The Tumult in MLPs

If the recent violent sell-off in energy infrastructure stocks has you puzzled, you have plenty of company. That’s why Sunday’s blog is going out early, because we’ve been discussing it with so many people. We enjoy a regular dialogue with many of our investors and last week was the busiest we can recall in responding to clients.

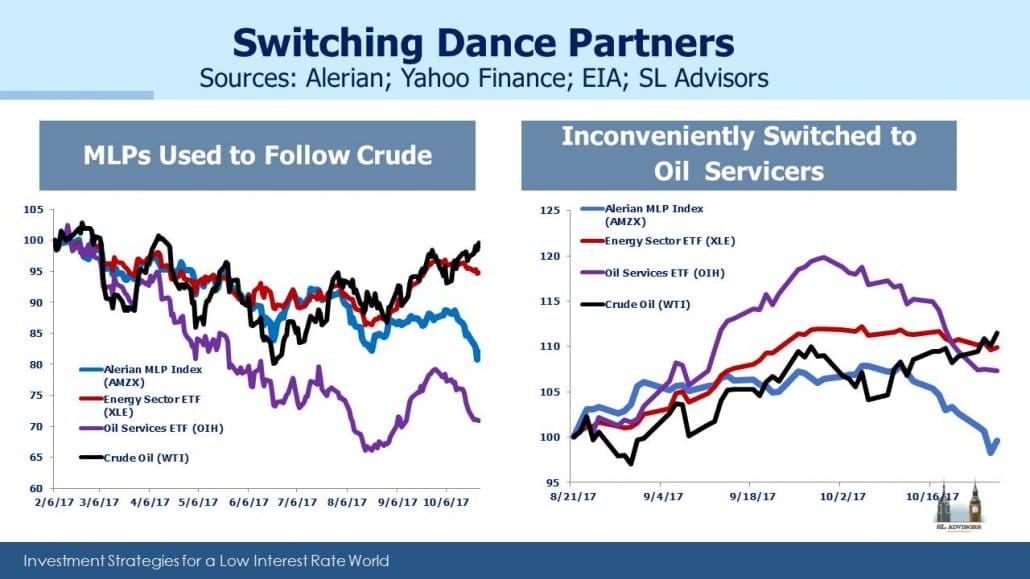

Many wanted to understand why MLPs had followed crude oil lower earlier in the year but failed to mimic its recent recovery. It’s easy to sympathize. A bullish view on oil was almost a prerequisite to committing capital to the sector in the first half of the year. Never mind that linking MLP operating performance to oil is in most cases futile. Their stock prices and oil did move together for months, until that correlation broke down most inconveniently as oil rose. Investors feel duped.

Many callers were looking for confirmation that they’re not missing something, so absent were compelling explanations. Is it tax reform? Little detail is known, but the Administration has proposed allowing owners of partnerships to pay taxes at newly reduced corporate rates rather than the higher ones on income (see MLPs and Tax Reform). And anyway, the MLPA is well practiced at lobbying against adverse tax changes.

Perhaps investors are looking ahead to declining global crude oil demand? It’s a long way off and in any case US output looks set to exceed it previous high of 10 Million Barrels per Day next year, eclipsing a record set in 1970.

Is shale output peaking? The rig count is growing but more slowly. But looking across a broad selection of exploration and production companies, capex plans for 2018 don’t show much sign of retrenchment.

Tax loss selling was suggested by some — energy stocks offer many of the rather limited opportunities this year to sell at a tax-deductible loss. As MLP investors are painfully aware, the stock market has been registering new all-time highs seemingly every week. Hedge fund selling was certainly cited in some quarters, but there are a lot of hedge funds and they’re always buying and selling.

BP’s IPO of its refining business was probably responsible for some selling as investors created room by liquidating other positions. We didn’t participate and it doesn’t look as if we missed an opportunity since it quickly traded below its initial pricing.

Enterprise Products (EPD) used an announced future buyback to redirect cashflow back into new projects (see Why Don’t MLPs Do Buybacks?). It’s reflective of the shifting financing model. An Energy infrastructure sector with opportunities to reinvest in its business is redirecting cash from payouts to capex. It’s disillusioning to the income-seeking investor but is a sensible move if the returns are attractive. The continuing shift from income-seeking to growth-oriented investors is disruptive (see The Changing MLP Investor and More on the Changing MLP Investor), and is a major theme driving recent returns.

Energy Transfer Partners (ETP) yields over 13%. It’s a safe bet that a year from now its yield will be lower, either because the investor skepticism such a yield demonstrates is proven correct and it’s cut, or because buyers scoop up the stock and drive the yield lower. Yesterday, in an act of willful defiance aimed at the skeptics, Energy Transfer raised the dividend both on the GP, Energy Transfer Equity (ETE), and ETP.

Investing usually involves making a decision with adequate information but not all the knowledge one might like. There’s consequently a certain paranoia that, when things don’t go as expected, it’s because others (usually those selling) had some insight overlooked by the buyer. This can be a valuable self-protective instinct. The trader who concludes he knows all that’s needed to trade profitably is usually an ex-trader before too long. Many clients were explicitly or implicitly worried that this might be the case.

But while a certain amount of paranoia can be useful, it’s not always correct that a mark to market loss proves an analytical oversight. We continue to scour for tangible justifications behind the recent move, so far with limited success. We’ve talked to investors in the last week who are buying, holding and selling. The first two are easy to justify on valuation terms even though it takes a brave soul to risk capital under current circumstances. But the sellers we’ve chatted to know little more than the first two categories. What they do know is that they’ve had enough. They feel aggrieved that a correctly constructive view on oil prices has been destructive. They are tired of their clients asking why, in such a buoyant equity market, they own stocks that are falling. They’re fed up with missing the action. Maybe valuations are compelling but they’re no longer of a mind to wait for other buyers to act on this. They don’t possess more facts than the buyers, they’ve simply run out of patience.

It’s a pity, and will probably look like an emotional decision over the long run. But it sure felt good earlier in the week, and may well look brilliant following another week of selling.

Market timing is rarely easy, and so we remain invested because valuations are more attractive in energy infrastructure than any other sector. Don’t use leverage. Pick companies and sectors with strong balance sheets. This enables waiting out the inevitable swoons that over-managing positions causes.

We are invested in EPD and ETE

Important Disclosures

The information provided is for informational purposes only and investors should determine for themselves whether a particular service, security or product is suitable for their investment needs. The information contained herein is not complete, may not be current, is subject to change, and is subject to, and qualified in its entirety by, the more complete disclosures, risk factors and other terms that are contained in the disclosure, prospectus, and offering. Certain information herein has been obtained from third party sources and, although believed to be reliable, has not been independently verified and its accuracy or completeness cannot be guaranteed. No representation is made with respect to the accuracy, completeness or timeliness of this information. Nothing provided on this site constitutes tax advice. Individuals should seek the advice of their own tax advisor for specific information regarding tax consequences of investments. Investments in securities entail risk and are not suitable for all investors. This site is not a recommendation nor an offer to sell (or solicitation of an offer to buy) securities in the United States or in any other jurisdiction.

References to indexes and benchmarks are hypothetical illustrations of aggregate returns and do not reflect the performance of any actual investment. Investors cannot invest in an index and do not reflect the deduction of the advisor’s fees or other trading expenses. There can be no assurance that current investments will be profitable. Actual realized returns will depend on, among other factors, the value of assets and market conditions at the time of disposition, any related transaction costs, and the timing of the purchase. Indexes and benchmarks may not directly correlate or only partially relate to portfolios managed by SL Advisors as they have different underlying investments and may use different strategies or have different objectives than portfolios managed by SL Advisors (e.g. The Alerian index is a group MLP securities in the oil and gas industries. Portfolios may not include the same investments that are included in the Alerian Index. The S & P Index does not directly relate to investment strategies managed by SL Advisers.)

This site may contain forward-looking statements relating to the objectives, opportunities, and the future performance of the U.S. market generally. Forward-looking statements may be identified by the use of such words as; “believe,” “expect,” “anticipate,” “should,” “planned,” “estimated,” “potential” and other similar terms. Examples of forward-looking statements include, but are not limited to, estimates with respect to financial condition, results of operations, and success or lack of success of any particular investment strategy. All are subject to various factors, including, but not limited to general and local economic conditions, changing levels of competition within certain industries and markets, changes in interest rates, changes in legislation or regulation, and other economic, competitive, governmental, regulatory and technological factors affecting a portfolio’s operations that could cause actual results to differ materially from projected results. Such statements are forward-looking in nature and involves a number of known and unknown risks, uncertainties and other factors, and accordingly, actual results may differ materially from those reflected or contemplated in such forward-looking statements. Prospective investors are cautioned not to place undue reliance on any forward-looking statements or examples. None of SL Advisors LLC or any of its affiliates or principals nor any other individual or entity assumes any obligation to update any forward-looking statements as a result of new information, subsequent events or any other circumstances. All statements made herein speak only as of the date that they were made. r

Certain hyperlinks or referenced websites on the Site, if any, are for your convenience and forward you to third parties’ websites, which generally are recognized by their top level domain name. Any descriptions of, references to, or links to other products, publications or services does not constitute an endorsement, authorization, sponsorship by or affiliation with SL Advisors LLC with respect to any linked site or its sponsor, unless expressly stated by SL Advisors LLC. Any such information, products or sites have not necessarily been reviewed by SL Advisors LLC and are provided or maintained by third parties over whom SL Advisors LLC exercise no control. SL Advisors LLC expressly disclaim any responsibility for the content, the accuracy of the information, and/or quality of products or services provided by or advertised on these third-party sites.

All investment strategies have the potential for profit or loss. Different types of investments involve varying degrees of risk, and there can be no assurance that any specific investment will be suitable or profitable for a client’s investment portfolio.

Past performance of the American Energy Independence Index is not indicative of future returns.

Good insight and feedback, Simon.

I’m in for long haul and just pur chased additional shares for my daughter in Mlxix.

Thanks for that column. It needed to be said. As for the disclosure about being in ETE , aren’t you worried about investing with Kelcy Warren? I am.

Yes, Kelcy doesn’t act like a fiduciary. It’s a factor. ETE is less of a position than it would otherwise be for this reason. So it’s not a binary issue, but is incorporated into our sizing.

Great Article Simon, thank you.

At its current yield, I think the ETP calls are mispriced.I picked up a significant amount at the 18 strike at $1.10 earlier this week. I can’t see the stock at these yields a year from now – one way or the other. Either it will get bid back up, or they’ll cut and the stock will stagnate/drop. I don’t necessarily want it to be a long term position (Kelcy is the major factor) but it offers too compelling a risk/reward here.