America Is Great!

| Back in 2014 they were unlikely adversaries. Saudi Energy Minister Ali Al-Naimi, and Pioneer Natural Resources (PXD) CEO Scott Sheffield (pictured below) had both made their careers in the oil business. They had each spent formative years abroad, with Al-Naimi attending Lehigh University and Sheffield going to high school in Iran (his father worked for Atlantic Richfield). Both were dedicated to maximizing the value of the fossil fuels they controlled, and had hunted together (a common pastime for oilmen).

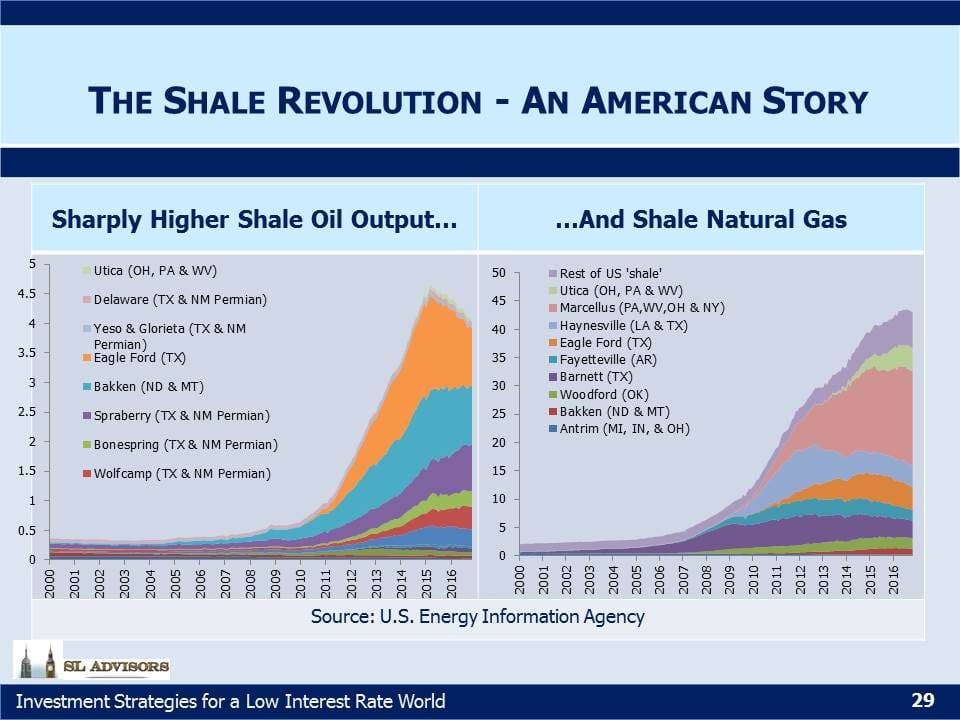

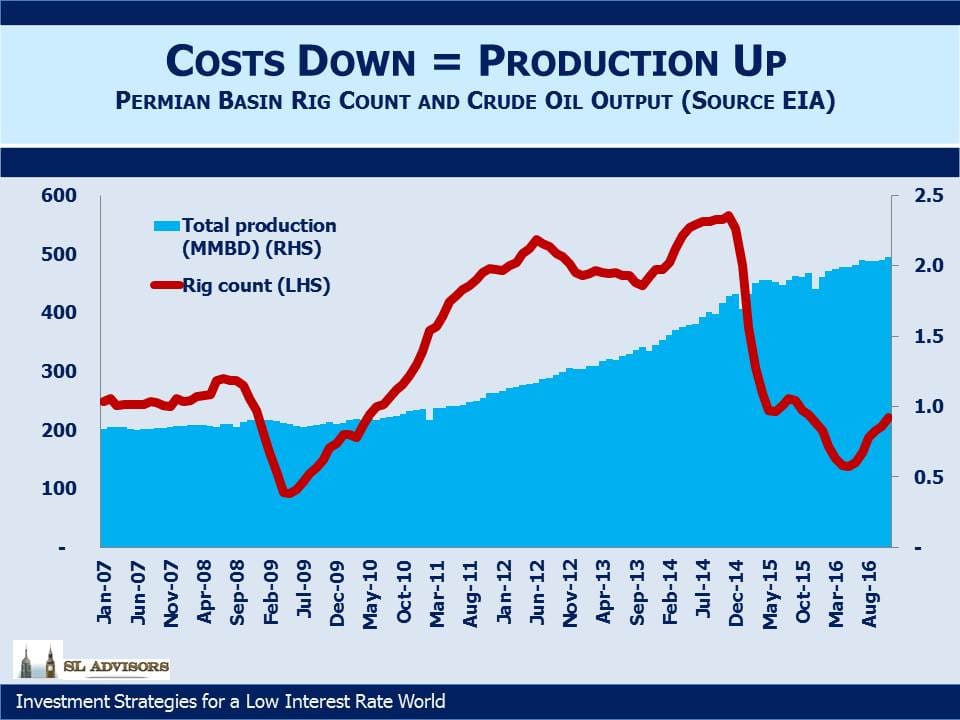

But t So it was that in late 2014 the Saudis shocked the oil market by promising to increase production into an already oversupplied market, rather than adopt their familiar role of swing producer, modifying their own output to smooth price swings. They calculated that lower prices would bankrupt large swathes of the U.S. shale oil industry, eventually cutting production and allowing prices to return to the $100+ levels necessary to support Saudi Arabia’s budget. “We are going to continue to produce what we are producing, we are going to continue to welcome additional production if customers come and ask for it,” al-Naimi said.  What followed over the next two years is one of the most extraordinary stories of private sector innovation in the biggest, most dynamic economy the world has ever seen. Crude prices plummeted, falling as low as $26 a barrel on February 11th, 2016. Facing an existential threat to their businesses, Pioneer and many companies like it drove production costs down relentlessly, bringing break-evens down to levels few had thought possible. This is most obvious in metrics such as the rig count, whose 75% fall led to only a relatively modest drop in production as the best rigs were employed for shorter periods at lower rates. Moreover, individual well productivity improved as longer laterals focused on sweet spots increased output. The composition of proppant was refined. Sand keeps the cracks open that fracking creates, and finer grains in greater volumes further increased output. Service providers were squeezed to reduce their costs and idle less efficient equipment. The industry staggered for a while under the body blow of lower prices, and many overleveraged companies failed. But overall it stayed on its feet, adapted to the new world and maintained oil production at levels substantially higher than prior to the Shale Revolution. Although prices bounced from $26, they remained persistently lower than many OPEC countries (including most notably Saudi Arabia) needed to balance their budgets. In 2015 the Saudis ran a deficit equal to 15% of GDP and resorted to issuing bonds to fund expenses. Sharp spending cuts followed. Drilling budgets around the world were slashed, and an estimated $1TN was cut from planned capex out to 2020. As the failure of Al-Naimi’s strategy became apparent, he was replaced in May of 2016. The Saudis still plan to sell shares in their giant oil company Saudi Aramco, so in choosing its chief, Khalid Al-Falih, as their next Oil Minister, they picked someone acutely sensitive to the need for a higher price.  OPEC’s recently announced production cutbacks, whether or not they are in fact implemented, are an admission of defeat. As many of the world’s biggest oil producers gathered in Vienna to plot global output and prices, the biggest disruptor was absent. America has no view on global oil production. Crude oil prices remain around half of their highest levels in 2014. Scott Sheffield heads into retirement with PXD’s stock close again to its all-time high, and claims to have production costs as low as $2 per barrel for Permian Horizontal wells.

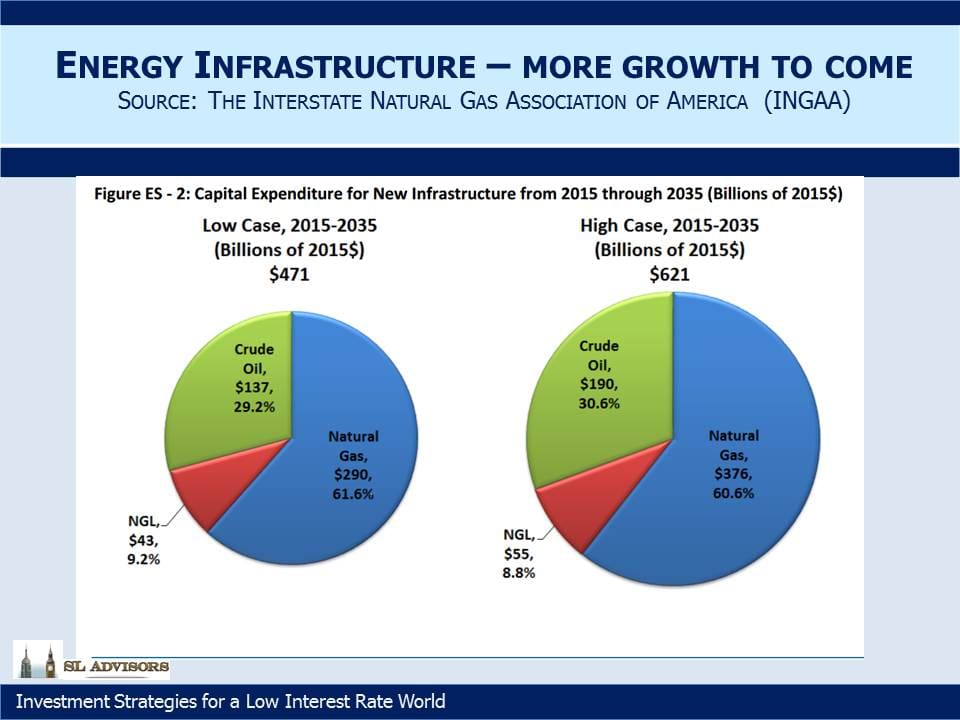

Start with a large energy sector already adept at exploiting conventional resources, with a deep pool of skilled labor and long history of technological improvement. Add to this: access to capital from the world’s biggest capital market; a strong entrepreneurial culture; existing energy infrastructure that can be modified and enhanced to service these new regions of output; ample water and specific grade sand supplies (needed for fracking), often conveniently located; mineral rights that belong to property owners, unknown in other countries but taken for granted in the U.S., which builds community acceptance of drilling activity that creates local wealth. Natural gas from U.S. shale was developed under a much higher price regime which allowed time for scale that could lower costs as global Liquified Natural Gas supplies weighed on prices. Similarly, the development of crude oil sourced from shale started when prices were higher, so the industry was subsequently mature enough to adapt to falling prices. Horizontal drilling and hydraulic fracturing of rock could not have developed as they did under today’s hydrocarbon price regime. OPEC’s strategy was correct but several years too late. There is no going back. Only the U.S. combines all these advantages. The result is that cheap natural gas now produces more electricity than coal, and in November for the first time we became a net exporter of natural gas. We’ve even shipped it to the United Arab Emirates (see Coals to Newcastle), because it’s cheap enough to cover the transportation costs. Crude oil production has turned back up, and the Permian Basin in west Texas (Pioneer’s main area of production) may lead the U.S. to being the world’s biggest oil producer, with both Goldman Sachs and JPMorgan forecasting meaningful increases in output over the next five years at current prices. The world needs U.S. supply. Global consumption is currently around 95MMBD (Million Barrels Per Day). Existing plays suffer annual depletion of around 5% (around 5 MMBD) and new demand is another 1-1.5MMBD. So 6-6.5MMBD of new supply is needed, and the $1TN of capex reductions noted earlier mean it will be coming from fewer places.  Bear in mind that this all happened with an Administration regarded as hostile to domestic production of fossil fuels, at least by the senior executives in that industry. The strong growth in production during Obama’s eight years in office either disproves this view or demonstrates resilience in spite of it. Nonetheless, it’s hard to imagine a more supportive scenario than the one presented by the incoming Administration. Kelcy Warren, Energy Transfer Equity (ETE) CEO, can’t wait for Trump to lift the remaining obstacles to completion of the $3.6BN Dakota Access Pipeline, held up by protests and a late White House intervention in the permitting process. Connections with the energy industry are conspicuous among Trump’s early cabinet picks. Former Texas governor Rick Perry is a director of Energy Transfer Partners (ETP), a position he will no doubt relinquish as he heads up the Department of Energy. As a presidential candidate four years ago Perry planned to close the department. It was one of three Federal agencies he planned to close, and in a delicious twist was the one he famously forgot during a debate (his “Oops” moment). As its head, once he finds his way there he will presumably exercise a light touch in overseeing the energy sector. America’s foreign policy will be led by Exxon Mobil (XOM) CEO Rex Tillerson. After these and other cabinet picks are approved by the Senate, the shift in public policy at the Federal level in support of domestic energy could be dramatic. Moreover, in crude oil the U.S. is now the global swing producer. To see why, consider the thinking behind the $1TN in cuts to exploration budgets (see Why Oil Could Be Higher for Longer). Conventional oil projects involve a large up front capital commitment with a long payback period, during which the overall profitability will be exposed to oil prices. Since the futures market only offers liquidity out to 2-3 years, oil drillers are basically long the oil market. Assessing this risk now includes the 2014-16 oil price collapse which damaged the IRR on many prior investments. A previously uncontemplated oil price is preventing many new projects from being funded, because it might repeat. Yet the U.S. shale producer, ostensibly the instigator of the excess supply, pursues many small projects with minor upfront expense (a horizontal well now costs on average less than $5MM) mitigating individual risk. U.S frackers may forego the significant cost of completing a drilled well in response to lower prices, resulting in an inventory of DUCs (Drilled UnCompleted wells) awaiting higher prices. High initial production rates and faster depletion mean output can be hedged. These producers are better able to protect themselves from the very swings in price that they themselves might create. The other end of the spectrum is Canadian Tar Sands (the Canadians prefer to call it Oil Sands), where production continued even at February’s lows. This generated operating losses before adding in corporate overhead and an appropriate return on capital. Shutting down a tar sands project, with its buried pipes carrying steam to heat the bitumen, risks the infrastructure freezing and cracking. They had little choice but to continue production. New tar sands projects are unlikely. The nimble producer is the swing producer. U.S. Energy Independence in both natural gas and crude oil are within sight. Furthermore, natural gas liquids (such as Ethane and Propane) are supporting a new spurt of growth in Chemicals as cheap domestic inputs drive production of plastics for clothing, electronics, food packaging and aerospace equipment. To state the obvious, we believe the outlook for U.S. energy is very good. And yet, investing in the infrastructure to support this positive outlook is so much more attractive than holding E&P companies. PXD may well go on to make its owners increasingly wealthy, but is in a cyclical business in which financial disaster is one price collapse away. The safer bet is surely the owners of the pipelines, storage, processing facilities and related infrastructure without which none of this potential can be realized. Pipelines are often irreplaceable once built, as communities grow up around and over them. The imperative to connect to the existing network creates insurmountable barriers for would-be new entrants. The impact on midstream businesses from certain of their E&P customers going bankrupt was muted. Debtors taking possession of a defaulting borrower still want cashflow, and in most cases oil and gas production was maintained.  Williams Companies (WMB) is investing heavily in its Transco pipeline network to increase natural gas take-away capacity from the Marcellus and Utica shale regions in Pennsylvania & Ohio. Plains All American (PAGP) is the best placed to profit from increased oil output in the Permian Basin which will use up excess capacity on its pipeline network. Master Limited Partnerships (MLPs), which largely own and operate this infrastructure, will continue to make investments that grow their physical asset base. As we have written many times before, an MLP’s legal structure has much in common with a hedge fund; both have a General Partner (GP) who’s in charge and gets preferential economics. Hedge fund managers have done spectacularly better than hedge fund clients (see The Hedge Fund Mirage). MLP GPs similarly stand to profit from asset growth in the MLPs they control (see Quarterly Report Cards Provide Comfort). We have invested for years with this outlook, a view that is clearly shared with the people who run MLPs who are overwhelming invested in the GPs. Stocks are at all-time highs, while the benchmark Alerian Index remains 30% off its 2014 high. Energy infrastructure is in America, largely immune to a strong dollar or a trade war. Many oil and gas producing regions are politically unstable. Reducing our exposure to such regions through self-sufficiency has obvious national security benefits. The U.S. is a far more attractive trade partner than Russia’s Gazprom for example, where maintenance is scheduled around politically-inspired supply disruptions. There is no more compelling sector in public equities today than American Energy Infrastructure. We are invested in ETE, PAGP, and WMB. |

he success of horizontal drilling and hydraulic fracturing (“fracking”) in the U.S. was releasing increasing amounts of crude oil from hitherto impenetrable porous rock. A consequence was that from 2011-2014 fully all of the increase in global demand for crude oil had been met by North American production (see

he success of horizontal drilling and hydraulic fracturing (“fracking”) in the U.S. was releasing increasing amounts of crude oil from hitherto impenetrable porous rock. A consequence was that from 2011-2014 fully all of the increase in global demand for crude oil had been met by North American production (see  Shale oil and gas production are upending the energy markets. The U.S. is not just the leader in this new technology, it’s virtually the only game in town. Oil, natural gas liquids and natural gas are known to exist in porous rock all over the

Shale oil and gas production are upending the energy markets. The U.S. is not just the leader in this new technology, it’s virtually the only game in town. Oil, natural gas liquids and natural gas are known to exist in porous rock all over the

Important Disclosures

The information provided is for informational purposes only and investors should determine for themselves whether a particular service, security or product is suitable for their investment needs. The information contained herein is not complete, may not be current, is subject to change, and is subject to, and qualified in its entirety by, the more complete disclosures, risk factors and other terms that are contained in the disclosure, prospectus, and offering. Certain information herein has been obtained from third party sources and, although believed to be reliable, has not been independently verified and its accuracy or completeness cannot be guaranteed. No representation is made with respect to the accuracy, completeness or timeliness of this information. Nothing provided on this site constitutes tax advice. Individuals should seek the advice of their own tax advisor for specific information regarding tax consequences of investments. Investments in securities entail risk and are not suitable for all investors. This site is not a recommendation nor an offer to sell (or solicitation of an offer to buy) securities in the United States or in any other jurisdiction.

References to indexes and benchmarks are hypothetical illustrations of aggregate returns and do not reflect the performance of any actual investment. Investors cannot invest in an index and do not reflect the deduction of the advisor’s fees or other trading expenses. There can be no assurance that current investments will be profitable. Actual realized returns will depend on, among other factors, the value of assets and market conditions at the time of disposition, any related transaction costs, and the timing of the purchase. Indexes and benchmarks may not directly correlate or only partially relate to portfolios managed by SL Advisors as they have different underlying investments and may use different strategies or have different objectives than portfolios managed by SL Advisors (e.g. The Alerian index is a group MLP securities in the oil and gas industries. Portfolios may not include the same investments that are included in the Alerian Index. The S & P Index does not directly relate to investment strategies managed by SL Advisers.)

This site may contain forward-looking statements relating to the objectives, opportunities, and the future performance of the U.S. market generally. Forward-looking statements may be identified by the use of such words as; “believe,” “expect,” “anticipate,” “should,” “planned,” “estimated,” “potential” and other similar terms. Examples of forward-looking statements include, but are not limited to, estimates with respect to financial condition, results of operations, and success or lack of success of any particular investment strategy. All are subject to various factors, including, but not limited to general and local economic conditions, changing levels of competition within certain industries and markets, changes in interest rates, changes in legislation or regulation, and other economic, competitive, governmental, regulatory and technological factors affecting a portfolio’s operations that could cause actual results to differ materially from projected results. Such statements are forward-looking in nature and involves a number of known and unknown risks, uncertainties and other factors, and accordingly, actual results may differ materially from those reflected or contemplated in such forward-looking statements. Prospective investors are cautioned not to place undue reliance on any forward-looking statements or examples. None of SL Advisors LLC or any of its affiliates or principals nor any other individual or entity assumes any obligation to update any forward-looking statements as a result of new information, subsequent events or any other circumstances. All statements made herein speak only as of the date that they were made. r

Certain hyperlinks or referenced websites on the Site, if any, are for your convenience and forward you to third parties’ websites, which generally are recognized by their top level domain name. Any descriptions of, references to, or links to other products, publications or services does not constitute an endorsement, authorization, sponsorship by or affiliation with SL Advisors LLC with respect to any linked site or its sponsor, unless expressly stated by SL Advisors LLC. Any such information, products or sites have not necessarily been reviewed by SL Advisors LLC and are provided or maintained by third parties over whom SL Advisors LLC exercise no control. SL Advisors LLC expressly disclaim any responsibility for the content, the accuracy of the information, and/or quality of products or services provided by or advertised on these third-party sites.

All investment strategies have the potential for profit or loss. Different types of investments involve varying degrees of risk, and there can be no assurance that any specific investment will be suitable or profitable for a client’s investment portfolio.

Past performance of the American Energy Independence Index is not indicative of future returns.

Leave a Reply

Want to join the discussion?Feel free to contribute!