How to Short A Stock and Get Others to Join You

Although the equity research business is dominated by large, sell-side firms hoping to generate trading commissions from their (usually bullish) recommendations, there are alternate business models out there. Prescience Point is a hitherto unheard of research firm with no known location (so presumably outside the U.S. since they’re not registered) and no publicly disclosed employees. They focus on research uncovering companies’ fraudulent activities. Although they write about what they find, so as to (presumably) sell their research to subscribers, they also short the stocks they cover.

Short sellers are a fascinating bunch. The odds are stacked against them. Company managements and sell side research (both of which are generally bullish) are in the opposite corner from them. In addition, short positions have almost unlimited potential loss with gains limited by the proceeds received for the sale of the stock. Markets generally rise over time, so these headwinds to success mean that short sellers need to carry out pretty detailed work, and they need to be right.

What Prescience can do (based on their website) is:

(1) Produce a bearish report

(2) Share it privately with paying subscribers

(3) Short the stock themselves prior to its public release

(4) Buy back the shorted stock when the report is out

Chicago Bridge and Iron (CBI) is a $7.5 billion market cap company that builds energy infrastructure. Nuclear plants, oil pipelines, LNG plants (for transporting liquid natural gas) and other related projects. Their contracts are lumpy since completion can take many years. They recently acquired a competitor, Shaw Group, almost doubling their revenues.

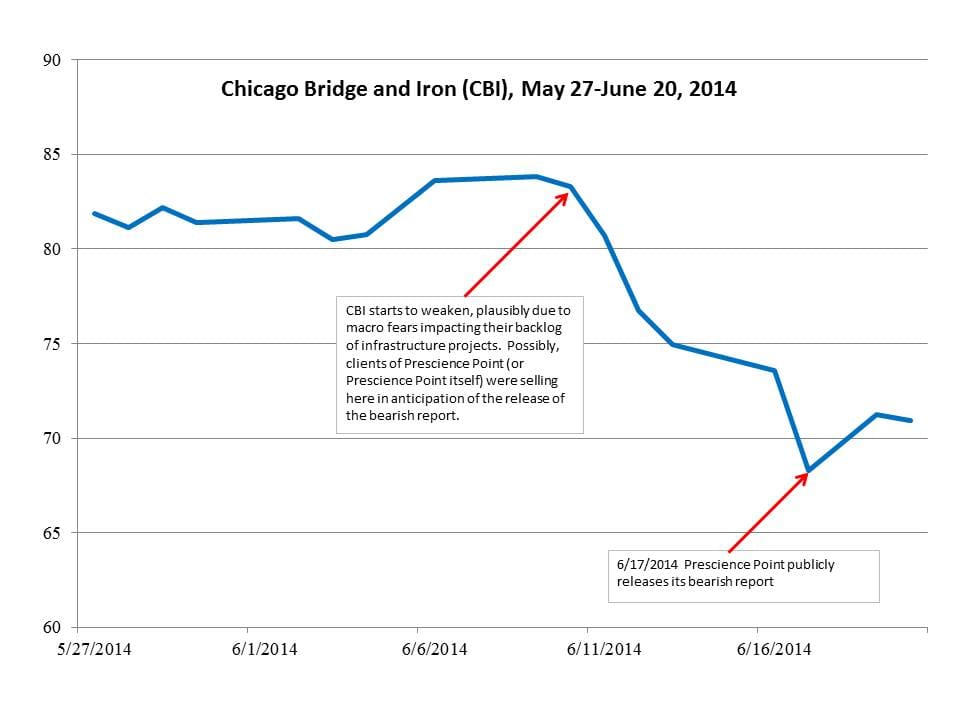

CBI’s stock recently behaved as if Prescience had imposed its business model described above on it. When CBI began to weaken in early June on no apparent news, we assumed perhaps investors were becoming more wary of their backlog of infrastructure orders given the developing tumult in the Middle East. The stock weakened further (as shown in the chart below) until Prescience released their report. At this point reasons for the earlier weakness became clear, and additional sellers unwilling to subscribe but now finally aware of the report’s insight, were convinced to sell.

There doesn’t seem to be anything illegal with this. In any event, Prescience appears to be outside the U.S. and their website is pretty clear in warning that they trade both before and after releasing their reports. And it’s not obvious that there’s even anything wrong with what they’re doing. They have a point of view; they share it with clients; they act on it; they publicize their view. And they tell you this is what they’re doing.

In fact, their research doesn’t even need to be right. To be valuable, all that’s required is for the stock price to drop after Prescience and its clients have sold. What’s needed is a group of sellers who will sell after the report is public, for it’s this last drop that creates the profit opportunity. As long as there are enough uninformed sellers willing to sell the stock on the public release of the report so that the earlier, informed sellers can cover their positions, the business model will work. This presumably limits the number of subscribers because too many of them might cause the stock to rally on the report’s publication as they overwhelmed the fewer sellers involved. It’s quite an interesting business model; not quite God’s Work, as Goldman’s CEO Lloyd Blankfein so regrettably once described what his company does, but it’s a living of sorts I guess.

We’ve held a small long position in CBI for some time. We were puzzled by the early June sell off, but when the report was published on June 17th,the reason for the stock’s weakness became clear. Warren Buffett has famously said that in a poker game, if you don’t know who the patsy is, you’re the patsy. June 17th was a day during which we guess that patsies were unusually active in CBI. We just don’t know if the patsies were the sellers (late to the party, having missed the opportunity to sell at higher prices during the prior few days) or the buyers (willfully ignoring the now public short thesis offered by Prescience).

For our part, we didn’t find much compelling in their report and so bought more CBI on June 17th. We just don’t know yet if we’re the patsies or not.

Important Disclosures

The information provided is for informational purposes only and investors should determine for themselves whether a particular service, security or product is suitable for their investment needs. The information contained herein is not complete, may not be current, is subject to change, and is subject to, and qualified in its entirety by, the more complete disclosures, risk factors and other terms that are contained in the disclosure, prospectus, and offering. Certain information herein has been obtained from third party sources and, although believed to be reliable, has not been independently verified and its accuracy or completeness cannot be guaranteed. No representation is made with respect to the accuracy, completeness or timeliness of this information. Nothing provided on this site constitutes tax advice. Individuals should seek the advice of their own tax advisor for specific information regarding tax consequences of investments. Investments in securities entail risk and are not suitable for all investors. This site is not a recommendation nor an offer to sell (or solicitation of an offer to buy) securities in the United States or in any other jurisdiction.

References to indexes and benchmarks are hypothetical illustrations of aggregate returns and do not reflect the performance of any actual investment. Investors cannot invest in an index and do not reflect the deduction of the advisor’s fees or other trading expenses. There can be no assurance that current investments will be profitable. Actual realized returns will depend on, among other factors, the value of assets and market conditions at the time of disposition, any related transaction costs, and the timing of the purchase. Indexes and benchmarks may not directly correlate or only partially relate to portfolios managed by SL Advisors as they have different underlying investments and may use different strategies or have different objectives than portfolios managed by SL Advisors (e.g. The Alerian index is a group MLP securities in the oil and gas industries. Portfolios may not include the same investments that are included in the Alerian Index. The S & P Index does not directly relate to investment strategies managed by SL Advisers.)

This site may contain forward-looking statements relating to the objectives, opportunities, and the future performance of the U.S. market generally. Forward-looking statements may be identified by the use of such words as; “believe,” “expect,” “anticipate,” “should,” “planned,” “estimated,” “potential” and other similar terms. Examples of forward-looking statements include, but are not limited to, estimates with respect to financial condition, results of operations, and success or lack of success of any particular investment strategy. All are subject to various factors, including, but not limited to general and local economic conditions, changing levels of competition within certain industries and markets, changes in interest rates, changes in legislation or regulation, and other economic, competitive, governmental, regulatory and technological factors affecting a portfolio’s operations that could cause actual results to differ materially from projected results. Such statements are forward-looking in nature and involves a number of known and unknown risks, uncertainties and other factors, and accordingly, actual results may differ materially from those reflected or contemplated in such forward-looking statements. Prospective investors are cautioned not to place undue reliance on any forward-looking statements or examples. None of SL Advisors LLC or any of its affiliates or principals nor any other individual or entity assumes any obligation to update any forward-looking statements as a result of new information, subsequent events or any other circumstances. All statements made herein speak only as of the date that they were made. r

Certain hyperlinks or referenced websites on the Site, if any, are for your convenience and forward you to third parties’ websites, which generally are recognized by their top level domain name. Any descriptions of, references to, or links to other products, publications or services does not constitute an endorsement, authorization, sponsorship by or affiliation with SL Advisors LLC with respect to any linked site or its sponsor, unless expressly stated by SL Advisors LLC. Any such information, products or sites have not necessarily been reviewed by SL Advisors LLC and are provided or maintained by third parties over whom SL Advisors LLC exercise no control. SL Advisors LLC expressly disclaim any responsibility for the content, the accuracy of the information, and/or quality of products or services provided by or advertised on these third-party sites.

All investment strategies have the potential for profit or loss. Different types of investments involve varying degrees of risk, and there can be no assurance that any specific investment will be suitable or profitable for a client’s investment portfolio.

Past performance of the American Energy Independence Index is not indicative of future returns.

Plenty of other investors are into this old act, publicizing research of both long and short positions after they’ve been taken. I think that’s ok, though the ethics do seem to be challenged when the shorts attempt to attack though the regulatory process as in MBI, QCOR, HLF or WRLD.