Why Shale Upends Conventional Thinking

Long time subscribers will recall that back in 2015 this blog sought ever more creative and different ways to communicate the same message, which was that MLP prices had fallen far enough and represented compelling value. Bear markets have an unfortunate tendency to last longer than their opponents would like. Although the sector rebounded strongly in 2016, some of those 2015 blog posts were premature.

One lesson is that if you’re going to write constructively during a bear market, marshall your arguments and prepare to spread them over more weeks than you might anticipate. Last week MLPs and crude oil rediscovered their once close relationship, to the detriment of investors in energy infrastructure. Forewarned, your blogger will not expend all his constructive thoughts right away.

Prior to the Shale Revolution, MLPs were fairly described as having little correlation with commodity prices. Pipelines were a toll-like business model whose returns were driven by volumes. Today, much of the point of investing in the sector relies on the growth prospects made possible by the Shale Revolution. Ten years ago the need for new investment was limited; today it’s clear that to exploit newly accessible hydrocarbons, infrastructure needs to support these new locations. North Dakota was not known for oil, nor was Pennsylvania known for natural gas.

Therefore, the returns on energy infrastructure investments are nowadays more sensitive to growing domestic production and the consequent utilization of existing as well as planned infrastructure. To take one example, Plains GP Holdings (PAGP) anticipates a substantial increase in EBITDA if growing oil production absorbs more of its available pipeline capacity. Oil production reacts to prices; PAGP’s prospects are linked to those of its customers.

Last November’s strategy shift by OPEC to cut production was an ignominious admission that their prior effort to bankrupt the U.S. shale industry through low prices had failed. It represented a watershed event, the moment when it became clear that a new paradigm was in place, as we noted in The Changing Face of Oil Supply.

“Short-cycle opportunities” are what every oil company needs. Shale now counts the biggest integrated oil companies among its proponents. Exxon (XOM) CEO Darren Woods recently noted that a third of their capex budget is devoted to such opportunities. The key here is the liquidity of the oil futures market. If your project’s timeframe extends beyond the availability of hedge instruments, your IRR is going to be driven by things you can estimate but not control. The real revolution of shale is its short capital cycle; numerous wells are drilled cheaply, with fast but sharply declining production. Capital invested is returned with a year or two and risk can be hedged. Conventional projects require huge upfront commitments with long payback times and consequently uncertain economics.

The recent sharp drop in oil prices hasn’t been pleasant for producers anywhere. But consider the planners of a conventional project – a Final Investment Decision to proceed is a little less certain. Once capital is committed beyond a certain point, there’s little choice but to press on and accept whatever outcome markets deliver. Whereas shale producers, the group whose success ostensibly caused the 2015 crash, can cut back activity with comparative ease. They can just stop drilling, and wait. They can take advantage of even brief rallies in crude futures to hedge production and increase output.

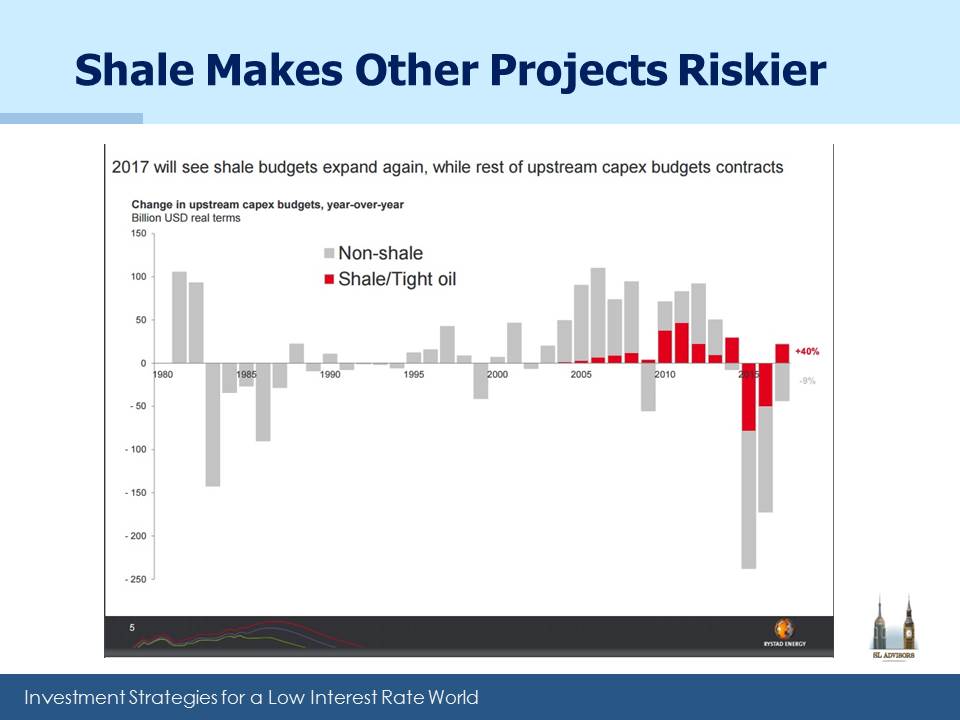

This is why capex on conventional projects continues to fall, as shown in the attached chart from a recent presentation by Lars Eirik Nicolaisen of Rystad Energy. The longer term problem is shaping up to be insufficient investment in new supply to offset depletion of existing fields and new demand (estimated to require around 6% of new supply annually, about 6MMBD, or Millions of Barrels a Day).

The recent drop in crude demonstrates no shortage of supply currently, but also makes providing new supply less attractive in the long run.

MLP investors easily recall the 50.8% drop in the Alerian Index from August 2014-February 2016, its low coinciding to the day with that for oil. We don’t know where crude prices will go over the short term, but it’s becoming increasingly clear that the U.S. is set to gain market share because its short-cycle opportunities represent a substantially more attractive risk/return than conventional projects.

Reaching the long term requires navigating the short term. While you’re doing that, consider how you’d seek your company’s Board approval for a conventional oil project requiring ten years of output to recover its upfront cost. Those shale guys in the Permian could wreck your assumptions, and then protect themselves from the damage they’d wrought by quickly cutting their own capex and production. Without an adequate response, you might feel like moving to West Texas.

We are invested in PAGP

A few weeks ago I did an interview with friend Barry Ritholtz for his Bloomberg series “Masters in Business”. It was just posted online, so for those that are interested you can find it here. Comments on MLPs are at the 65 minutes mark.

Important Disclosures

The information provided is for informational purposes only and investors should determine for themselves whether a particular service, security or product is suitable for their investment needs. The information contained herein is not complete, may not be current, is subject to change, and is subject to, and qualified in its entirety by, the more complete disclosures, risk factors and other terms that are contained in the disclosure, prospectus, and offering. Certain information herein has been obtained from third party sources and, although believed to be reliable, has not been independently verified and its accuracy or completeness cannot be guaranteed. No representation is made with respect to the accuracy, completeness or timeliness of this information. Nothing provided on this site constitutes tax advice. Individuals should seek the advice of their own tax advisor for specific information regarding tax consequences of investments. Investments in securities entail risk and are not suitable for all investors. This site is not a recommendation nor an offer to sell (or solicitation of an offer to buy) securities in the United States or in any other jurisdiction.

References to indexes and benchmarks are hypothetical illustrations of aggregate returns and do not reflect the performance of any actual investment. Investors cannot invest in an index and do not reflect the deduction of the advisor’s fees or other trading expenses. There can be no assurance that current investments will be profitable. Actual realized returns will depend on, among other factors, the value of assets and market conditions at the time of disposition, any related transaction costs, and the timing of the purchase. Indexes and benchmarks may not directly correlate or only partially relate to portfolios managed by SL Advisors as they have different underlying investments and may use different strategies or have different objectives than portfolios managed by SL Advisors (e.g. The Alerian index is a group MLP securities in the oil and gas industries. Portfolios may not include the same investments that are included in the Alerian Index. The S & P Index does not directly relate to investment strategies managed by SL Advisers.)

This site may contain forward-looking statements relating to the objectives, opportunities, and the future performance of the U.S. market generally. Forward-looking statements may be identified by the use of such words as; “believe,” “expect,” “anticipate,” “should,” “planned,” “estimated,” “potential” and other similar terms. Examples of forward-looking statements include, but are not limited to, estimates with respect to financial condition, results of operations, and success or lack of success of any particular investment strategy. All are subject to various factors, including, but not limited to general and local economic conditions, changing levels of competition within certain industries and markets, changes in interest rates, changes in legislation or regulation, and other economic, competitive, governmental, regulatory and technological factors affecting a portfolio’s operations that could cause actual results to differ materially from projected results. Such statements are forward-looking in nature and involves a number of known and unknown risks, uncertainties and other factors, and accordingly, actual results may differ materially from those reflected or contemplated in such forward-looking statements. Prospective investors are cautioned not to place undue reliance on any forward-looking statements or examples. None of SL Advisors LLC or any of its affiliates or principals nor any other individual or entity assumes any obligation to update any forward-looking statements as a result of new information, subsequent events or any other circumstances. All statements made herein speak only as of the date that they were made. r

Certain hyperlinks or referenced websites on the Site, if any, are for your convenience and forward you to third parties’ websites, which generally are recognized by their top level domain name. Any descriptions of, references to, or links to other products, publications or services does not constitute an endorsement, authorization, sponsorship by or affiliation with SL Advisors LLC with respect to any linked site or its sponsor, unless expressly stated by SL Advisors LLC. Any such information, products or sites have not necessarily been reviewed by SL Advisors LLC and are provided or maintained by third parties over whom SL Advisors LLC exercise no control. SL Advisors LLC expressly disclaim any responsibility for the content, the accuracy of the information, and/or quality of products or services provided by or advertised on these third-party sites.

All investment strategies have the potential for profit or loss. Different types of investments involve varying degrees of risk, and there can be no assurance that any specific investment will be suitable or profitable for a client’s investment portfolio.

Past performance of the American Energy Independence Index is not indicative of future returns.

Very insightful article. Thank you!

MLPs have historically required multi-year contracts for access to their pipelines. Will this continue to be the model? Or will the MLPs offer different types of “plans” to different type of clients, such as “on-demand shale producers”?

Thanks for the article.

– Chris