Williams Satisfies Two Masters; More on Solar

Williams Satisfies Two Masters

Master Limited Partnership (MLPs) have been reporting earnings over the past couple of weeks. They were largely as expected with several names providing modest positive surprises. There were also some other interesting announcements – notably the sale by Energy Transfer Partners (ETP) and Sunoco Logistics (SXL) of part of their interest in the Bakken Pipeline Project to Enbridge Energy Partners (EEP) and Marathon Petroleum (MPC).

We calculate that ETP and SXL collectively invested $2BN developing this asset and have received $2BN for a partial interest, leaving them with a significant economic stake for minimal cash outlay. In addition, they removed competitor project Sandpiper by bringing its sponsors into their project and MPC’s refineries will be an important customer which could provide an uplift to volumes. The value of the assets and backlog of the Energy Transfer Family is why we’re invested for now in ETP and SXL’s General Partner (GP), Energy Transfer Equity (ETE). This is in spite of misgivings about management who remain unapologetic about acting in their own self interest (see Will Energy Transfer Act With Integrity?). On this topic we salute friend Ethan Bellamy, R.W. Baird’s Senior Analyst covering MLPs, for shunning the usual, sycophantic “great quarter guys” posture of most analysts and asking CEO Kelcy Warren a direct question on his crooked converts.

But our focus this week is on Williams Companies (WMB). As they warned before the vote on their ill-fated merger with ETE, a dividend cut was coming and was duly announced this week. In the meantime, a failed effort to fire CEO Alan Armstrong resulted in six of thirteen board members resigning.

Dividend cuts usually reflect strategic mis-steps by management, and although WMB controls a unique asset in Transco (an extensive pipeline network covering much of the eastern U.S.) their stock has lagged the Alerian Index substantially over the past two years. CEO Armstrong might argue that the influence of activists led by Keith Meister (an investor whose long term advice is of dubious value, as we wrote in The Corvex Discount) forced poor strategic decisions. The pending sale to ETE limited WMB’s ability to make any other moves, such as raising capital, until it was resolved.

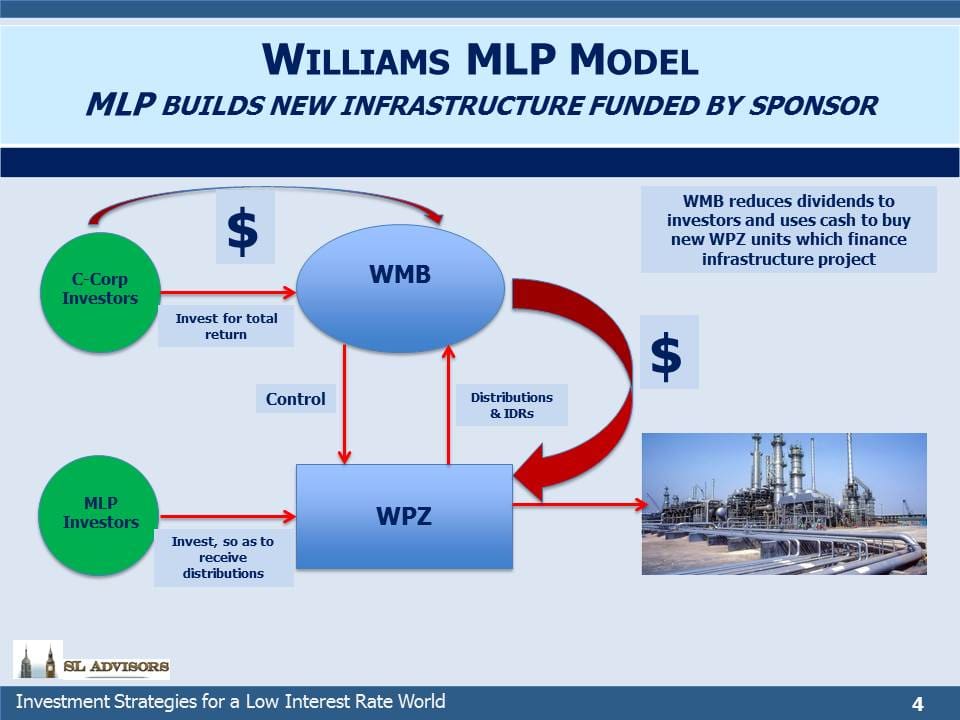

But in this case WMB is using the cash saved from its reduced dividend to fund its growth capex, most of which is going to expand its Transco asset at attractive multiples. Although WMB cut its dividend by 70%, its MLP Williams Partners (WPZ) maintained theirs and both securities rose on the news. It was a perfect illustration of the divergent views of dividends. WMB investors are total-return oriented and cheered the redirection of cash into high-return projects. WPZ investors just want the cash. Both classes of investors are getting what they want.

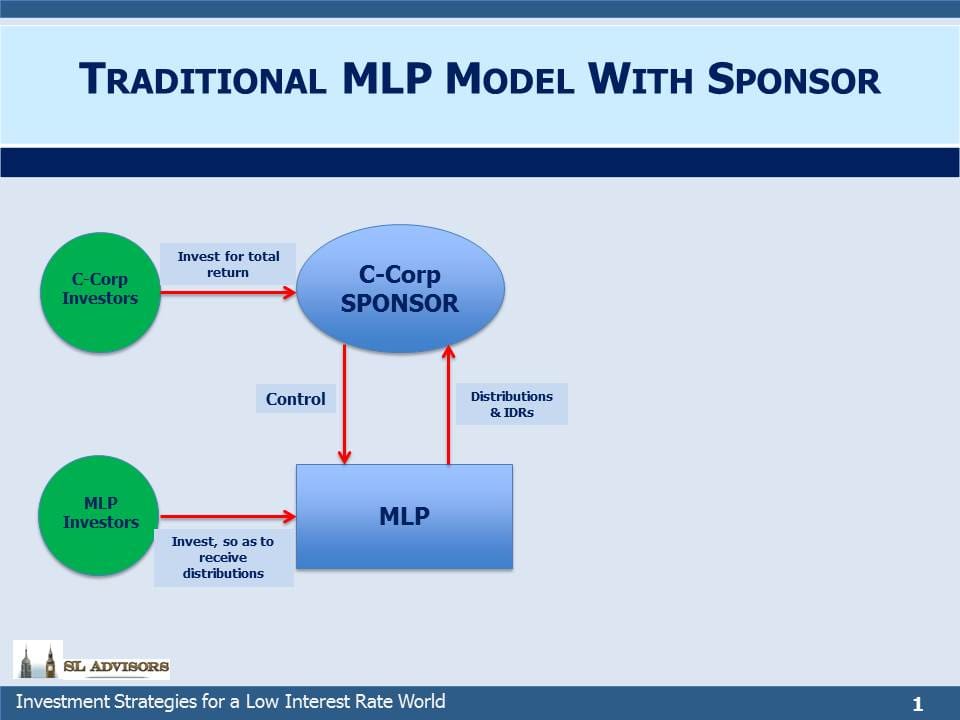

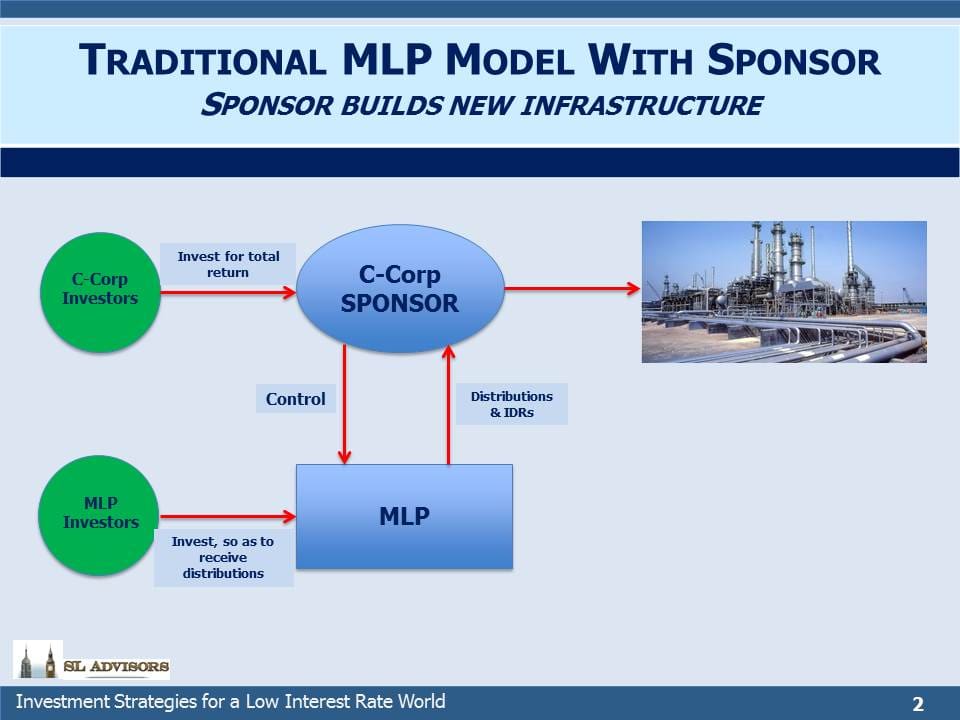

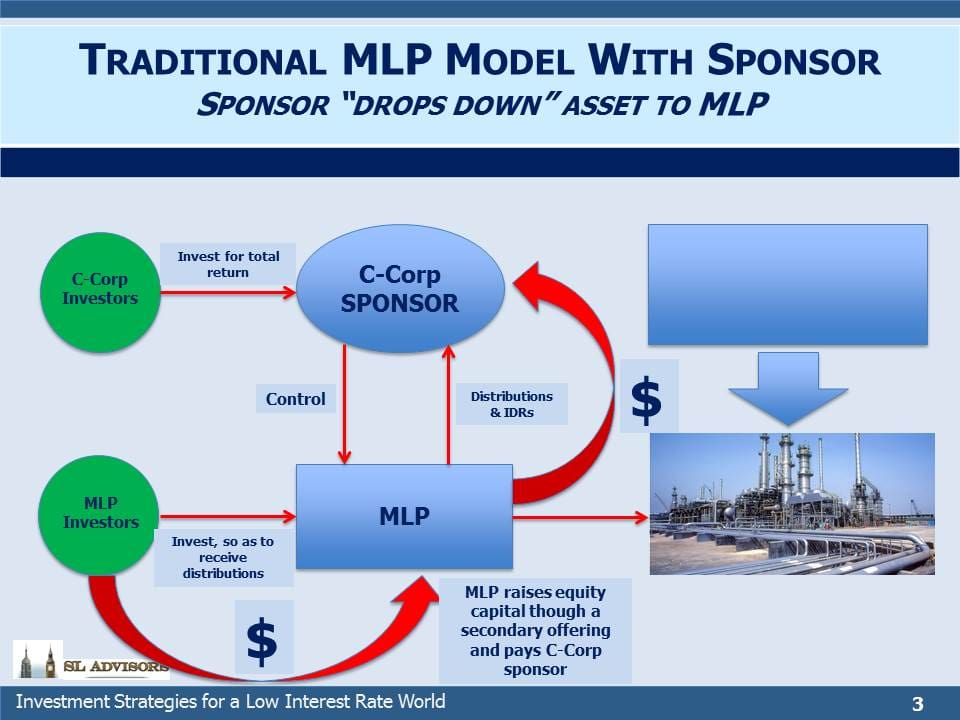

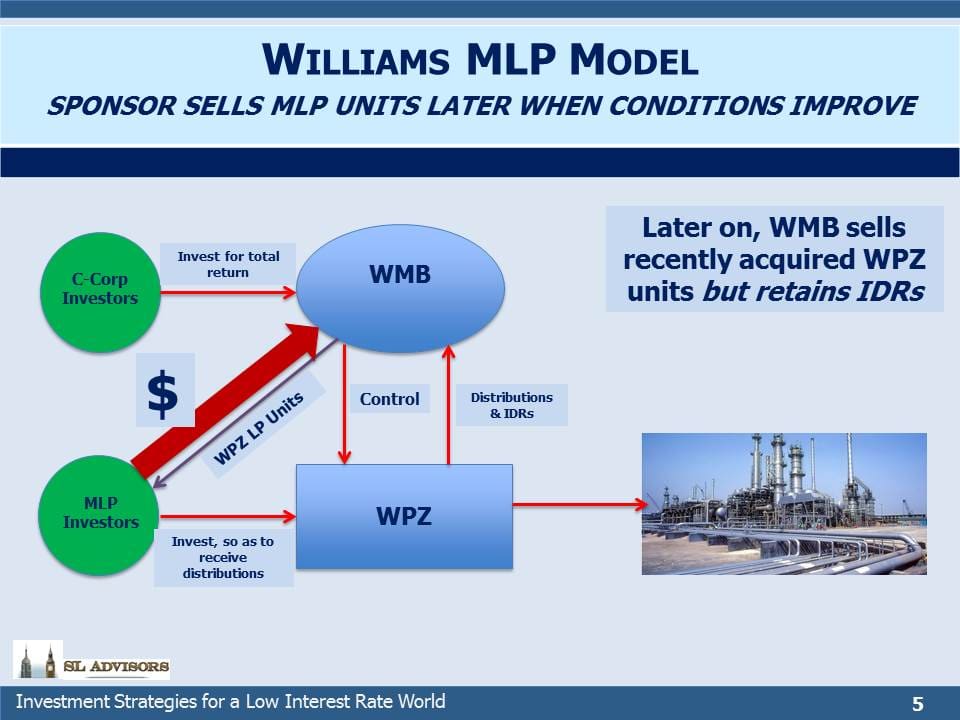

It reflects a different approach to the Sponsor/MLP model. Traditionally, the sponsor develops the assets and then sells them to its MLP through a “dropdown” transaction. The MLP raises capital through a secondary offering of equity (usually supplemented with debt) and uses the cash raised to pay its sponsor for the asset.

This model broke down last year as MLP yields rose to levels that made equity financing prohibitive. And yet, many attractive investment opportunities remained. It illustrates that the problem with midstream MLPs last year was not poor operating performance but a need for growth capital in excess of traditional investors’ desire to provide it (see The 2015 MLP Crash; Why and What’s Next).

Prior to the WMB dividend cut, WPZ yielded 9.7%, representing an expensive cost of equity capital. The 70% cut in WMB’s dividend will save $1.3BN annually. WMB expects to invest $1.7BN through the end of 2017 in new WPZ units. WPZ will use this cash to fund its capex, thereby eliminating its need to issue equity to the public and also taking pressure off its distribution.

WMB can in the future sell the WPZ units it will be acquiring through the next five quarters when the market environment is better and yields are lower. It’s an elegant way to provide WMB C-corp investors what they want (invested capital in high return projects) and WPZ investors what they want (stable distributions under any and all circumstances). Because the two classes of investors have different objectives, there are different times to access them for capital. Today the C-corp investor is more receptive, whereas MLP investors are setting a higher price. In time the cycle will shift, and the MLP investor will be a more eager capital provider, at which time WMB may sell its WPZ units. Crucially, the Incentive Distribution Rights (IDRs), under which WMB earns 50% of WPZ’s incremental Distributable Cash Flow (DCF) will remain with WMB even after the WPZ units are sold. It’s like a hedge fund manager investing his own cash in his hedge fund when investors are hard to find but opportunities attractive, and later on replacing his capital at a profit with outside investors’ money which will pay the ubiquitous “2 & 20”.

This is why it’s better to invest in MLP GPs.

We are invested in ETE and WMB

More on Solar

We received quite a few comments on our August newsletter (see Why Electric Cars Are Good for Fossil Fuels). We see solar-derived electricity generation growing at a high rate, but maintain that electric cars will for the foreseeable future consume electricity that is largely derived by burning natural gas and coal.

There are solar bulls who forecast that the sun will provide a substantial portion of our electricity in less than a generation (see Ray Kurzweil: Here’s Why Solar Will Dominate Energy Within 12 Years). Mr. Kurzweil’s Wikipedia page lists him as a computer scientist, inventor and futurist. He works for Google, so is a seriously smart guy.

So we won’t take on Mr. Kurzweil’s forecast directly; I’m personally a late adopter on most new things and on solar domination well, I’m just not quite there yet. But an important challenge for solar is that U.S. electricity consumption is barely growing, rising at 0.5% annually since 2000 according to the Energy Information Administration’s Annual Energy Outlook 2016. So to be significant quickly, solar will have to gain market share from traditional sources of electricity generation – and it is expected to gain at the expense of coal (as is natural gas). But to become the dominant source of electricity it will have to undercut many power stations that still have years of useful life ahead of them.

Moreover (as my partner Henry so insightfully noted), to do so they’ll need to deliver electricity not simply cheaper than the fully-loaded cost of a power plant but below its marginal cost. A nuclear power plant involves a high up-front cost to construct. Thereafter, its operating costs are the threshold for any new, competing source of electricity. As in micro-economics, once your fixed costs are spent, as long as you cover your variable costs you’ll keep producing widgets (or Megawatts). Power plants last for decades, so the openings for solar even if competitively priced will occur very slowly as less efficient plants are retired.

Furthermore, utilities and municipalities account for two thirds of U.S. gas transport capacity (pipelines) and sign long-dated volume & price commitments, making a quick switch ever more cost-prohibitive. Replacing retired coal capacity is how natural gas is making inroads into coal (although expensive environmental regulations are hastening the process). For these reasons and a lot of others specific to the intricacies of the electric utility sector (including load balancing and regulations), we think solar will grow and yet fail to be dominant for decades, similar to all past transformative energy technologies.

Important Disclosures

The information provided is for informational purposes only and investors should determine for themselves whether a particular service, security or product is suitable for their investment needs. The information contained herein is not complete, may not be current, is subject to change, and is subject to, and qualified in its entirety by, the more complete disclosures, risk factors and other terms that are contained in the disclosure, prospectus, and offering. Certain information herein has been obtained from third party sources and, although believed to be reliable, has not been independently verified and its accuracy or completeness cannot be guaranteed. No representation is made with respect to the accuracy, completeness or timeliness of this information. Nothing provided on this site constitutes tax advice. Individuals should seek the advice of their own tax advisor for specific information regarding tax consequences of investments. Investments in securities entail risk and are not suitable for all investors. This site is not a recommendation nor an offer to sell (or solicitation of an offer to buy) securities in the United States or in any other jurisdiction.

References to indexes and benchmarks are hypothetical illustrations of aggregate returns and do not reflect the performance of any actual investment. Investors cannot invest in an index and do not reflect the deduction of the advisor’s fees or other trading expenses. There can be no assurance that current investments will be profitable. Actual realized returns will depend on, among other factors, the value of assets and market conditions at the time of disposition, any related transaction costs, and the timing of the purchase. Indexes and benchmarks may not directly correlate or only partially relate to portfolios managed by SL Advisors as they have different underlying investments and may use different strategies or have different objectives than portfolios managed by SL Advisors (e.g. The Alerian index is a group MLP securities in the oil and gas industries. Portfolios may not include the same investments that are included in the Alerian Index. The S & P Index does not directly relate to investment strategies managed by SL Advisers.)

This site may contain forward-looking statements relating to the objectives, opportunities, and the future performance of the U.S. market generally. Forward-looking statements may be identified by the use of such words as; “believe,” “expect,” “anticipate,” “should,” “planned,” “estimated,” “potential” and other similar terms. Examples of forward-looking statements include, but are not limited to, estimates with respect to financial condition, results of operations, and success or lack of success of any particular investment strategy. All are subject to various factors, including, but not limited to general and local economic conditions, changing levels of competition within certain industries and markets, changes in interest rates, changes in legislation or regulation, and other economic, competitive, governmental, regulatory and technological factors affecting a portfolio’s operations that could cause actual results to differ materially from projected results. Such statements are forward-looking in nature and involves a number of known and unknown risks, uncertainties and other factors, and accordingly, actual results may differ materially from those reflected or contemplated in such forward-looking statements. Prospective investors are cautioned not to place undue reliance on any forward-looking statements or examples. None of SL Advisors LLC or any of its affiliates or principals nor any other individual or entity assumes any obligation to update any forward-looking statements as a result of new information, subsequent events or any other circumstances. All statements made herein speak only as of the date that they were made. r

Certain hyperlinks or referenced websites on the Site, if any, are for your convenience and forward you to third parties’ websites, which generally are recognized by their top level domain name. Any descriptions of, references to, or links to other products, publications or services does not constitute an endorsement, authorization, sponsorship by or affiliation with SL Advisors LLC with respect to any linked site or its sponsor, unless expressly stated by SL Advisors LLC. Any such information, products or sites have not necessarily been reviewed by SL Advisors LLC and are provided or maintained by third parties over whom SL Advisors LLC exercise no control. SL Advisors LLC expressly disclaim any responsibility for the content, the accuracy of the information, and/or quality of products or services provided by or advertised on these third-party sites.

All investment strategies have the potential for profit or loss. Different types of investments involve varying degrees of risk, and there can be no assurance that any specific investment will be suitable or profitable for a client’s investment portfolio.

Past performance of the American Energy Independence Index is not indicative of future returns.

Leave a Reply

Want to join the discussion?Feel free to contribute!