Growing Without Paying For It

Investors in Master Limited Partnerships (MLPs) like their distributions to be reliable and, by comparison with other asset classes, generous. Investors in the General Partners (GPs) that control them hold a more discerning view on value creation. Last month we highlighted how Williams Companies (WMB) was giving its MLP investors in Williams Partners (WPZ) what they want (reliable, high distributions) while also meeting the different needs of WMB investors for total return (see Williams Satisfies Two Masters).

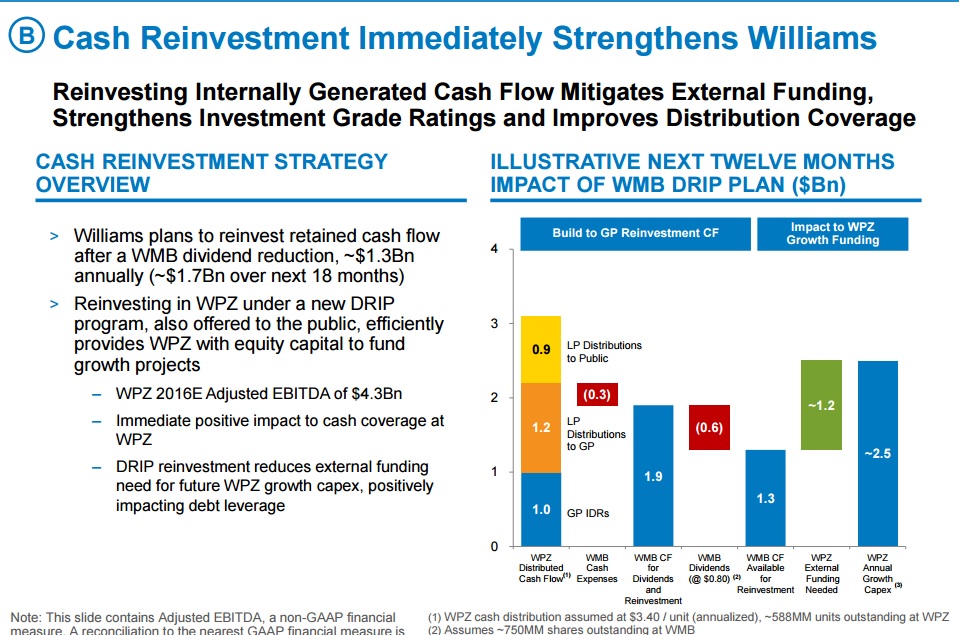

The slide below from a recent WMB investor presentation lays it out nicely. WMB has two sources of cashflow – LP distributions from WPZ (since it owns WPZ units) and Incentive Distribution Rights (IDR) related cashflows from their GP interest. These two items are expected to generate 1.2BN and $1BN respectively for WMB over the next twelve months.

Move right across the bar chart and they’re planning to invest $1.3BN annually in new projects, by investing in new units of WPZ. These new WPZ units will generate additional IDRs through WMB’s GP interest. Working through the numbers, WPZ will supplement the $1.3BN it receives for selling new units to WMB with $1.2BN in debt, giving it $2.5BN to invest in new projects.

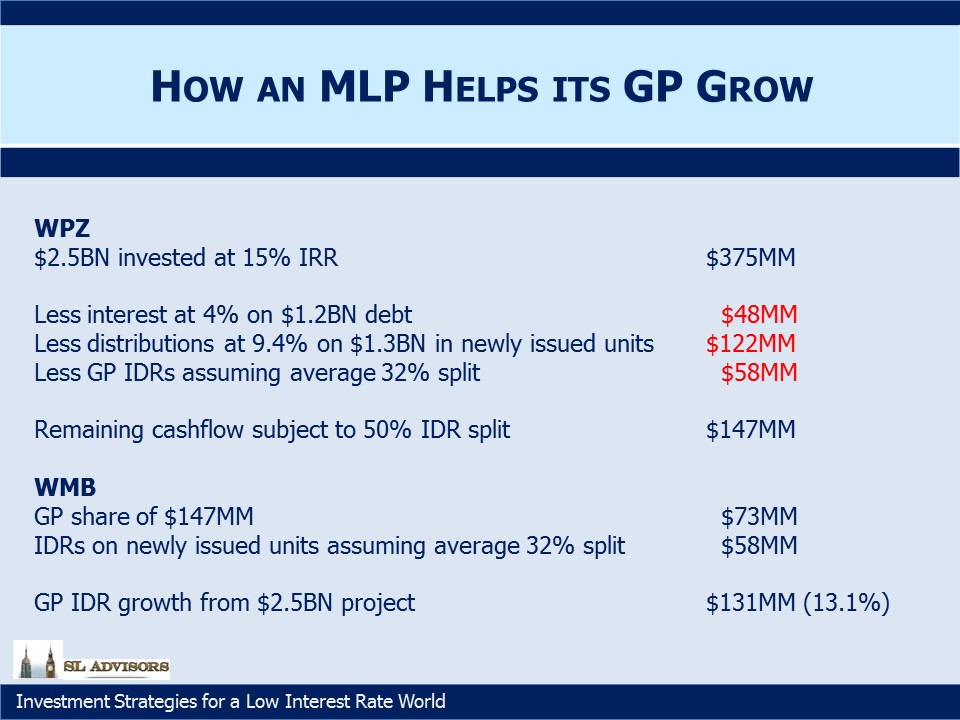

We know from other regulated projects that WPZ’s minimum IRR target is 15% on invested capital. The table below shows how this cashflow will divide up. WMB receives on average 32% of WPZ cashflows (i.e. the $1BN GP take is 32% of the $3.1BN total WPZ Distributed Cash Flow, the left-most bar on the chart). So WMB should expect 32% of the project’s cashflows and WPZ LP unitholders 68% up to a 9.4% return on the LP units (the current yield on WPZ). Thereafter, since the GP is at the 50% level on IDRs, the excess cashflow is split equally.

The total IDR take for WMB from the $2.5BN WPZ capital outlay is $131MM, representing a 13.1% growth rate on its current $1BN GP IDR receipts. WMB can if it chooses sell the $1.3BN in WPZ LP units acquired into the open market at a time of its choosing, thus winding up with no net cash outlay in exchange for this growth.

So what’s it worth? The LP cashflows are pretty straightforward. $1.2BN in WPZ distributions less the $300MM in cash operating costs leaves $900MM, valued at the market yield on WPZ units of 9.4% gives $9.6BN.

WMB’s market cap is $22.4BN, so the GP stake is being valued at $12.8BN ($22.4BN – $9.6BN), or 11.3X next year’s cashflow. This looks cheap compared to other transactions. For example, Marathon (MPL) acquired MarkWest last year at an implied GP multiple of more than twice this, according to figures from Wells Fargo. And our analysis here only assumes GP IDR growth from new projects; it gives no credit to growth from WPZ’s substantial existing asset base. So we think the 13.1% growth rate on the GP IDRs is conservative. In effect, WMB can grow its GP IDR-derived cashflow without having to pay for it.

We think on this basis that WMB is undervalued.

We are invested in WMB.