and there can be no assurance that any specific investment will be suitable or profitable for a client’s investment portfolio.

Past performance of the American Energy Independence Index is not indicative of future returns.

Leave a Reply

Want to join the discussion?Feel free to contribute!