U.S. Natural Gas Terms of Trade Continue to Shift

Data recently released by the Energy Information Agency (EIA) highlighted the continuing shift in U.S. terms of trade regarding natural gas. The North East U.S. (NY, OH, PA, NJ, MD, DE and VA) was for the first time in 2014 no longer a net importer of natural gas from Canada, as production in the Marcellus Shale in Pennsylvania finally grew so as to make the region self-sufficient. The Great Lakes states (MI, WI, MN) have been net exporters for several years, now joined by another region as defined in the EIA’s release.

Even though the North East is reducing its reliance on Canadian natural gas, there remain infrastructure bottlenecks in New England preventing sufficient peak supplies reaching customers. Boston paid as much as $30/MCF for natural gas this past winter to meet high electricity demand, and limited regional pipeline capacity is expected to cause continued seasonal spikes for the next few years. The states in the region have begun to co-ordinate their efforts to improve access to electricity, natural gas and renewables. Spectra Energy (SE) is just one of the energy infrastructure companies seeking support from state and local governments in the region for its plans to improve natural gas distribution.

In related news, the first LNG export facility in the lower 48 states is expected to begin operations later this year (The Kenai LNG export terminal in Alaska is currently the only source of U.S. LNG exports). The Sabine Pass facility in Louisiana is owned by Cheniere Energy Partners (CQH). It is run by a colorful character named Charif Souki, memorably portrayed in Greg Zuckerman’s 2014 book The Frackers. Last year CQH’s parent company, Cheniere Inc (LNG) was forced to withdraw its proposed compensation plan following investor lawsuits arguing it was too generous. Meanwhile, CQH spent $17MM on distributions to MLP investors last year, no doubt fostering a warm feeling about their stable business. However, unlike most MLPs, distribution coverage isn’t a useful metric since CQH has no revenues yet. One wonders how many unitholders actually know that. No doubt when the Sabine Pass facility begins operations their income statement will look wholly different, but this was one name that didn’t make it through our screening process, although LNG exports remain a fascinating story.

As an aside, in a previous career as a restaurant operator Souki had the misfortune to own the L.A. restaurant where Nicole Brown Simpson, OJ Simpson’s wife, last ate prior to being murdered in 1994. Souki’s business career includes episodes of near-bankruptcy and it’s fair to say he and I have different risk appetites. However, having successfully converted Sabine Pass from an LNG import facility to one that exports, he’s likely to be one of the winners from U.S. energy independence.

Of the names mentioned, we are invested in SE.

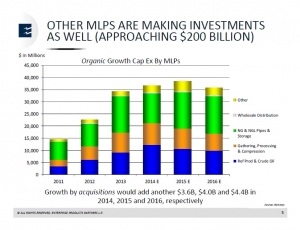

l expenditures (“capex”) and a drop in 2016 versus 2015. However, the numbers remain substantially higher than the pre-2013 period, and support the forecast of $30-50BN in annual capex for energy infrastructure (since while MLPs are the main operators of such assets, integrated oil companies and utilities also fund energy sector projects).

l expenditures (“capex”) and a drop in 2016 versus 2015. However, the numbers remain substantially higher than the pre-2013 period, and support the forecast of $30-50BN in annual capex for energy infrastructure (since while MLPs are the main operators of such assets, integrated oil companies and utilities also fund energy sector projects). bigger MLPs.

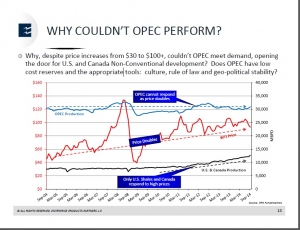

bigger MLPs. ‘t, and highlights the difference between very low production costs for proved, developed reserves in the Middle East versus relatively high costs to develop new resources beyond what is already in production. Clearly, from the perspective of a group of producers that still satisfies roughly one third of global oil demand, a modest increase in output to maintain market share and render new sources of supply uneconomic early on would have been a far less costly strategy than the current one of maintaining fairly constant output regardless of price. It suggests that even countries such as Saudi Arabia have a fairly limited capacity to increase output over the short term.

‘t, and highlights the difference between very low production costs for proved, developed reserves in the Middle East versus relatively high costs to develop new resources beyond what is already in production. Clearly, from the perspective of a group of producers that still satisfies roughly one third of global oil demand, a modest increase in output to maintain market share and render new sources of supply uneconomic early on would have been a far less costly strategy than the current one of maintaining fairly constant output regardless of price. It suggests that even countries such as Saudi Arabia have a fairly limited capacity to increase output over the short term.