Rate Hike Or Not, The Same Problems Persist

On May 22, 2013 then-Fed chairman Ben Bernanke inadvertently added “taper tantrum” to the lexicon of terms used to describe the impact of the Fed’s activities. That date marks the formal beginning of the Fed’s efforts to prepare financial markets for an eventual tightening of policy — or the start of the removal of accommodative policy, to use their description. In the belief that transparent policy deliberations reduce the possibility of a monetary surprise with its consequent financial market upheaval, the Fed’s public statements, release of projections and even the ubiquitous “blue dots” showing the rate forecast of each FOMC member have all been provided to help us. In fact, for almost four years I’ve been constructing an “FOMC Futures Curve”, which is what short term interest rate futures would look like if FOMC members were the only participants. It’s been absorbing for brief moments around four times a year when they provide updated information. Many might find it a nerdy preoccupation, but having spent a good part of my career in Fed-engineered darkness over their intentions, the shift to greater openness begun under Greenspan has been fascinating.

Forward guidance presumably is intended to let us know what the Fed will do before they do it. As we head into a two-day FOMC meeting on September 16-17, opinions are evenly split about whether they’ll raise rates. Perhaps we ought not to be surprised in either outcome, but it seems to me that if there’s no consensus after years of openness, the communication strategy has failed. The problem with providing meaningful forward guidance is that it involves a commitment, and a commitment reduces your ability to change your mind. The window into the Fed’s deliberations has simply revealed that they want to retain maximum flexibility until the day they meet. Announcing a hike with a delayed effective date would soften the blow (see Advice for the Fed) but it’s too late for that.

Following the FOMC’s announcement and the elimination of near term uncertainty, investors will be faced with the same dilemma as before: how are they to invest so as to preserve the purchasing power of their assets after taxes and inflation? Whether ten year treasury yields move up 0.25% or not this week, the paucity of assets offering acceptable returns will remain Dilemma #1.

Suppose a taxable investor visits her financial advisor with the objective of constructing a portfolio with a 6% return and moderate risk. Assuming our investor is facing a 30% average tax rate (combination of Federal and state taxes on capital gains, dividends and ordinary income), a pre-tax 6% is 4.2% afterwards. 2% inflation (the Fed’s target) knocks that return down to 2.2%. Then there are the advisor’s fees, and the possibility that returns won’t be as hoped. 6% doesn’t seem that demanding given all of this, and yet the building blocks with which to achieve it are limited.

Public equities yield around 2%, and assuming the fifty-year average dividend growth rate of 5% prevails (for a total return of 7%), stocks clearly are part of the portfolio. Bonds (as defined by the iShares Aggregate Bond ETF which tracks the Barclays Aggregate Index) yield 2.4%. Since the yield at which you buy a bond heavily impacts your total return, it’s going to be hard to do much better than 2.4% with investment grade debt. Moreover, the ability of bonds to offset a falling equity market is limited given their already low yields. Backward-looking models may justify them, but to us they look like returnless risk. Moving up the risk spectrum to High Yield gets you 5.5% (as defined by the iShares High Yield Corporate Bond ETF). There is some chance for capital appreciation — but this year capital losses have more than wiped out coupon income reflecting the preponderance of energy names in the index.

REITs yield 4.4% (as defined by the Vanguard REIT ETF), and this, combined with some modest growth may deliver a return that at least equals the investor’s 6% target.

Regular readers can by now guess where this is going. The Alerian MLP Index, yields 7.25%, and MLP distributions even grew in 2009 following the financial crisis. However, MLPs are down 23% so far in 2015. In fact, they’ve fallen that much since the end of April, creating an unpleasant backdrop to an otherwise glorious Summer for anyone more than tangentially involved.

There is a bear story to MLPs, as those prescient enough to sell at the highs of August 2014 well know. A 33% drop can’t happen without a fundamental story, and the collapse in oil is challenging the expected production growth of U.S. shale plays with its attendant reduction in needed infrastructure. The growth story that has driven MLP prices is in doubt.

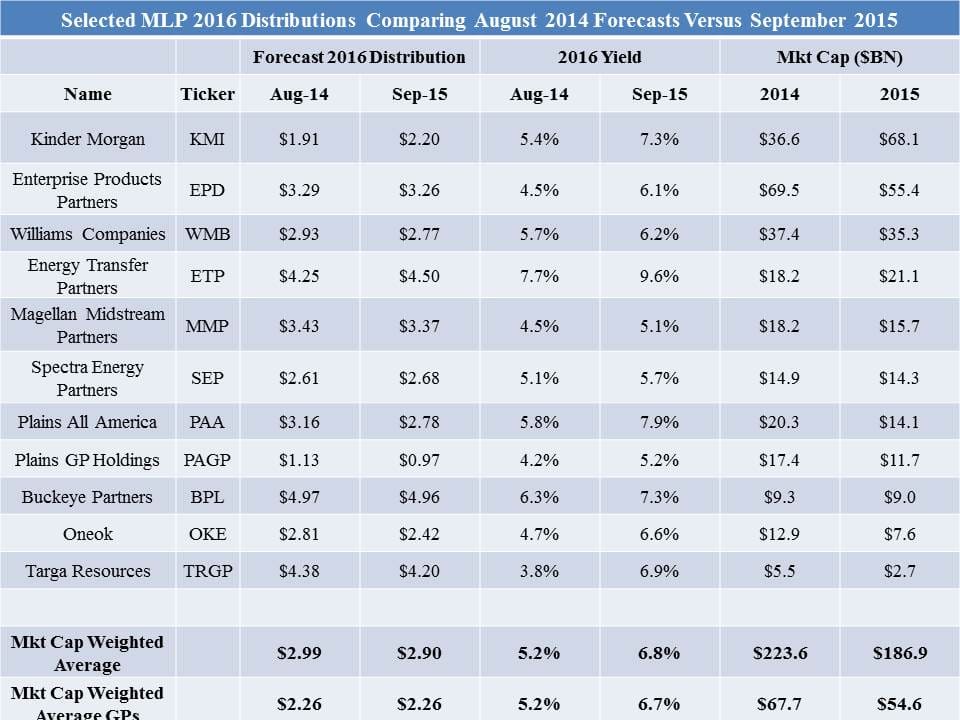

It’s therefore instructive to examine metrics on a number of businesses as they were in August 2014 and how they appear today. The table below shows forecasts for 2016 distributions from selected MLPs (chosen unscientifically because we are invested in them or the General Partners that control them), and shows how those 2016 forecast distributions have changed from the market peak in MLPs 13 months ago to now. The data is from JPMorgan but such figures are typically heavily influenced by company guidance.

Looking at the numbers, you certainly wouldn’t think we’d seen a collapse in oil. The 2016 forecast distribution for this group is modestly lower at $2.90 (cap-weighted) versus $2.99 a year ago. The market cap of these companies (excluding Kinder Morgan since during the intervening period it combined with its two outstanding MLPs to create a substantially larger entity) has fallen by 16%, hence the 2016 yield has risen from 5.2% to 6.8%. Just looking at the General Partners in this group (KMI, OKE, PAGP and WMB) provides a similar result. The operations of these firms and their cashflow generating abilities have on average not shifted that much. Plains All America (PAA) and its GP (PAGP) have seen forecast reductions because of their crude oil exposure. The same is true of Oneok (OKE).

But overall, the fall in their security prices has simply driven up their yields. These names are representative — they’re all midstream, which is to say they operate toll-like business midels with limited direct commodity exposure. There are MLPs concentrated in Exploration & Production (upstream) and others that run refineries (variable distribution MLPs), but we don’t care about those.

So for the investor seeking a 6% portfolio return, the most compelling reason to exclude MLPs is the 23% drop since April which has made few people happy. However, looking beyond the undoubted voting by many investors who have abandoned the sector, 7% yields combined with 8-9% growth rates (the cap-weighted forecast on the group of names listed) seems pretty compelling for long-term investors willing to look beyond recent price action and focus on the fundamentals by including MLPs, perhaps even with an overweight, in their portfolios.

Important Disclosures

The information provided is for informational purposes only and investors should determine for themselves whether a particular service, security or product is suitable for their investment needs. The information contained herein is not complete, may not be current, is subject to change, and is subject to, and qualified in its entirety by, the more complete disclosures, risk factors and other terms that are contained in the disclosure, prospectus, and offering. Certain information herein has been obtained from third party sources and, although believed to be reliable, has not been independently verified and its accuracy or completeness cannot be guaranteed. No representation is made with respect to the accuracy, completeness or timeliness of this information. Nothing provided on this site constitutes tax advice. Individuals should seek the advice of their own tax advisor for specific information regarding tax consequences of investments. Investments in securities entail risk and are not suitable for all investors. This site is not a recommendation nor an offer to sell (or solicitation of an offer to buy) securities in the United States or in any other jurisdiction.

References to indexes and benchmarks are hypothetical illustrations of aggregate returns and do not reflect the performance of any actual investment. Investors cannot invest in an index and do not reflect the deduction of the advisor’s fees or other trading expenses. There can be no assurance that current investments will be profitable. Actual realized returns will depend on, among other factors, the value of assets and market conditions at the time of disposition, any related transaction costs, and the timing of the purchase. Indexes and benchmarks may not directly correlate or only partially relate to portfolios managed by SL Advisors as they have different underlying investments and may use different strategies or have different objectives than portfolios managed by SL Advisors (e.g. The Alerian index is a group MLP securities in the oil and gas industries. Portfolios may not include the same investments that are included in the Alerian Index. The S & P Index does not directly relate to investment strategies managed by SL Advisers.)

This site may contain forward-looking statements relating to the objectives, opportunities, and the future performance of the U.S. market generally. Forward-looking statements may be identified by the use of such words as; “believe,” “expect,” “anticipate,” “should,” “planned,” “estimated,” “potential” and other similar terms. Examples of forward-looking statements include, but are not limited to, estimates with respect to financial condition, results of operations, and success or lack of success of any particular investment strategy. All are subject to various factors, including, but not limited to general and local economic conditions, changing levels of competition within certain industries and markets, changes in interest rates, changes in legislation or regulation, and other economic, competitive, governmental, regulatory and technological factors affecting a portfolio’s operations that could cause actual results to differ materially from projected results. Such statements are forward-looking in nature and involves a number of known and unknown risks, uncertainties and other factors, and accordingly, actual results may differ materially from those reflected or contemplated in such forward-looking statements. Prospective investors are cautioned not to place undue reliance on any forward-looking statements or examples. None of SL Advisors LLC or any of its affiliates or principals nor any other individual or entity assumes any obligation to update any forward-looking statements as a result of new information, subsequent events or any other circumstances. All statements made herein speak only as of the date that they were made. r

Certain hyperlinks or referenced websites on the Site, if any, are for your convenience and forward you to third parties’ websites, which generally are recognized by their top level domain name. Any descriptions of, references to, or links to other products, publications or services does not constitute an endorsement, authorization, sponsorship by or affiliation with SL Advisors LLC with respect to any linked site or its sponsor, unless expressly stated by SL Advisors LLC. Any such information, products or sites have not necessarily been reviewed by SL Advisors LLC and are provided or maintained by third parties over whom SL Advisors LLC exercise no control. SL Advisors LLC expressly disclaim any responsibility for the content, the accuracy of the information, and/or quality of products or services provided by or advertised on these third-party sites.

All investment strategies have the potential for profit or loss. Different types of investments involve varying degrees of risk, and there can be no assurance that any specific investment will be suitable or profitable for a client’s investment portfolio.

Past performance of the American Energy Independence Index is not indicative of future returns.

Leave a Reply

Want to join the discussion?Feel free to contribute!