The Bond Market Loses Its Friends

In 2013, my book Bonds Are Not Forever; The Crisis Facing Fixed Income Investors presented a populist framework for evaluating interest rates. The prospects for the bond market can only be evaluated by considering the U.S. fiscal situation, which is steadily deteriorating along with that of many states. I was dismayed to read the other day of an analysis that places New Jersey (where I live) dead last behind even Illinois in its funding of public sector pensions. We have, at almost every level of government and household, too much debt.

The solution has, since the 2008 Financial Crisis been low rates. If you owe a lot of money low rates are better than high ones. Financial repression in the form of returns that fail to beat inflation after taxes is a stealth means of transferring wealth from savers (lenders) to borrowers. Count the central banks of China and Japan with their >$1TN in U.S. treasury holdings among those on the wrong side of this trade, along with many other foreign governments and sovereign wealth funds.

Some have argued that low rates only help the wealthy (through driving up asset prices); they impede lending (because lending rates aren’t high enough to induce banks to take risk); they force savers to save more (thereby consuming less) than they otherwise would, because returns are so low; and they communicate central bank concern about future economic prospects. Low mortgage rates help homeowners and drive up home values which helps McMansion owners but not first-time buyers. Low rates may be good for the wealthy, and by lessening the burden of the government’s debt they may indirectly help everyone. But to someone with little or no savings, the tangible benefits are not obvious even if they are real (through higher employment, for example).

Nonetheless, we are likely at the early stages of watching this benign process swing into reverse. The conventional result of lower taxes combined with higher spending should be a wider deficit, rising inflation and therefore higher interest rates. The bond market is already beginning to price this in through higher yields, well before any discussions of next year’s budget (or even the appointment of a White House Budget Director).

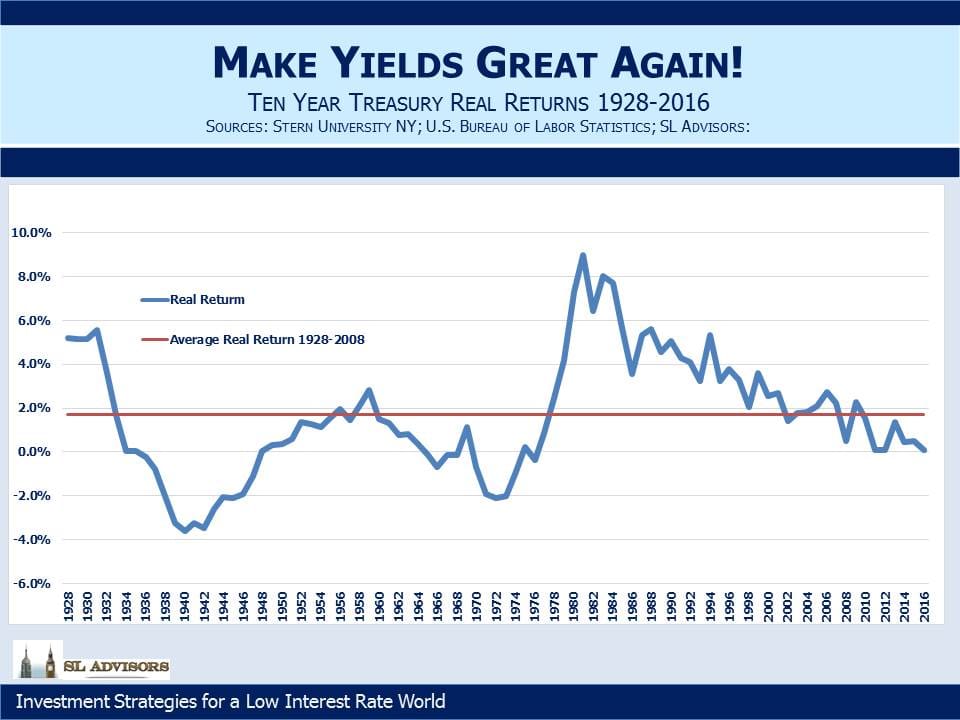

Part of the problem is that bonds don’t offer much value to begin with. They’ve represented an over-priced asset class for years, and it’ll take more than a 0.50% jump in yields to fix that. From 1928 until 2008 when the Federal Reserve’s Quantitative Easing program began distorting yields, the average annual return over inflation (that is, the real return) on ten year treasuries was 1.7%. This is calculated by comparing the average yield each year with the inflation rate that prevailed over the subsequent decade-long holding period of that security. So investing in a ten year treasury note today at 2% would, if the Fed hits its inflation target of 2% over the next ten years, deliver a 0% real return (worse after taxes).

Given the Federal Reserve’s 2% inflation target, even a 4% ten year treasury (roughly double its current yield) would appear to represent a no better than neutral valuation. The deficit was already set to begin rising again before even considering any Republican-enacted tax cuts and other stimulus (such as infrastructure spending). In fact, borrowing at today’s low rates to invest in projects that will improve productivity makes sense in many cases. But under such circumstances, with the possibility of inflation above 2%, perhaps a yield of 5% or even 6% is the threshold at which ten year treasuries (and by extension other long term U.S. corporate bonds at an appropriate spread higher) could justify an investment.

Holding out for such a yield is fanciful. Millions of investors demand far less, which is why we don’t bother with the bond market. Our valuation requirements render us wholly uncompetitive buyers.

Low rates may be the best policy for America, but it looks as if we’re about to try boosting growth through greater fiscal stimulus. The Federal Reserve will seek to normalize short term rates, perhaps faster than their current practice of annual 0.25% hikes. The twin friends of gridlock-induced fiscal discipline (sort of) and low rates are moving on, leaving fixed income investors to fend for themselves. Bonds are a very long way from representing an attractive investment.

Important Disclosures

The information provided is for informational purposes only and investors should determine for themselves whether a particular service, security or product is suitable for their investment needs. The information contained herein is not complete, may not be current, is subject to change, and is subject to, and qualified in its entirety by, the more complete disclosures, risk factors and other terms that are contained in the disclosure, prospectus, and offering. Certain information herein has been obtained from third party sources and, although believed to be reliable, has not been independently verified and its accuracy or completeness cannot be guaranteed. No representation is made with respect to the accuracy, completeness or timeliness of this information. Nothing provided on this site constitutes tax advice. Individuals should seek the advice of their own tax advisor for specific information regarding tax consequences of investments. Investments in securities entail risk and are not suitable for all investors. This site is not a recommendation nor an offer to sell (or solicitation of an offer to buy) securities in the United States or in any other jurisdiction.

References to indexes and benchmarks are hypothetical illustrations of aggregate returns and do not reflect the performance of any actual investment. Investors cannot invest in an index and do not reflect the deduction of the advisor’s fees or other trading expenses. There can be no assurance that current investments will be profitable. Actual realized returns will depend on, among other factors, the value of assets and market conditions at the time of disposition, any related transaction costs, and the timing of the purchase. Indexes and benchmarks may not directly correlate or only partially relate to portfolios managed by SL Advisors as they have different underlying investments and may use different strategies or have different objectives than portfolios managed by SL Advisors (e.g. The Alerian index is a group MLP securities in the oil and gas industries. Portfolios may not include the same investments that are included in the Alerian Index. The S & P Index does not directly relate to investment strategies managed by SL Advisers.)

This site may contain forward-looking statements relating to the objectives, opportunities, and the future performance of the U.S. market generally. Forward-looking statements may be identified by the use of such words as; “believe,” “expect,” “anticipate,” “should,” “planned,” “estimated,” “potential” and other similar terms. Examples of forward-looking statements include, but are not limited to, estimates with respect to financial condition, results of operations, and success or lack of success of any particular investment strategy. All are subject to various factors, including, but not limited to general and local economic conditions, changing levels of competition within certain industries and markets, changes in interest rates, changes in legislation or regulation, and other economic, competitive, governmental, regulatory and technological factors affecting a portfolio’s operations that could cause actual results to differ materially from projected results. Such statements are forward-looking in nature and involves a number of known and unknown risks, uncertainties and other factors, and accordingly, actual results may differ materially from those reflected or contemplated in such forward-looking statements. Prospective investors are cautioned not to place undue reliance on any forward-looking statements or examples. None of SL Advisors LLC or any of its affiliates or principals nor any other individual or entity assumes any obligation to update any forward-looking statements as a result of new information, subsequent events or any other circumstances. All statements made herein speak only as of the date that they were made. r

Certain hyperlinks or referenced websites on the Site, if any, are for your convenience and forward you to third parties’ websites, which generally are recognized by their top level domain name. Any descriptions of, references to, or links to other products, publications or services does not constitute an endorsement, authorization, sponsorship by or affiliation with SL Advisors LLC with respect to any linked site or its sponsor, unless expressly stated by SL Advisors LLC. Any such information, products or sites have not necessarily been reviewed by SL Advisors LLC and are provided or maintained by third parties over whom SL Advisors LLC exercise no control. SL Advisors LLC expressly disclaim any responsibility for the content, the accuracy of the information, and/or quality of products or services provided by or advertised on these third-party sites.

All investment strategies have the potential for profit or loss. Different types of investments involve varying degrees of risk, and there can be no assurance that any specific investment will be suitable or profitable for a client’s investment portfolio.

Past performance of the American Energy Independence Index is not indicative of future returns.

Down is a long way from here.