Tallgrass Energy is the Right Kind of MLP

Tallgrass Energy is the Right Kind of MLP

If Linn Energy was the wrong kind of MLP (see last week’s blog), Tallgrass Energy is the right kind. They have an MLP, Tallgrass Energy Partners (TEP) and a publicly traded General Partner, Tallgrass Energy, GP (TEGP). It’ll come as little surprise to regular readers that we are invested in TEGP alongside CEO David Dehaemers because, as Willie Sutton knew, that’s where the money is. Dehaemers runs a great conference call, combining plain talk with a little levity, such as promising to finish a recent call in time for analysts to get their opinions from Jim Cramer’s Mad Money.

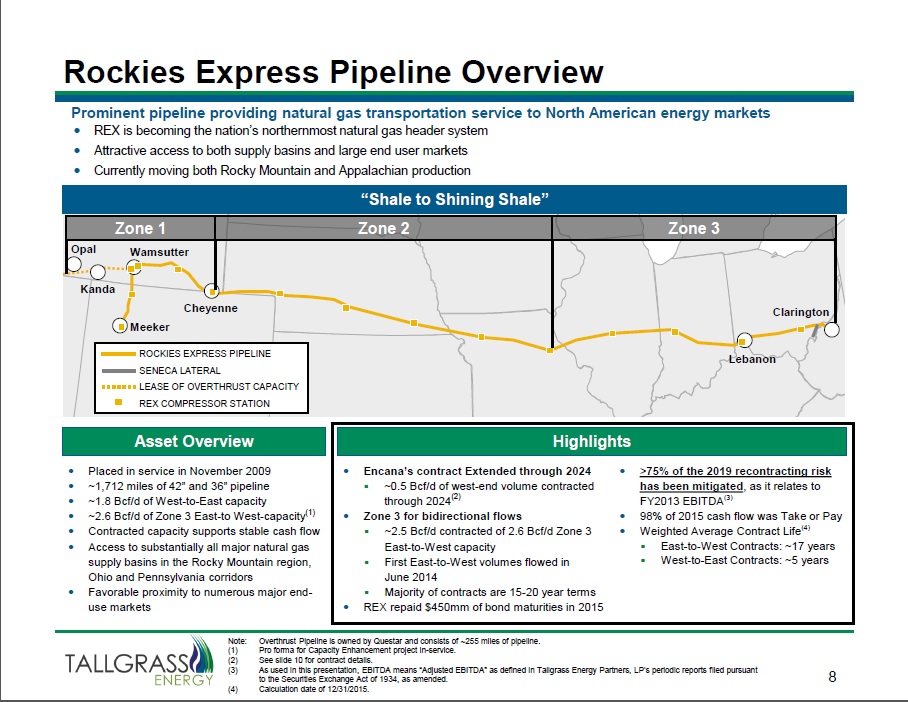

Last week Tallgrass held a webcast to discuss their Rockies Express natural gas pipeline (“REX”). The slide below is from that webcast. REX runs from Wyoming to West Virginia, from “Shale to Shining Shale” if nonetheless short of being completely transcontinental. TEP recently acquired a 25% interest in REX from privately-held Tallgrass Development. It’s a great asset, with the ability to connect to many population centers across the northern U.S. states it traverses. However, the recent abundance of natural gas in the north east U.S. out of the Marcellus and Utica shales has hindered the traditional west-east flow of gas from the Rockies, and had especially affected demand in the Zone 3 eastern section of the pipeline from Illinois.

The webcast provided a positive update on the contracting of capacity on REX. Last year Tallgrass implemented a pipeline reversal on Zone 3 to allow two-way flow on that part of the network. They anticipate extending this to the rest of REX in the years ahead. The increased capacity and flexibility create substantial optionality to meet future demand, and have brought improved visibility to the EBITDA REX is expected to generate. Consequently, TEP is guiding to 20% distribution growth. More interestingly for Dehaemers and other investors in the GP, TEGP is expecting to grow its cash distributions at twice the rate of TEP. Since TEGP’s entitled to half the additional Distributable Cash Flow generated by TEP, growth at TEP is magnified for TEGP, whose economic relationship with TEP resembles that of hedge fund manager to hedge fund. Tallgrass is midstream infrastructure operating a toll-type business model. Tallgrass is the right kind of MLP.

Is Irrational Exuberance Returning to MLPs?

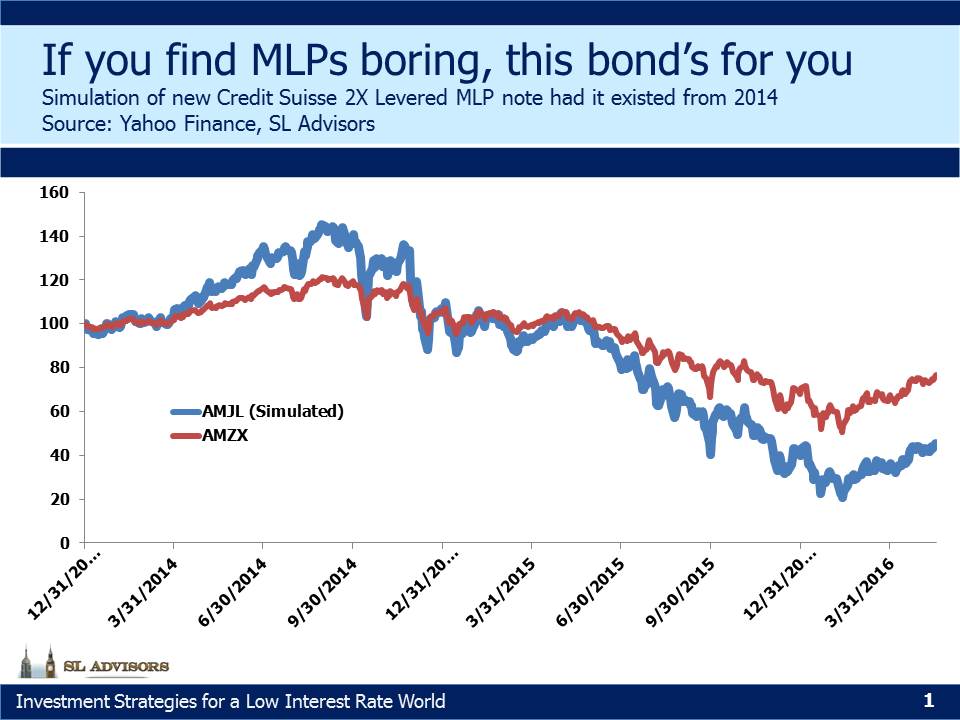

Such a question seems premature by at least several years, and yet is prompted by the issuance last week by Credit Suisse of a 2X levered note linked to the Alerian Index. Its buyers must desire to make money in a hurry, a quest which invariably results in the opposite outcome.

At the risk of being a party pooper, below is a simulation of the performance AMJL would have delivered to its thrill seeking holder had he invested at the beginning of 2014. Here I’m unapologetically sexist; only a man would buy AMJL (see June 2014 newsletter How to Invest Like a Woman). The highs would have been high, but the lows would have been, well, low. AMJL’s creator is unburdened by the need to design products for which a long term holding period is preferable. Lots of products are sold that nonetheless are bad for you, including tobacco products, cocaine and non-traded REITs. Add enough warning labels and (with some exceptions) you can meet consumer demand. However, you are unlikely to find a CFA charterholder near AMJL because the CFA’s Integrity List includes “Place the client’s interests before your own”, a requirement inconveniently at odds with distributing securities whose holders, “…intend to actively monitor and manage their investments” (as noted in the 14 page section on Risk Factors).

If a non-financial company issued a security like AMJL, potential buyers would reasonably assume that the issuer’s objective was simply to raise money cheaply. Credit Suisse has the same objective, and yet as their brokers promote it some confused investors will assume Credit Suisse has their best interests at heart and will be persuaded that it is a good investment.

There are worse securities than AMJL to be sure. It is not in the league of non-traded REITs. But it is one whose proponents have fingers crossed while promoting, and will hopefully inflict less damage on clients than two similar ETN’s issued by UBS which collapsed far enough to trigger mandatory redemptions as recently as January (see the second section of this blog post from January). Standards in Finance are not yet unreasonably high.

We are invested in TEGP.