Pity the Equity Analyst

This week I felt a pang of pity for a sell-side research analyst. Not an obviously sympathetic constituency, you might well retort. There are many other categories of employment more deserving of such consideration – indeed, probably too numerous to list here. But I did, and here’s why.

This particular analyst (he’ll remain nameless because I don’t wish to embarrass him) has been a relentless cheerleader for Master Limited Partnerships and increasingly so as their prices have plummeted. That’s already sufficient reason for me to express my sympathy. You may have spotted that we have something in common.

Explaining why MLPs keep falling in willful defiance of what an evident minority asserts is compelling valuation can be tiring, and some become weary of it before others.

Plains All America (PAA) is the midstream infrastructure MLP most clearly linked with falling crude oil prices. Like most MLPs they rely on issuing equity to fund their growth plans, and PAA has been growing in recent years to accommodate increased domestic oil production. Acknowledging the unwillingness of investors to fund growth as well as the reality of falling domestic production, PAA recently cut their 2016 growth plans from $2.1BN to $1.5BN.

On Tuesday, January 12th PAA announced they had raised $1.5BN through a convertible preferred security yielding 8%, some 5% less than the yield on their equity. It was privately placed with several institutions, and as a result PAA has no need to issue equity through 2017. Moreover, it was pretty cheap capital since it is convertible to equity at the holder’s option in two years or at PAA’s option (under certain circumstances) in three. In any event, it is junior to all their other liabilities and is in reality equity (which is how PAA regards it). Private equity investors, not normally accused of superficial research, saw fit to invest $1.5BN in equity in an MLP.

So you have a piece of news that is unambiguously positive, in that PAA raised capital on surprisingly inexpensive terms from informed investors and is no longer a seller of its own equity. Now let’s return to our sell-side analyst.

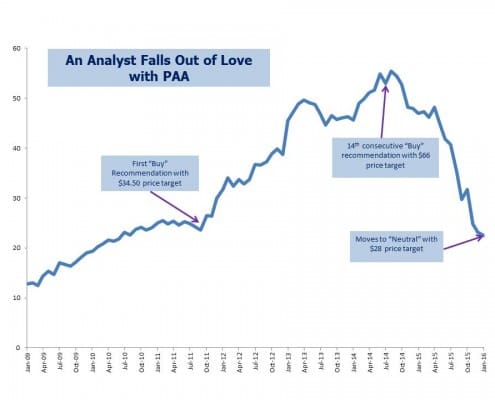

Research reports include a history of the Certifying Analyst’s prior recommendations on the stock. PAA had been a Buy (called an “Overweight”) since October 2011, at which time it was trading at $30 with a price target of $34.50. Through 19 subsequent revisions the Buy recommendation remained, with the price target regularly adjusted so as to be always 10-20% higher than the current price. In October 2014, with PAA at $58 the peak price target of $66 was recorded.

To quote a friend of mine, from that point down was a long way and on Monday, January 11th just prior to PAA’s announcement, its stock closed at $20.36, 70% below its target of fifteen months earlier. Now put the numbers aside, and consider what the past fifteen months have been like for the sell-side analyst. He has doggedly articulated the bullish case through the most relentless selling. He has noted the fee-based nature of PAA’s cashflows, the highly regarded management and their history of solid execution. His analysis is widely read and his day must have increasingly been one of verbal jousting with his firm’s salespeople as they relayed client dissatisfaction and most likely anger. When losing money on an investment it’s some small solace to blame one of the unapologetic cheerleaders.

Sell-side analysts can be highly paid (although one suspects that MLP analysts face a supply/demand imbalance similar to crude oil). But even highly paid people have a breaking point, and this week our analyst reached his. We know this because on Wednesday, January 13th following PAA’s $1.5BN capital raise the sequence of 20 consecutive Buy recommendations was finally broken with a switch to Neutral. The unspoken message was clear:

I am tired of this. Let me hide in the obscurity of the current market price. I no longer wish to explain what cannot be explained to my colleagues or my clients. I am out.

This is how it feels to sell after intending to never sell. If you’re planning to panic, it’s best done immediately.

How do I infer this from a research report that doesn’t make such a confession? Because of what it does say. Acknowledging that the capital raise was undoubtedly good, our analyst nonetheless downgrades the stock because of lack of visibility around crude oil. Of course the crude oil price remains both highly visible and unpleasant. Moreover, because all good research must include a Mathematical basis by which the current price target is derived, the discount rate on PAA’s future cashflows was arbitrarily jacked up to 11% and a zero growth rate was assumed on their terminal value beyond ten years. This last point will seem obscure but is important – PAA is highly unlikely to forego forever price increases on its assets in the future. Or put another way, how do you change the spreadsheet inputs so as to get the desired output, which is an innocuous price target close to the current market so I don’t have to talk about PAA anymore.

Also of note was that our analyst didn’t rely on any of the familiar criticisms of industry bears, such as that the MLP model is irretrievably broken, that contracts will suffer widespread renegotiation or abrogation in bankruptcy court, or that MLPs are a Ponzi scheme. This is because he for one can’t find much evidence of that or he would most assuredly have relied on such to justify his about-face following a 70% drop. He’s just had enough.

Meanwhile, on Wednesday PAA yielded 14% on an unchanged dividend newly declared. Its General Partner, Plains GP Holdings (PAGP) which we own yielded 11.5%. The analyst isn’t even forecasting a dividend cut.

The point of this story is not to argue that PAA or PAGP are cheap, but to show why MLPs remain so weak. The people involved are reaching the limits of their tolerance for remaining bullish when the P&L’s of countless MLP holders say very loudly that any MLP proponent must have an IQ lower than room temperature. The facts as reflected in market prices relentlessly say so. One guy’s had enough, and I feel his pain but shan’t follow his lead.

Important Disclosures

The information provided is for informational purposes only and investors should determine for themselves whether a particular service, security or product is suitable for their investment needs. The information contained herein is not complete, may not be current, is subject to change, and is subject to, and qualified in its entirety by, the more complete disclosures, risk factors and other terms that are contained in the disclosure, prospectus, and offering. Certain information herein has been obtained from third party sources and, although believed to be reliable, has not been independently verified and its accuracy or completeness cannot be guaranteed. No representation is made with respect to the accuracy, completeness or timeliness of this information. Nothing provided on this site constitutes tax advice. Individuals should seek the advice of their own tax advisor for specific information regarding tax consequences of investments. Investments in securities entail risk and are not suitable for all investors. This site is not a recommendation nor an offer to sell (or solicitation of an offer to buy) securities in the United States or in any other jurisdiction.

References to indexes and benchmarks are hypothetical illustrations of aggregate returns and do not reflect the performance of any actual investment. Investors cannot invest in an index and do not reflect the deduction of the advisor’s fees or other trading expenses. There can be no assurance that current investments will be profitable. Actual realized returns will depend on, among other factors, the value of assets and market conditions at the time of disposition, any related transaction costs, and the timing of the purchase. Indexes and benchmarks may not directly correlate or only partially relate to portfolios managed by SL Advisors as they have different underlying investments and may use different strategies or have different objectives than portfolios managed by SL Advisors (e.g. The Alerian index is a group MLP securities in the oil and gas industries. Portfolios may not include the same investments that are included in the Alerian Index. The S & P Index does not directly relate to investment strategies managed by SL Advisers.)

This site may contain forward-looking statements relating to the objectives, opportunities, and the future performance of the U.S. market generally. Forward-looking statements may be identified by the use of such words as; “believe,” “expect,” “anticipate,” “should,” “planned,” “estimated,” “potential” and other similar terms. Examples of forward-looking statements include, but are not limited to, estimates with respect to financial condition, results of operations, and success or lack of success of any particular investment strategy. All are subject to various factors, including, but not limited to general and local economic conditions, changing levels of competition within certain industries and markets, changes in interest rates, changes in legislation or regulation, and other economic, competitive, governmental, regulatory and technological factors affecting a portfolio’s operations that could cause actual results to differ materially from projected results. Such statements are forward-looking in nature and involves a number of known and unknown risks, uncertainties and other factors, and accordingly, actual results may differ materially from those reflected or contemplated in such forward-looking statements. Prospective investors are cautioned not to place undue reliance on any forward-looking statements or examples. None of SL Advisors LLC or any of its affiliates or principals nor any other individual or entity assumes any obligation to update any forward-looking statements as a result of new information, subsequent events or any other circumstances. All statements made herein speak only as of the date that they were made. r

Certain hyperlinks or referenced websites on the Site, if any, are for your convenience and forward you to third parties’ websites, which generally are recognized by their top level domain name. Any descriptions of, references to, or links to other products, publications or services does not constitute an endorsement, authorization, sponsorship by or affiliation with SL Advisors LLC with respect to any linked site or its sponsor, unless expressly stated by SL Advisors LLC. Any such information, products or sites have not necessarily been reviewed by SL Advisors LLC and are provided or maintained by third parties over whom SL Advisors LLC exercise no control. SL Advisors LLC expressly disclaim any responsibility for the content, the accuracy of the information, and/or quality of products or services provided by or advertised on these third-party sites.

All investment strategies have the potential for profit or loss. Different types of investments involve varying degrees of risk, and there can be no assurance that any specific investment will be suitable or profitable for a client’s investment portfolio.

Past performance of the American Energy Independence Index is not indicative of future returns.

While I can agree with much of what you’ve said, there’s one point that neither you nor anyone on the call following the preferred announcement fully explored. Take a look at PAA’s investor presentation issued simultaneously with that announcement. I have a hard time agreeing with PAA’s outlook for oil prices and US onshore production for this year and next. If those projections are off, then there could be more trouble than management lets on.