Why the Fed Likes Bonds a Little More

The chart above doesn’t look like much, but it represents a snapshot of the thinking of the Federal Open Market Committee (FOMC) on interest rates. Their communication has come a long way since the days of cigar-chomping Paul Volcker in the 1970s, when they went out of their way to disguise their intentions. Alan Greenspan inherited this culture and while in his early years he clearly relished confounding Senators with his unintelligible responses during Congressional testimony, over time he initiated a move towards greater transparency around the Fed’s decision making process and objectives. Ben Bernanke continued this and no doubt the trend will be maintained under Janet Yellen.

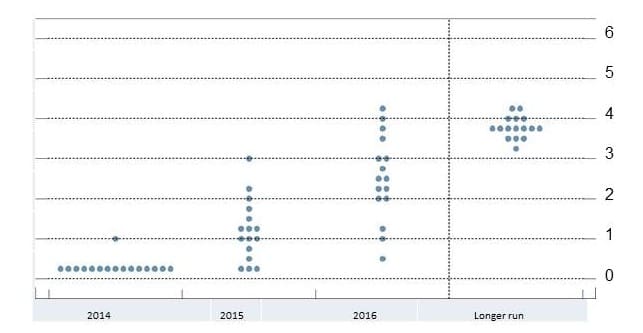

On the chart above (reproduced from the Fed’s website), each dot represents the view of a single FOMC member on the year-end level for short term interest rates (specifically, the Fed Funds rate). There are 16 voting members and each provides a forecast for the end of this year, 2015, 2016 and the long term. I’ve been watching these releases for nearly three years because over time they provide a fascinating picture of their evolving interest rate views.

The first three annual forecasts (2014-2016) can almost be used to construct a yield curve. Indeed, interest rate futures contracts are now often described as priced above or below the Fed’s forecast. Of course, their rate forecast can be wrong, just as the economic forecasts on which it’s based can be. Circumstances change, and there’s nothing intended to be inflexible about these figures. But it does allow us to see more clearly whether economic events alter their view. For example, U.S. GDP growth in the first quarter was quite weak at -1.5%, due largely to the harsh winter those of us in the north east endured. However, the FOMC has a reasonably positive view of growth for the remainder of the year (2.1%-2.3% for all of 2014 which implies around 3.4% on average for the remaining three quarters). As a result, they very modestly tweaked their rate forecasts higher over 2015-2016 (by about 0.07%-0.10%).

More significantly in my view, their long run forecast of interest rates fell from 4.0% to 3.75%. This is the equilibrium rate at which they think rates should settle assuming they had no bias to run monetary policy with either an accomodative bias (as it is now) or a restrictive one. 3.75% is neutral. It takes account of their long run estimate of inflation and of GDP growth.

Back in early 2012, their median long run forecast for rates was 4% and they raised it to 4.25%. They brought it back down to 4% last Summer and then 3.75% yesterday. If their forecast is right (and their forecasts are more important than anybody else’s) it means the fair value yield for, say, a ten year treasury security is a little lower. An investor now ought to be willing to hold it at a somewhat lower yield than before since in theory a ten year bond represents roughly the average short term yield over that period of time.

Steve Liesman from CNBC picked up on this and asked Janet Yellen in her press conference yesterday what was behind this shift. She noted that the composition of the FOMC had changed since the last forecast in March which might make the comparison less meaningful (two voting members were replaced according to a rotating schedule). But she conceded that it also probably reflected a more modest view of long term GDP potential in the U.S. economy.

For investors, it confirms what we’ve long felt, which is that interest rates are likely to stay relatively low for a long time. The Fed’s not about to make bonds more attractive by pushing rates sharply higher, so they will remain a fairly unattractive investment choice. And while you can’t infer too much about equities from the Fed’s interest rate view, it still seems likely that stocks will provide superior long term returns compared with bonds over the medium term.

Important Disclosures

The information provided is for informational purposes only and investors should determine for themselves whether a particular service, security or product is suitable for their investment needs. The information contained herein is not complete, may not be current, is subject to change, and is subject to, and qualified in its entirety by, the more complete disclosures, risk factors and other terms that are contained in the disclosure, prospectus, and offering. Certain information herein has been obtained from third party sources and, although believed to be reliable, has not been independently verified and its accuracy or completeness cannot be guaranteed. No representation is made with respect to the accuracy, completeness or timeliness of this information. Nothing provided on this site constitutes tax advice. Individuals should seek the advice of their own tax advisor for specific information regarding tax consequences of investments. Investments in securities entail risk and are not suitable for all investors. This site is not a recommendation nor an offer to sell (or solicitation of an offer to buy) securities in the United States or in any other jurisdiction.

References to indexes and benchmarks are hypothetical illustrations of aggregate returns and do not reflect the performance of any actual investment. Investors cannot invest in an index and do not reflect the deduction of the advisor’s fees or other trading expenses. There can be no assurance that current investments will be profitable. Actual realized returns will depend on, among other factors, the value of assets and market conditions at the time of disposition, any related transaction costs, and the timing of the purchase. Indexes and benchmarks may not directly correlate or only partially relate to portfolios managed by SL Advisors as they have different underlying investments and may use different strategies or have different objectives than portfolios managed by SL Advisors (e.g. The Alerian index is a group MLP securities in the oil and gas industries. Portfolios may not include the same investments that are included in the Alerian Index. The S & P Index does not directly relate to investment strategies managed by SL Advisers.)

This site may contain forward-looking statements relating to the objectives, opportunities, and the future performance of the U.S. market generally. Forward-looking statements may be identified by the use of such words as; “believe,” “expect,” “anticipate,” “should,” “planned,” “estimated,” “potential” and other similar terms. Examples of forward-looking statements include, but are not limited to, estimates with respect to financial condition, results of operations, and success or lack of success of any particular investment strategy. All are subject to various factors, including, but not limited to general and local economic conditions, changing levels of competition within certain industries and markets, changes in interest rates, changes in legislation or regulation, and other economic, competitive, governmental, regulatory and technological factors affecting a portfolio’s operations that could cause actual results to differ materially from projected results. Such statements are forward-looking in nature and involves a number of known and unknown risks, uncertainties and other factors, and accordingly, actual results may differ materially from those reflected or contemplated in such forward-looking statements. Prospective investors are cautioned not to place undue reliance on any forward-looking statements or examples. None of SL Advisors LLC or any of its affiliates or principals nor any other individual or entity assumes any obligation to update any forward-looking statements as a result of new information, subsequent events or any other circumstances. All statements made herein speak only as of the date that they were made. r

Certain hyperlinks or referenced websites on the Site, if any, are for your convenience and forward you to third parties’ websites, which generally are recognized by their top level domain name. Any descriptions of, references to, or links to other products, publications or services does not constitute an endorsement, authorization, sponsorship by or affiliation with SL Advisors LLC with respect to any linked site or its sponsor, unless expressly stated by SL Advisors LLC. Any such information, products or sites have not necessarily been reviewed by SL Advisors LLC and are provided or maintained by third parties over whom SL Advisors LLC exercise no control. SL Advisors LLC expressly disclaim any responsibility for the content, the accuracy of the information, and/or quality of products or services provided by or advertised on these third-party sites.

All investment strategies have the potential for profit or loss. Different types of investments involve varying degrees of risk, and there can be no assurance that any specific investment will be suitable or profitable for a client’s investment portfolio.

Past performance of the American Energy Independence Index is not indicative of future returns.

Leave a Reply

Want to join the discussion?Feel free to contribute!