U.S. Oil Output Continues to Grow

We’re in earnings season again, and last week we listened to US Silica’s (SLCA) conference call on Wednesday morning. Weakness in MLP prices due to softer crude oil is incongruous with the positive outlook communicated by SLCA’s CEO Bryan Shinn. Volumes and pricing were both up 15% quarter-on-quarter, with sand volumes in their Oil and Gas segment up 79% versus a year ago.

The continued innovation in shale drilling extends to varying the grades of sand used and generally quantities too. Moreover, while some analysts are concerned about overcapacity in the sand industry, CEO Shinn noted that because different grades of sand are not easily substituted, total supply capacity needs to be 20-25% greater than demand in order for the market to clear. He noted projections of 100 million tons (MT) of demand in 2018 (up from 75 MT this year), versus optimistic 2018 supply estimates of only 90 MT.

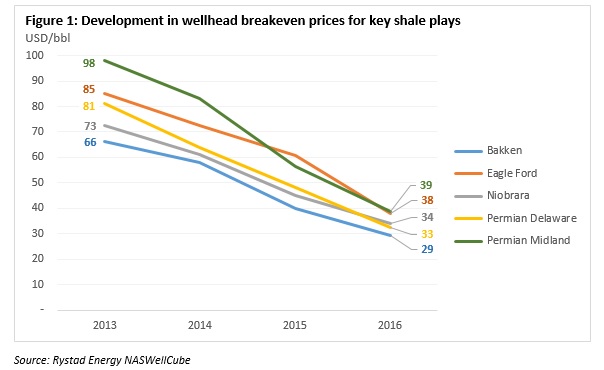

To SLCA, higher prices will be needed for the market to balance. U.S. shale drillers, who are the customers of MLPs and consumers of sand, show every sign of continuing to increase production. Breakevens continue to fall, with costs coming down another $10 per barrel across many shale plays over the past year. Shell’s CEO recently noted that break-evens in the Permian Basin in West Texas were $40 per barrel. This will support ongoing demand for the infrastructure and support MLPs provide.

The shale industry is producing more, while MLP investors remain nervous about the price of crude oil (see MLP Investors Not Yet Convinced).

Meanwhile, the International Energy Agency noted that global oil discoveries and new projects fell to historic lows last year with 2017 expected to offer little improvement. For three straight years exploration spending has been half of what it was in 2014. They contrasted the sharply reduced investment spending in the conventional oil sector with resilience of the U.S. shale industry.

Oil has been very volatile over the past three years, swinging from a high of $106 per barrel in June 2014 to $26 in February 2016. Historically, both supply and demand have been fairly inelastic which has resulted in fairly modest shifts in producer/consumer behavior translating into large price moves. The supply response function has historically been slow; if the world suddenly needs another 1 million barrels a day, there isn’t a dormant oil field that can be suddenly switched on. From discovery to production with a conventional field is years. Similarly, if supply is just a little more than the world needs (as was the case in 2015) it takes quite a price drop to induce a supply reduction.

Conventional oil (and gas) projects are long cycle. By contrast, U.S. shale is short cycle in that wells can be drilled inexpensively and begin producing within months, with the high initial production rates allowing faster payback of capital invested. The availability of short cycle oil projects should make the supply response function shorter, which in turn should reduce the volatility of oil. This is why Exxon Mobil and other major energy firms are redirecting their capital spending (see Why Shale Upends Conventional Thinking).

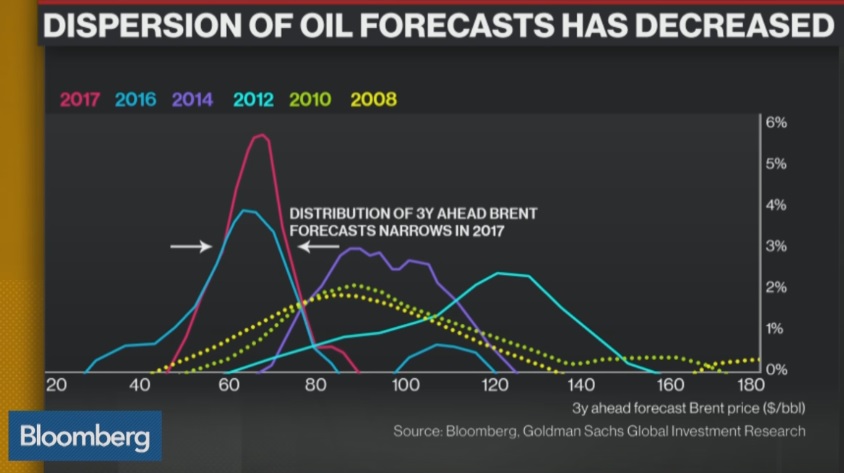

Our thanks go to good friend and client Gerry Gaudet for directing us to the chart above. It compares the dispersion of oil forecasts in recent years, and the range is the narrowest in a decade. In other words, market participants are converging on a narrower likely price range for oil price as they incorporate the growing role of short cycle, U.S. shale into their supply models. This greater certainty is also likely to flatten the price curve for oil and perhaps even cause it to invert to backwardation (i.e. future prices lower than current), at least until something happens to upset these forecasts. One inference (apart from unexciting times for oil traders) is that projects with a breakeven much above $80 a barrel are going to be hard to finance since so few forecasters expect that high a price.

We are invested in SLCA