The Hedge Fund Mirage Turns Five

Five years ago this month John Wiley published my first book. The Hedge Fund Mirage; The Illusion of Big Money and Why It’s Too Good to Be True explained how hedge funds have in aggregate been a great business and a lousy investment. The opening sentence asserted that treasury bills would have been a better choice for the average hedge fund investor. This was a startling conclusion, since money had long been flowing to hedge funds in willful defiance of steadily worsening results. Surely, the flows were confirmation that the smart money was in hedge funds.

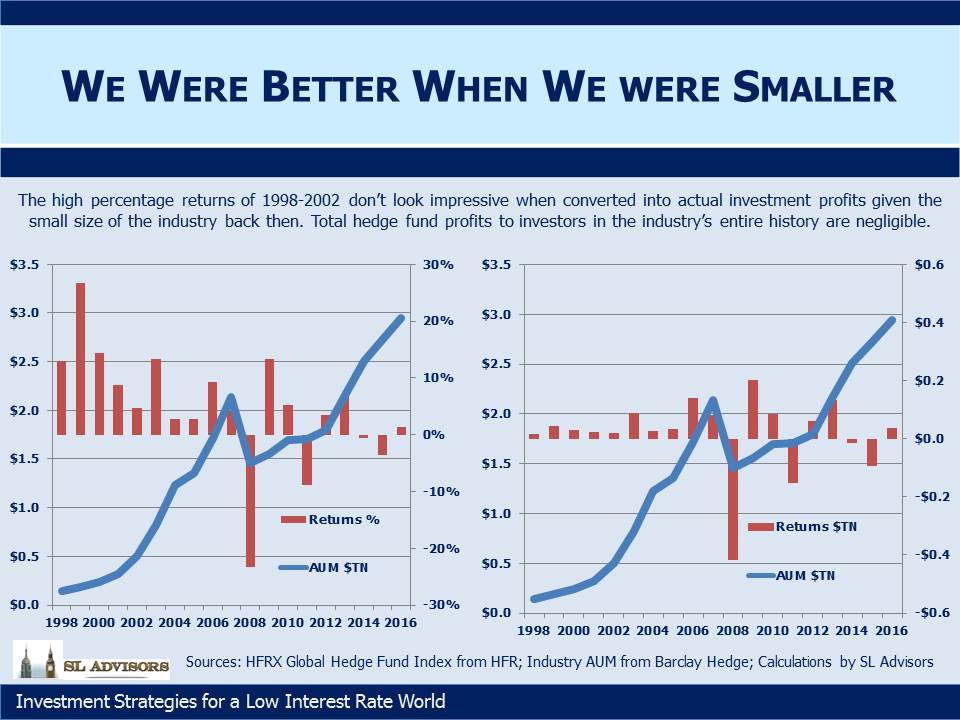

Hedge fund returns are conventionally presented from the perspective of a single investment at the beginning of the period. Such an approach is far from reflective of the experience of investors, since few were fortunate enough to invest in hedge funds in those early years. From 1998-2002 hedge fund investors enjoyed great returns; there just weren’t that many investors. A more meaningful analysis considers everyone’s returns. For this, you need to look at the asset weighted return, or IRR; the return on the average dollar invested rather than the first dollar. The difference is most stark when percentage returns (the left panel in the chart) are recalculated and shown as actual investment profits (the right panel). Viewed this way, hedge funds have delivered mediocre returns at great expense. The high percentage returns of the early years didn’t generate much actual profit for investors, because the investors were few. They benefitted from exploiting many inefficiencies in financial markets without the burden of too much capital.

Substantial sums followed with the misplaced hope of achieving similar results. The book was aimed not at hedge fund managers but at the stewards of this misdirected capital; hedge fund managers are an intelligent bunch and scarcely needed any advice. The goal was to help the star-struck institutional investors challenge the guidance of their consultants, and avoid high fee strategies that too often enrich the managers but not the clients.

Five years is probably a fair period of time over which to assess the most important prediction made in the book, which was that hedge fund returns would be disappointing. This was a lonely view at the time – not as completely obvious as it should have been. The entire industry was being weighed down by the growing pool of assets it was managing. The availability of uncorrelated returns, which is what hedge funds try to provide, is finite; inevitably, dilution of returns followed.

Small hedge funds outperform big ones. Any big hedge fund did better when it was small (which is how it became big). These first two insights are generally accepted, and yet very few investors take the third logical step in this sequence of thoughts – a small hedge fund industry generated higher returns than a big one. Hedge funds were, and remain, over-capitalized.

Today, it’s not hard to find critics of the industry including some of its most successful practitioners. Assets are too plentiful and fees too high. This now passes for conventional wisdom although in 2011 that was certainly not the case.

A disappointing consequence of America’s increasing political polarization is the tendency of each side to assume the other is intellectually challenged. I try hard to guard against this tendency myself, but have to concede that on the subject of hedge funds I have failed. Which is to say, the hedge fund professionals who praised The Hedge Fund Mirage when it came out, merely confirmed the superior investing intellect that their businesses had already demonstrated. The critics (who generally aspired to invest money rather than actually doing so) similarly confirmed their place at the other end of this intellectual spectrum.

Hedge fund managers are by no means the villains in this story. Some of the smartest people around run hedge funds because that’s where the financial rewards are greatest. If every hedge fund manager sincerely believes their fund is the best, this is no different than individual business owners in any industry. Many managers have long recognized the challenges of asset size even while maintaining they could rise above the weight of mediocrity.

The fault lies with those who aggregate all those optimistic individual views into a positive one of the industry without considering the obvious negative consequences of too much money. Not every institutional investor has the ability to run a hedge fund. Some of the least sophisticated investors I’ve ever met are the trustees of public pension plans. They understandably rely heavily on consultants to guide them, not just for their expertise but also because as fiduciaries their decisions are subject to scrutiny under ERISA (the Employee Retirement Income Security Act).

Although critics of The Hedge Fund Mirage were few in number, a couple are worth noting. The London-based Alternative Investment Management Association (AIMA), led at the time by Andrew Baker, abandoned any pretense of objectivity in their eagerness to defend the indefensible. They do represent hedge funds if not actually running one. An initial attempt at making the case for hedge funds was followed by a more lengthy but no more persuasive effort. One journalist famously noted that, “…the AIMA paper has convinced me of the deep truth of Lack’s book in a way that the book itself never could.”

Thomas Schneeweis, an academic and hedge fund consultant, descended from his ivory tower to criticize what he called “baby hedge fund analysis 101.” For the sake of investors everywhere, one must hope that his investment acumen surpasses his business building ability, ensuring few victims of any Schneeweis insight.

In short, the critics were dead wrong.

Although on average hedge fund investors have done poorly, there are great hedge funds and happy clients. There probably always will be. It’s not all bad. While it’s extremely hard to pick hedge funds, some investors are good at it. Some hedge fund investors focus on smaller managers where research has shown returns are higher. As hedge funds have become more generic their returns have become more prosaic. Success relies on leaving the well-traveled path and considering more obscure strategies.

Perhaps the strongest criticism of The Hedge Fund Mirage is that inflows to hedge funds have continued when they shouldn’t have. The reason this has happened in spite of overwhelming evidence that disappointment will follow lies in some quirky accounting. Public pension funds (such as the $300BN California Public Employee Retirement System, or CalPERS) don’t use GAAP (Generally Accepted Accounting Principles) accounting like public companies. Under GASB (Governmental Accounting Standards Board), investing in riskier assets has the odd result of lowering the present value of your pension obligations. There’s no economic connection between the two, and the flawed underlying logic is slowly creating a massive problem. It’s why public pension funds are today’s biggest hedge fund investors, a folly that will ultimately saddle taxpayers with the bill for unfunded pensions to retired teachers, firefighters and policemen in many U.S. states. Returns will continue to come up short.

The hedge fund consultants sit between the expensive, poorly performing hedge fund industry and the unsophisticated trustees of many public pension funds. The consultants are smart enough to understand the consequences of GASB, and commercial enough to know how to exploit this knowledge by guiding their naïve clients towards complex investments whose sourcing generates further consulting fees. There is a special place in Investment Purgatory for those who ply such a trade. The poor bargain this represents is gradually being acknowledged, often by early adopters including CalPERS who concluded hedge funds were going to create more problems than they’d solve.

That attractive hedge fund returns are a mirage is slowly dawning on the not-so-sophisticated institutions whose portfolios include them. The industry remains over-capitalized. Few of today’s investors even think to consider what level of total hedge fund assets is consistent with their aspirational returns. Until they do, continued disappointment awaits.

Important Disclosures

The information provided is for informational purposes only and investors should determine for themselves whether a particular service, security or product is suitable for their investment needs. The information contained herein is not complete, may not be current, is subject to change, and is subject to, and qualified in its entirety by, the more complete disclosures, risk factors and other terms that are contained in the disclosure, prospectus, and offering. Certain information herein has been obtained from third party sources and, although believed to be reliable, has not been independently verified and its accuracy or completeness cannot be guaranteed. No representation is made with respect to the accuracy, completeness or timeliness of this information. Nothing provided on this site constitutes tax advice. Individuals should seek the advice of their own tax advisor for specific information regarding tax consequences of investments. Investments in securities entail risk and are not suitable for all investors. This site is not a recommendation nor an offer to sell (or solicitation of an offer to buy) securities in the United States or in any other jurisdiction.

References to indexes and benchmarks are hypothetical illustrations of aggregate returns and do not reflect the performance of any actual investment. Investors cannot invest in an index and do not reflect the deduction of the advisor’s fees or other trading expenses. There can be no assurance that current investments will be profitable. Actual realized returns will depend on, among other factors, the value of assets and market conditions at the time of disposition, any related transaction costs, and the timing of the purchase. Indexes and benchmarks may not directly correlate or only partially relate to portfolios managed by SL Advisors as they have different underlying investments and may use different strategies or have different objectives than portfolios managed by SL Advisors (e.g. The Alerian index is a group MLP securities in the oil and gas industries. Portfolios may not include the same investments that are included in the Alerian Index. The S & P Index does not directly relate to investment strategies managed by SL Advisers.)

This site may contain forward-looking statements relating to the objectives, opportunities, and the future performance of the U.S. market generally. Forward-looking statements may be identified by the use of such words as; “believe,” “expect,” “anticipate,” “should,” “planned,” “estimated,” “potential” and other similar terms. Examples of forward-looking statements include, but are not limited to, estimates with respect to financial condition, results of operations, and success or lack of success of any particular investment strategy. All are subject to various factors, including, but not limited to general and local economic conditions, changing levels of competition within certain industries and markets, changes in interest rates, changes in legislation or regulation, and other economic, competitive, governmental, regulatory and technological factors affecting a portfolio’s operations that could cause actual results to differ materially from projected results. Such statements are forward-looking in nature and involves a number of known and unknown risks, uncertainties and other factors, and accordingly, actual results may differ materially from those reflected or contemplated in such forward-looking statements. Prospective investors are cautioned not to place undue reliance on any forward-looking statements or examples. None of SL Advisors LLC or any of its affiliates or principals nor any other individual or entity assumes any obligation to update any forward-looking statements as a result of new information, subsequent events or any other circumstances. All statements made herein speak only as of the date that they were made. r

Certain hyperlinks or referenced websites on the Site, if any, are for your convenience and forward you to third parties’ websites, which generally are recognized by their top level domain name. Any descriptions of, references to, or links to other products, publications or services does not constitute an endorsement, authorization, sponsorship by or affiliation with SL Advisors LLC with respect to any linked site or its sponsor, unless expressly stated by SL Advisors LLC. Any such information, products or sites have not necessarily been reviewed by SL Advisors LLC and are provided or maintained by third parties over whom SL Advisors LLC exercise no control. SL Advisors LLC expressly disclaim any responsibility for the content, the accuracy of the information, and/or quality of products or services provided by or advertised on these third-party sites.

All investment strategies have the potential for profit or loss. Different types of investments involve varying degrees of risk, and there can be no assurance that any specific investment will be suitable or profitable for a client’s investment portfolio.

Past performance of the American Energy Independence Index is not indicative of future returns.

Leave a Reply

Want to join the discussion?Feel free to contribute!