A Futurist's Vision of Energy

Recently a client drew our attention to a presentation by Stanford University Futurist Tony Seba. He has made a splash with his predictions of imminent, dramatic changes in the transportation industry. In less than a generation he expects a world of self-driving (i.e. autonomous), electric vehicles (EVs) supported by a heavily solar/wind-powered electric grid. In June he gave this presentation which you might find interesting.

Tony Seba is an engaging presenter. Moreover, the future of U.S. energy infrastructure will be impacted both by the increasing use of renewables for electricity generation as well as the growth in EVs (renewables and EVs are separate topics, albeit linked). In discussions with investors both of these topics regularly come up. There’s the near-term impact on the sector of growing production driven by the Shale Revolution. Farther out, the growth in renewables (mainly solar and wind) combined with dramatic improvements in battery technology, could represent an existential threat to segments of the U.S. oil industry.

We read and think about these issues a lot. Behavioral economists teach that humans tend to make overconfident forecasts, whether it’s of equity returns, jellybeans in a jar, or the impact of new technology. Precise forecasts exude confidence and draw attention. A date when EVs will predominate is more eye-catching than a range of dates within which such change is more likely than not. Nonetheless, precision in such matters is usually wrong, and we are not with Tony Seba at the extreme end of predictions; the future is rarely so certain. He makes some specific forecasts, including that crude oil demand will peak in 2020-21, after which it will fall 30% by 2030. He also forecasts that by 2030, 100% of new mass-market vehicles bought in the U.S. will be autonomous EVs.

Exxon Mobil (XOM) recently published Outlook for Energy: Journey to 2040, their regularly updated long-term energy forecast. They have an institutional bias towards fossil fuels so they’re never going to line up with a futurist. Nonetheless, forecasting energy use is critical to their long term survival. Seba includes a reference to Eastman Kodak, a company which invented digital photography and was then destroyed by it. XOM will be aware of that example of disruptive technology.

The Outlook for Energy makes forecasts too, beginning with growth in global GDP and population. They forecast 1.8 billion cars, trucks and SUVs on the roads in 2040 (versus 1 billion today) as rising living standards in developing countries drive demand. While expecting impressive percentage growth rates in wind and solar, they expect oil and natural gas to increase their share of the world’s energy needs. Overall, they see fossil fuels slipping modestly, from above 80% to just under 80%, with both coal and oil losing market share to natural gas. They expect crude oil consumption to be around 17% higher in 2040 than it is today. By 2040 they expect 15% of new car sales globally to be hybrids, and 10% of U.S. car sales to be EVs.

To summarize:

| Seba | XOM | |

| Electric Vehicles | 100% of U.S. sales by 2030 | 10% of U.S. sales by 2040 |

| Crude Oil Consumption | Down to approx 70MM Barrels per day by 2030 | Up to approx 115 MM Barrels per day by 2040 |

One of these will be spectacularly wrong.

Although they’re both point forecasts and so unlikely to be precisely right, we think it’s more likely Seba will miss by a lot. His presentation opens with an old photo of New York’s Fifth Avenue in 1900 full of horse-drawn vehicles, and moves to 1912, same place, with all automobiles. It’s true that some new technologies have been highly disruptive, but it doesn’t follow that they all are. Seba’s analogy to the car is intended to validate his EV/solar forecast, although he wasn’t around in 1900 to predict the former.

Growth rates can quickly lead to exponential change when projected out a decade or more. Yet change more often follows an “S” curve, with a high growth rate during widespread adoption followed by slower growth thereafter. We think it’s unlikely the electric grid could adapt so quickly to transmitting the substantially increased electricity required to run a national EV fleet. We also note Seba’s assuming no new advances in the technology of the internal combustion engine, whereas there are continual improvements here too. And the Shale Revolution itself is a form of disruptive technology. We think natural gas is the most likely winner, as it’s the cleanest fossil fuel and enables increased use of renewables by providing baseload electricity for when it’s not sunny or windy.

The price advantage Seba forecasts for solar assumes that the recent substantial productivity improvements in shale drilling don’t continue at all. In fact, he assumes that all the losers, which includes automakers, utilities, oil and gas producing companies, refineries and all those invested in life today as we know it, will stand by passively while their business models are disrupted by new technology. In fact, they are and will continue to respond, by improving their own technology. Furthermore, until battery storage technology and cost improve substantially, we still need backup power for intermediate solar power. This provides demand for of fossil fuel baseload capacity, which often comes from natural gas “peaker” plants (i.e that run only during times of high demand). It’s hard to see a widespread transition to renewables without increased natural gas usage..

An 80% drop in car ownership by 2030 (another Seba forecast) implies widespread car-sharing. Using an Uber-type app to summon an autonomous EV when you need it suggests acceptance of a generic car. What if you need a babyseat? Extra room for luggage? A big family? We think car demand will remain more heterogenous than Seba suggests. Other non-technology hurdles include issues of liability — if your autonomous EV causes an accident, who’s at fault? What if a software bug causes multiple, simultaneous collisions? The deep-pocketed corporations developing the technology will need protection from class action lawyers before it is allowed to go mainstream.

Directionally, Seba’s probably right in that we’re eventually moving to EVs. But investing requires timing too. Seba’s most extreme, widely known forecasts could miss and yet still gain plaudits for getting the direction right, in the same way an equity analyst might gain followers with the highest target price for a hot stock even if it never gets there. But as investors, we care about pace of change as well as direction. Vaclav Smil, a thoughtful and prolific writer about many topics including energy, articulated the major impediments confronting widespread, rapid adoption of renewables. This brief essay, albeit nearly four years old, is still relevant.

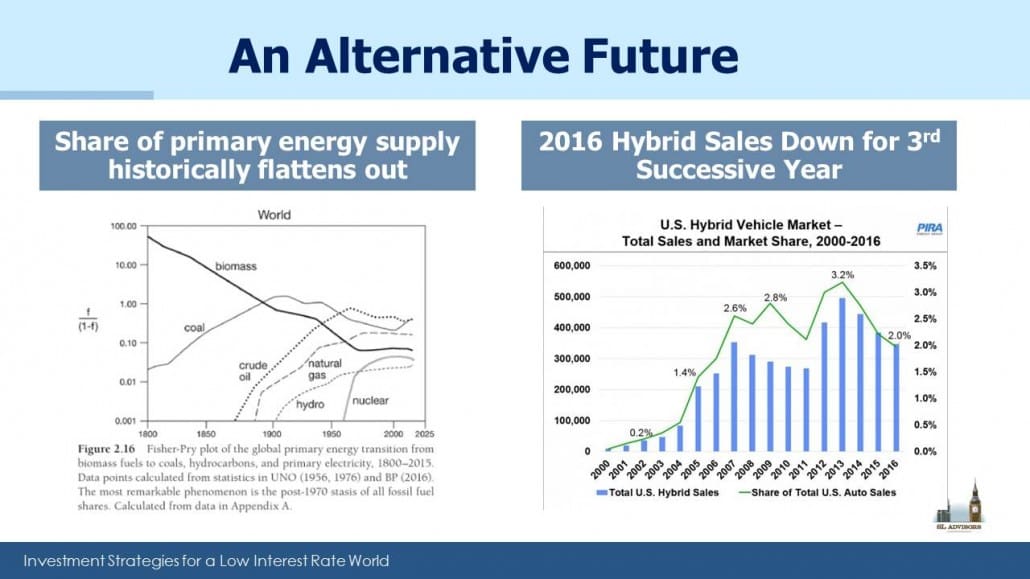

The left chart in the panel below looks complicated, but it shows the proportion of primary energy delivered by each source going back two centuries, on a semi-log scale. The point is that growth slows sooner than expected, and the notes underneath highlight that fossil fuels in aggregate stopped gaining market share in the 1970s, which is probably not intuitive to most people. The chart is from Energy Transitions: Global and National Perspectives, 2nd edition (2016) by Vaclav Smil. The chart on the right shows sales of hybrids and the sensational early growth that fizzled out. Had Tony Seba been giving his presentation in 2005, he probably would have had a chart projecting a car market dominated by hybrids and leaping from its then current 1.4% market share, whereas a decade later it was at 2.0%.

And yet, it really is an exciting future. Personally I can’t wait for autonomous vehicles. I’m sure I’ll own one myself once the technology is proven (I am known by my friends as a late adopter of new things). Being driven by software so the passenger can read, send a text message or even sleep will surely be a great improvement in safety. When I’m finally in my autonomous EV and not driving I’m sure it’ll be better for those around me. Although Seba doesn’t highlight this, one of the strongest arguments in favor of autonomous vehicles is that the software will operate them more safely than unpredictable, sometimes impaired humans. Automobiles kill nearly 1.3 million people globally every year and an additional 20-50 million people are injured or disabled. In this arena like so many others, technology will eventually make the world a better place.

We watch these and other developments carefully. We acknowledge the danger of holding any view with excessive confidence, and new information can cause a reassessment. The further out one goes the harder it is to be certain about oil demand and its price. Growth in wind, solar and other future energy technologies should be taken seriously and must already be a consideration for any big, conventional oil and gas project with a projected return over decades. The optimistic case for renewables highlights the incredible advantage of the Shale Revolution, where development costs are low, production quick, and investments recouped in months. This compares favorably with conventional projects (respectively, high, slow and over many years). For now, we believe Tony Seba’s vision is farther off than he thinks, but what a fascinating journey we will be taking with American innovation revolutionizing the global energy markets from both sides.

Important Disclosures

The information provided is for informational purposes only and investors should determine for themselves whether a particular service, security or product is suitable for their investment needs. The information contained herein is not complete, may not be current, is subject to change, and is subject to, and qualified in its entirety by, the more complete disclosures, risk factors and other terms that are contained in the disclosure, prospectus, and offering. Certain information herein has been obtained from third party sources and, although believed to be reliable, has not been independently verified and its accuracy or completeness cannot be guaranteed. No representation is made with respect to the accuracy, completeness or timeliness of this information. Nothing provided on this site constitutes tax advice. Individuals should seek the advice of their own tax advisor for specific information regarding tax consequences of investments. Investments in securities entail risk and are not suitable for all investors. This site is not a recommendation nor an offer to sell (or solicitation of an offer to buy) securities in the United States or in any other jurisdiction.

References to indexes and benchmarks are hypothetical illustrations of aggregate returns and do not reflect the performance of any actual investment. Investors cannot invest in an index and do not reflect the deduction of the advisor’s fees or other trading expenses. There can be no assurance that current investments will be profitable. Actual realized returns will depend on, among other factors, the value of assets and market conditions at the time of disposition, any related transaction costs, and the timing of the purchase. Indexes and benchmarks may not directly correlate or only partially relate to portfolios managed by SL Advisors as they have different underlying investments and may use different strategies or have different objectives than portfolios managed by SL Advisors (e.g. The Alerian index is a group MLP securities in the oil and gas industries. Portfolios may not include the same investments that are included in the Alerian Index. The S & P Index does not directly relate to investment strategies managed by SL Advisers.)

This site may contain forward-looking statements relating to the objectives, opportunities, and the future performance of the U.S. market generally. Forward-looking statements may be identified by the use of such words as; “believe,” “expect,” “anticipate,” “should,” “planned,” “estimated,” “potential” and other similar terms. Examples of forward-looking statements include, but are not limited to, estimates with respect to financial condition, results of operations, and success or lack of success of any particular investment strategy. All are subject to various factors, including, but not limited to general and local economic conditions, changing levels of competition within certain industries and markets, changes in interest rates, changes in legislation or regulation, and other economic, competitive, governmental, regulatory and technological factors affecting a portfolio’s operations that could cause actual results to differ materially from projected results. Such statements are forward-looking in nature and involves a number of known and unknown risks, uncertainties and other factors, and accordingly, actual results may differ materially from those reflected or contemplated in such forward-looking statements. Prospective investors are cautioned not to place undue reliance on any forward-looking statements or examples. None of SL Advisors LLC or any of its affiliates or principals nor any other individual or entity assumes any obligation to update any forward-looking statements as a result of new information, subsequent events or any other circumstances. All statements made herein speak only as of the date that they were made. r

Certain hyperlinks or referenced websites on the Site, if any, are for your convenience and forward you to third parties’ websites, which generally are recognized by their top level domain name. Any descriptions of, references to, or links to other products, publications or services does not constitute an endorsement, authorization, sponsorship by or affiliation with SL Advisors LLC with respect to any linked site or its sponsor, unless expressly stated by SL Advisors LLC. Any such information, products or sites have not necessarily been reviewed by SL Advisors LLC and are provided or maintained by third parties over whom SL Advisors LLC exercise no control. SL Advisors LLC expressly disclaim any responsibility for the content, the accuracy of the information, and/or quality of products or services provided by or advertised on these third-party sites.

All investment strategies have the potential for profit or loss. Different types of investments involve varying degrees of risk, and there can be no assurance that any specific investment will be suitable or profitable for a client’s investment portfolio.

Past performance of the American Energy Independence Index is not indicative of future returns.

Not that he can’t be wrong but Buffett just lined up to buy a giant truck stop company which is going to need people in vehicles that need fuel.

Rush Limbaugh had a guest a couple of days ago who pointed out some pretty significant problems for electric vehicles…not sure if you have already covered these….each gas station in the us would have to be replaced by a charging station which would require the equivalent capacity of a power supply for a 75,000 person city….each gas station!….also the electricity to supply through those charging stations is not currently available, so a gigantic expansion of electricity power supply would be required….gigantic!….the commentators estimate of the required outlay for charging stations and additional electrical supply was $60 million per station….that is a lot more than your average filling station owner has in his bank account….the technical challenges of getting more electricity in a battery are small next to making enough electricity available to a national fleet of electric cars…these things will be toys for the wealthy for a long, long time…the idea that the source of the additional electricity will be renewables is just too ridiculous to even address given current technology

Emmett, thanks for your comments. We do agree that expanding the electricity distribution network to support a mostly-EV fleet in the U.S. is a huge undertaking not fully considered by some.