A Year After the MLP Crash

A year ago, on February 11th, the Alerian MLP Index (AMZX) put in its low. Following a relentless 58.2% drop from its peak on August 29th, 2014, the selling was finally exhausted. As a retired bond trader friend of mine has said, “Down was a long way”. And indeed it was. The biggest and longest bear market in the history of the index since its creation in 1996. As one whose portfolio holds MLPs in rather more abundance than most readers, I shan’t soon forget the wonder with which we regarded such wholesale liquidation. We never accepted that operating performance of midstream businesses was correctly reflected in those prices. Our conclusion about 2015 was that the real issue was one of the industry needing more growth capital than was available from its fairly narrow traditional investor base (who must generally be U.S., high net worth, taxable and K-1 tolerant). We first articulated this view in The 2015 MLP Crash; Why and What’s Next. The subsequent rebound seemed to support this, since operating results for midstream MLPs generally continued to be within expectations. More recently, in MLPs Feel the Love, we continued with this theme of different investor segments by reviewing how the need for capital was causing some energy infrastructure firms to adapt their corporate structure.

The Alerian Index shows distribution growth that never faltered, dipping only slightly from 6.3% in 2014 to 5.1% in 2015. How could any sector fall so far while continuing to grow payouts? In truth, it does present a slightly rosy picture, as the historic growth figures are based on today’s components of the index. Those MLPs (mostly Exploration and Production, not midstream) who cut or eliminated distributions were ejected from the index, and they took their past with them. Some might find this revisionist history somewhat Orwellian, although hedge fund index providers routinely “backfill” their index series with performance of new additions while removing all trace of those who drop out. Since good performance tends to get you in an index and bad performance gets you out, the consequently recalculated past results are not so easily attainable. Investors who held a cap-weighted portfolio of MLPs seeking to track the index in real time experienced a rather bumpier ride. Nonetheless, today distributions are increasing. Based on quarterly earnings reported so far, R.W. Baird notes 3.0% year-on-year growth in MLP payouts.

Readers should not assume any smugness on our part simply because MLPs have rebounded 77% from the low of a year ago. Such would surely invite the Market Gods to react. There’s always downside, but it does at least appear that today’s MLP investors have committed capital with more thought than the cohort who exited in 2015. All it takes is a glance at recent history to see what the downside might look like if repeated. It wasn’t pretty, but the energy infrastructure industry has upgraded its financiers. Those whose research consists of a price chart have been replaced with a crowd of deeper thinkers, to everybody’s benefit. Many of today’s MLP investors came in because of values, not momentum.

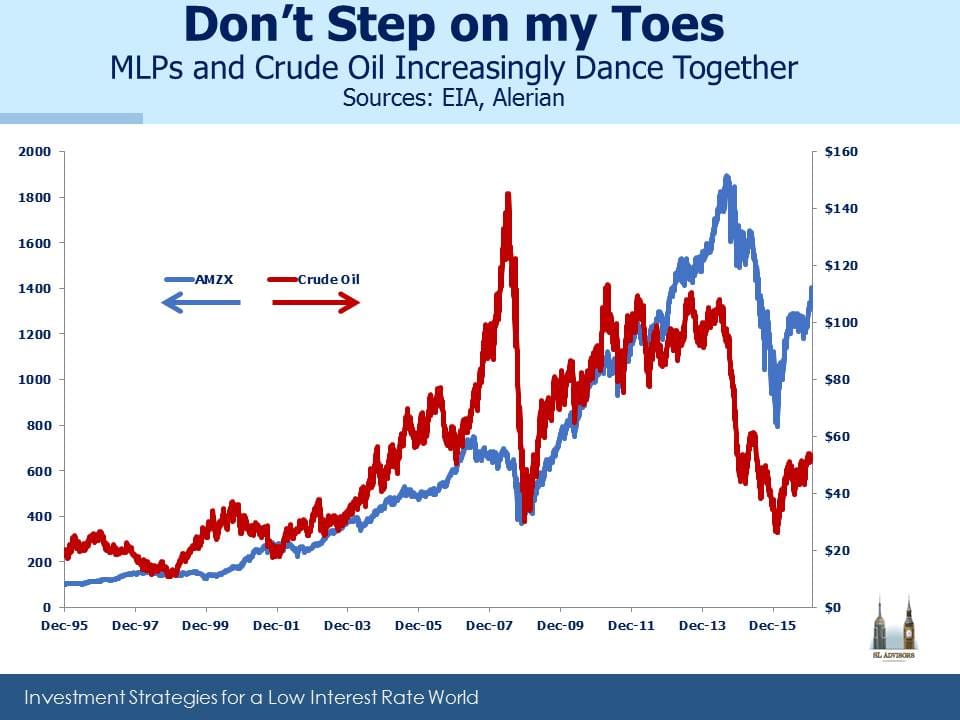

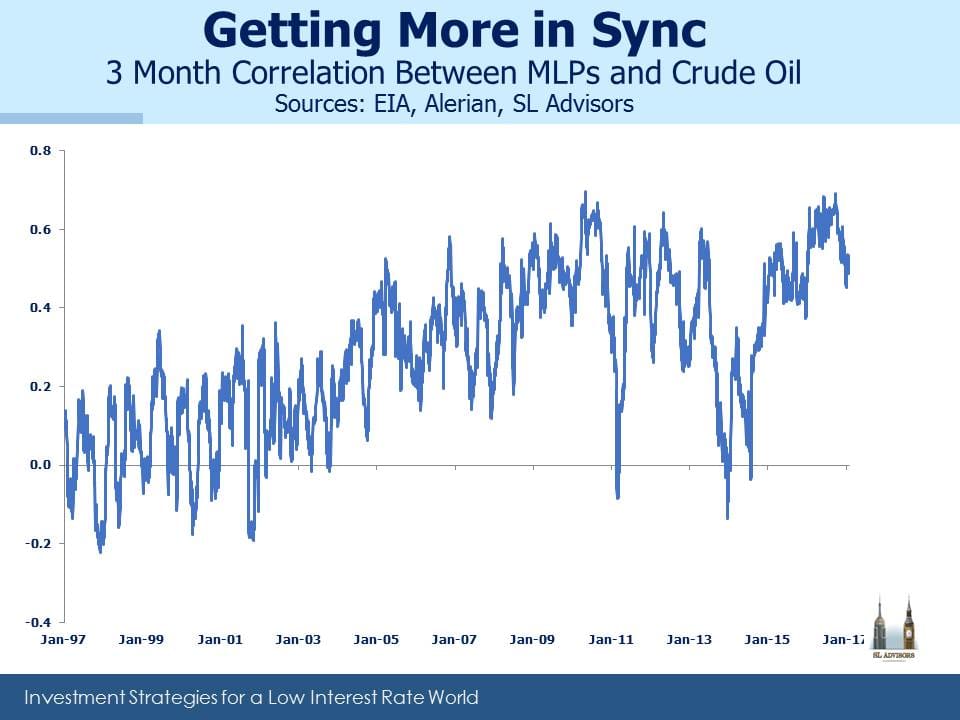

Views on energy infrastructure became synonymous with crude oil over the last couple of years, for good reason. We long ago ditched the slide showing a low correlation between the two. Although the relationship has varied substantially over the past two decades, the Shale Revolution has probably shifted things. Since MLPs care about volume, before domestic energy production was expanding the basic question concerned utilization of the existing network of infrastructure. Now that America can see its way to Energy Independence, supported by increasing domestic production, investors reasonably ask if the additions to infrastructure will be fully utilized. Fluctuations in oil and gas prices do impact production, and large swathes of the U.S. now benefit from higher oil whereas traditionally, lower crude was regarded as a tax cut. Moreover, the Energy ETF XLE now includes energy infrastructure names such as Kinder Morgan (KMI) and Spectra (SE), as well as other energy names that own infrastructure assets. This will inevitably strengthen the relationship between moves in the energy sector and the infrastructure that supports it.

Although the correlation has been falling recently, a stronger positive relationship is likely in the future. We believe there is a good case for rising crude prices (see Why Oil Could Be Higher for Longer) which will further underpin MLP performance. BP just revealed that their business model is predicated on a $60 price for oil by the end of 2018, higher than where it is today.

One of the minor positives of recent media coverage has been the absence of many bullish articles in the financial press. Regrettably, Barron’s finally found the confidence to move out along the ledge with a cautiously optimistic piece last weekend. Is It Too Late To Get In on MLPs’ Latest Bull Run does at least acknowledge in the title that 77% and 12 months after the low they are not exactly catching the proverbial falling knife. Fortunately, constructive articles are not yet an onslaught, so it’s still possible to own MLPs without fearing that it’s everyone’s favorite trade. A year ago bearish articles were abundant, including MLPs: Is the Worst Over? Within days of the low, this Barron’s piece (originally titled The Worst Isn’t Over as its URL betrays) countered its cautiously optimistic heading by quoting a breathless young analyst, “We’re in the early innings of the MLP down-cycle…we had a 15-year up-cycle, and now we’re a year and a half into the downturn.”

The investment writer unburdened by responsibility for managing other people’s money can draw comfort from the knowledge that the victims of poor advice may be few or even non-existent. Much is written and read on investments without being acted upon. Our own constructive tone in writing on MLPs in 2015 contrasted rather painfully with investment results that mocked our prose. One client memorably noted that it would be nice if the quality of our writing was matched by investment performance!

The fee-paying deserve the privilege of offering such feedback. Assuming the writing has remained interesting, over the last year its congruence with returns has improved dramatically.

On a separate note, from time to time fears surface that MLPs will lose their special tax status and be taxed like regular corporations. It’s highly unlikely, but in any event the status quo received support recently from Congress’s Joint Committee on Taxation which estimated foregone revenues from 2016-20 at $4.9BN, down $1BN from prior estimates. Part of the reason is that some MLP investors pay tax on their holdings, notably investors in AMLP and other taxable, C-corp MLP funds (see Some MLP Investors Get Taxed Twice). Not only are such investors hurting themselves, but they’re helping the rest of us by making a revision of MLP tax treatment even less likely. A generous bunch.

We are invested in KMI and SE

Important Disclosures

The information provided is for informational purposes only and investors should determine for themselves whether a particular service, security or product is suitable for their investment needs. The information contained herein is not complete, may not be current, is subject to change, and is subject to, and qualified in its entirety by, the more complete disclosures, risk factors and other terms that are contained in the disclosure, prospectus, and offering. Certain information herein has been obtained from third party sources and, although believed to be reliable, has not been independently verified and its accuracy or completeness cannot be guaranteed. No representation is made with respect to the accuracy, completeness or timeliness of this information. Nothing provided on this site constitutes tax advice. Individuals should seek the advice of their own tax advisor for specific information regarding tax consequences of investments. Investments in securities entail risk and are not suitable for all investors. This site is not a recommendation nor an offer to sell (or solicitation of an offer to buy) securities in the United States or in any other jurisdiction.

References to indexes and benchmarks are hypothetical illustrations of aggregate returns and do not reflect the performance of any actual investment. Investors cannot invest in an index and do not reflect the deduction of the advisor’s fees or other trading expenses. There can be no assurance that current investments will be profitable. Actual realized returns will depend on, among other factors, the value of assets and market conditions at the time of disposition, any related transaction costs, and the timing of the purchase. Indexes and benchmarks may not directly correlate or only partially relate to portfolios managed by SL Advisors as they have different underlying investments and may use different strategies or have different objectives than portfolios managed by SL Advisors (e.g. The Alerian index is a group MLP securities in the oil and gas industries. Portfolios may not include the same investments that are included in the Alerian Index. The S & P Index does not directly relate to investment strategies managed by SL Advisers.)

This site may contain forward-looking statements relating to the objectives, opportunities, and the future performance of the U.S. market generally. Forward-looking statements may be identified by the use of such words as; “believe,” “expect,” “anticipate,” “should,” “planned,” “estimated,” “potential” and other similar terms. Examples of forward-looking statements include, but are not limited to, estimates with respect to financial condition, results of operations, and success or lack of success of any particular investment strategy. All are subject to various factors, including, but not limited to general and local economic conditions, changing levels of competition within certain industries and markets, changes in interest rates, changes in legislation or regulation, and other economic, competitive, governmental, regulatory and technological factors affecting a portfolio’s operations that could cause actual results to differ materially from projected results. Such statements are forward-looking in nature and involves a number of known and unknown risks, uncertainties and other factors, and accordingly, actual results may differ materially from those reflected or contemplated in such forward-looking statements. Prospective investors are cautioned not to place undue reliance on any forward-looking statements or examples. None of SL Advisors LLC or any of its affiliates or principals nor any other individual or entity assumes any obligation to update any forward-looking statements as a result of new information, subsequent events or any other circumstances. All statements made herein speak only as of the date that they were made. r

Certain hyperlinks or referenced websites on the Site, if any, are for your convenience and forward you to third parties’ websites, which generally are recognized by their top level domain name. Any descriptions of, references to, or links to other products, publications or services does not constitute an endorsement, authorization, sponsorship by or affiliation with SL Advisors LLC with respect to any linked site or its sponsor, unless expressly stated by SL Advisors LLC. Any such information, products or sites have not necessarily been reviewed by SL Advisors LLC and are provided or maintained by third parties over whom SL Advisors LLC exercise no control. SL Advisors LLC expressly disclaim any responsibility for the content, the accuracy of the information, and/or quality of products or services provided by or advertised on these third-party sites.

All investment strategies have the potential for profit or loss. Different types of investments involve varying degrees of risk, and there can be no assurance that any specific investment will be suitable or profitable for a client’s investment portfolio.

Past performance of the American Energy Independence Index is not indicative of future returns.

Even “Barron’s cautiously optimistic piece last weekend” by the well-intentioned Amey Stone contained some negativity typical of those unfamiliar with midstream MLPs. Towards the end of the article Ms. Stone cautioned that the volatility of crude pricing and the continued excesses in supply might cause a relapse in MLP unit prices. Ms. Stone, being somewhat unfamiliar with the asset class, assumed that all midstream MLPs were subject to world-wide variations in crude supply and prices. She did not appreciate that there are a substantial number of MLPs whose orientation is towards natural gas infrastructure, which has an entirely different set of pricing disciplines, and unlike oil, has a manifest upward trajectory in the medium and long term (disregarding short term weather patterns) because of imports by Mexico, exports of LNG.by Cheniere and others, exports of NGLs such as ethane and propane (which have revived in price stability) by EPD and others, conversion of coal fueled power plant to gas powered plants, and the number of petrochemical plants coming on stream in the Gulf Coast this year and next, which use NGLs as a feedstock, etc. While there is a loose correlation between NGLs and crude prices they often do not move in lockstep.

In short, even somewhat positive articles often miss the details of the midstream infrastructure industry.