The Sand Rush

The resilience of the Shale Revolution in in the face of the 2015-16 oil price collapse is due in large part to dramatic improvements in productivity. Exploration and Production companies have strived to achieve more while using less of everything. Fewer rigs, for shorter times; less cement by drilling multiple wells on a pad; less water by recycling, and so on. But there’s one commodity whose volumes are growing substantially. Sand.

Hydraulic fracturing (“fracking”) involves pumping water combined with some other chemicals and sand (called “proppant”) into wells at high pressure. The rock cracks in millions of places as a result, and the sand allows the hydrocarbons to flow as the grains prop open these numerous cracks.

As fracking techniques have evolved, it’s turning out that more sand is better than less. Finer sand props open tinier cracks as well as being easier to transport. The need for more sand per well along with the increasing rig count have led to a big jump in sand use by the industry. A year ago I was at a dinner at which a senior executive from Antero Midstream (AM) described how this was playing out. Subsequently we’ve seen E&P companies such as Pioneer Natural Resources (PXD) note the advances made through increased sand utilization.

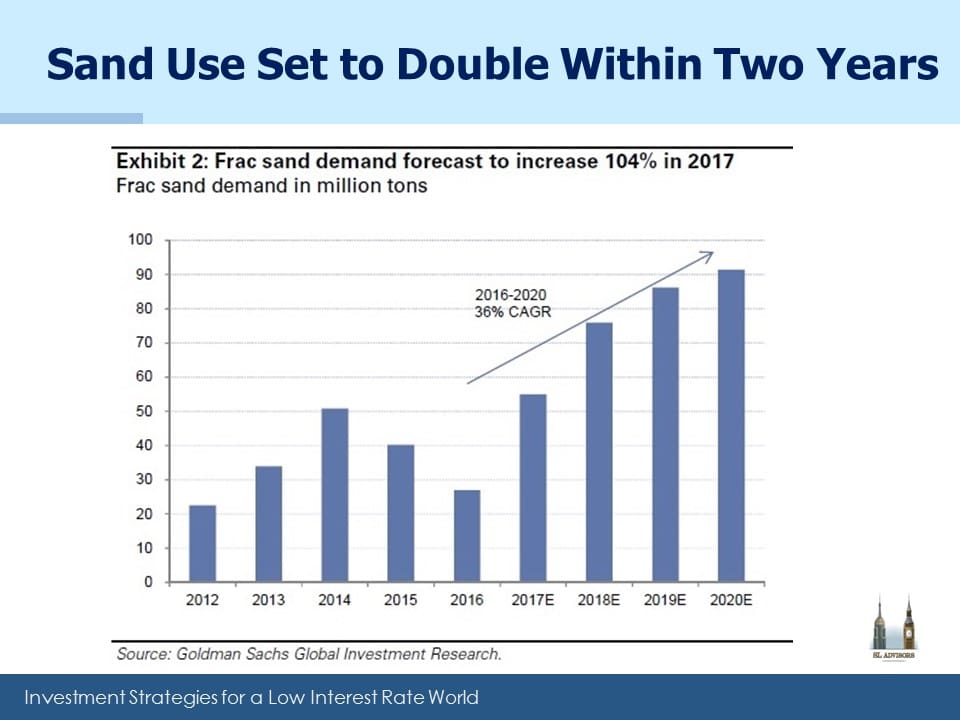

Goldman Sachs sees 36% annual growth in sand use by the industry, far faster than projections of oil and gas production. It means the price per ton of sand is increasing, and success for suppliers relies heavily on logistics.

Sand is heavy, so proximity to customers saves on transportation. Wisconsin is a key supplier of sand to the Bakken Shale in North Dakota. Illinois ships sand to the Permian in West Texas, although in-state Texan mine sources clearly have a big edge. Access to rail transportation is another key differentiator for suppliers, as are improvements in ease of delivery. Faster drop-off reduces truck waiting times and helps profitability. U.S. Silica (SLCA) is a leading supplier of sand to the oil and gas industry. They have positioned themselves as a consolidator in an industry still wrestling with too much debt. Their advantages include ready access to four large rail networks as well as substantial assets in Texas, both of which allow them to deliver sand more cheaply than their peers.

Last year SLCA acquired a company called Sandbox. Sandbox shipping containers allow for easier handling of sand, cutting delivery times as well as reducing the release of silica dust. SLCA has ambitious goals for their patented container technology, aiming to increase market share from 10% to 40-50%. Sandbox represents a form of vertical integration by SLCA using better technology as they seek wider margins in a tightening market. It’s one of the less well known stories in the Shale Revolution, but provides an example of the type of innovation that is driving increased output as we head towards Energy Independence. Notwithstanding its drop on Thursday following earnings, we continue to like its longer term prospects.

We are invested in SLCA

Important Disclosures

The information provided is for informational purposes only and investors should determine for themselves whether a particular service, security or product is suitable for their investment needs. The information contained herein is not complete, may not be current, is subject to change, and is subject to, and qualified in its entirety by, the more complete disclosures, risk factors and other terms that are contained in the disclosure, prospectus, and offering. Certain information herein has been obtained from third party sources and, although believed to be reliable, has not been independently verified and its accuracy or completeness cannot be guaranteed. No representation is made with respect to the accuracy, completeness or timeliness of this information. Nothing provided on this site constitutes tax advice. Individuals should seek the advice of their own tax advisor for specific information regarding tax consequences of investments. Investments in securities entail risk and are not suitable for all investors. This site is not a recommendation nor an offer to sell (or solicitation of an offer to buy) securities in the United States or in any other jurisdiction.

References to indexes and benchmarks are hypothetical illustrations of aggregate returns and do not reflect the performance of any actual investment. Investors cannot invest in an index and do not reflect the deduction of the advisor’s fees or other trading expenses. There can be no assurance that current investments will be profitable. Actual realized returns will depend on, among other factors, the value of assets and market conditions at the time of disposition, any related transaction costs, and the timing of the purchase. Indexes and benchmarks may not directly correlate or only partially relate to portfolios managed by SL Advisors as they have different underlying investments and may use different strategies or have different objectives than portfolios managed by SL Advisors (e.g. The Alerian index is a group MLP securities in the oil and gas industries. Portfolios may not include the same investments that are included in the Alerian Index. The S & P Index does not directly relate to investment strategies managed by SL Advisers.)

This site may contain forward-looking statements relating to the objectives, opportunities, and the future performance of the U.S. market generally. Forward-looking statements may be identified by the use of such words as; “believe,” “expect,” “anticipate,” “should,” “planned,” “estimated,” “potential” and other similar terms. Examples of forward-looking statements include, but are not limited to, estimates with respect to financial condition, results of operations, and success or lack of success of any particular investment strategy. All are subject to various factors, including, but not limited to general and local economic conditions, changing levels of competition within certain industries and markets, changes in interest rates, changes in legislation or regulation, and other economic, competitive, governmental, regulatory and technological factors affecting a portfolio’s operations that could cause actual results to differ materially from projected results. Such statements are forward-looking in nature and involves a number of known and unknown risks, uncertainties and other factors, and accordingly, actual results may differ materially from those reflected or contemplated in such forward-looking statements. Prospective investors are cautioned not to place undue reliance on any forward-looking statements or examples. None of SL Advisors LLC or any of its affiliates or principals nor any other individual or entity assumes any obligation to update any forward-looking statements as a result of new information, subsequent events or any other circumstances. All statements made herein speak only as of the date that they were made. r

Certain hyperlinks or referenced websites on the Site, if any, are for your convenience and forward you to third parties’ websites, which generally are recognized by their top level domain name. Any descriptions of, references to, or links to other products, publications or services does not constitute an endorsement, authorization, sponsorship by or affiliation with SL Advisors LLC with respect to any linked site or its sponsor, unless expressly stated by SL Advisors LLC. Any such information, products or sites have not necessarily been reviewed by SL Advisors LLC and are provided or maintained by third parties over whom SL Advisors LLC exercise no control. SL Advisors LLC expressly disclaim any responsibility for the content, the accuracy of the information, and/or quality of products or services provided by or advertised on these third-party sites.

All investment strategies have the potential for profit or loss. Different types of investments involve varying degrees of risk, and there can be no assurance that any specific investment will be suitable or profitable for a client’s investment portfolio.

Past performance of the American Energy Independence Index is not indicative of future returns.

“Finer sand is easier to transport”? I’m not certain what you mean by finer sand. Finer than what? Fine sand to me , is silica dust, which can set up a static charge and cling to anything,making it difficult to handle.

Goldman reports that E&P companies prefer finer grades of sand because it’s easier to use as they evolve towards longer laterals with larger fracking jobs.