Energy Sector Gathers Momentum

Last week I was chatting with an investor about the attractive valuations in the MLP sector. 2Q17 earnings were generally in-line, with the notable exception of Plains All American (see MLPs Learn About Logistics). Valuations are compelling, with the yield on the Alerian Index currently sitting at 5.5% above the ten year U.S. treasury, 2% above its 20-year average. On an Enterprise Value to EBITDA basis, energy infrastructure compares favorably with Utilities (see The Changing MLP Investor).

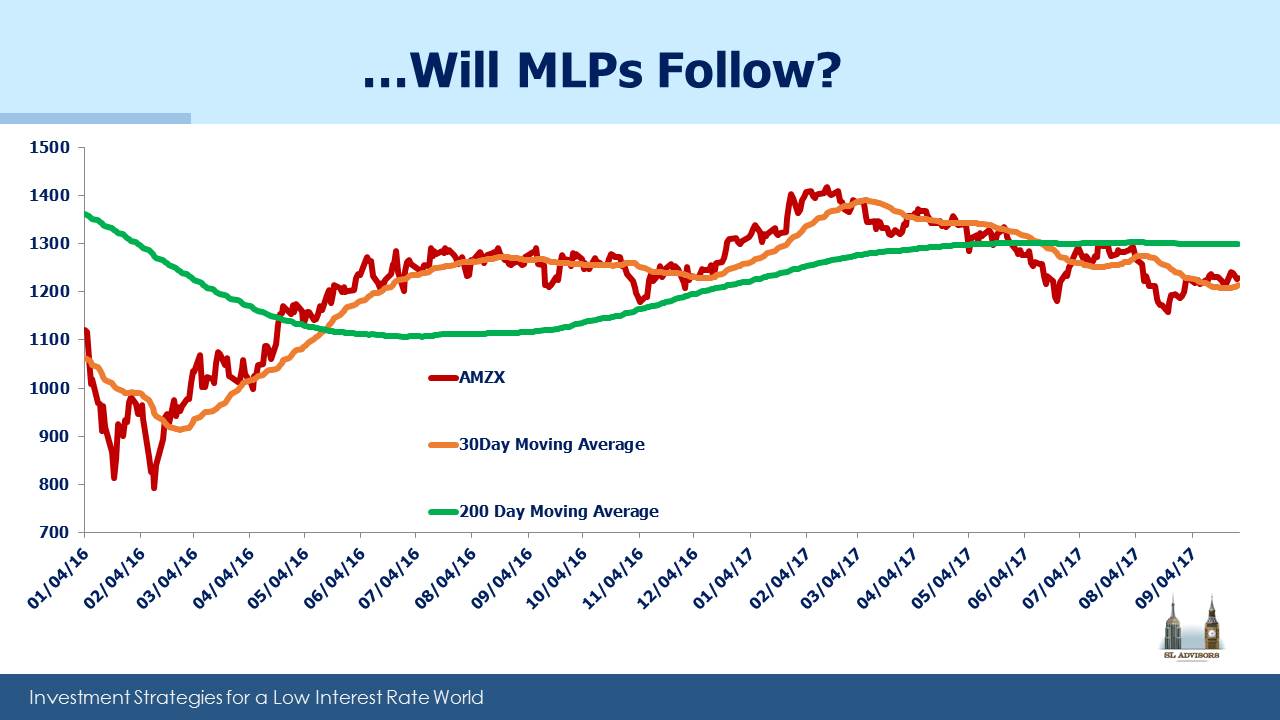

And yet, even though MLPs and crude oil have generally been moving together this year (see Crude and MLPs March Higher Together), in recent weeks MLPs have lagged the bounce in oil. So the natural question is, what is the catalyst that will cause investors to act on these valuation advantages?

CFA charterholders have to pass three fairly rigorous exams that (among other things) demonstrate an ability to analyze financial statements. In an effort to include most forms of equity analysis there is a brief section on Technical Analysis. When I studied that material I could almost feel the apologetic tone from CFA Institute as they reconciled undoubted antipathy towards an area that has wide adherence and works just often enough to warrant inclusion.

Many investors we know rely on fundamental analysis to make decisions but then use technical analysis to refine timing. The merits of an investment change far less often than its price, and technicals can help here. We’ve noted a pick-up in activity from some buyers partly because such analysis is indicating a change in trend.

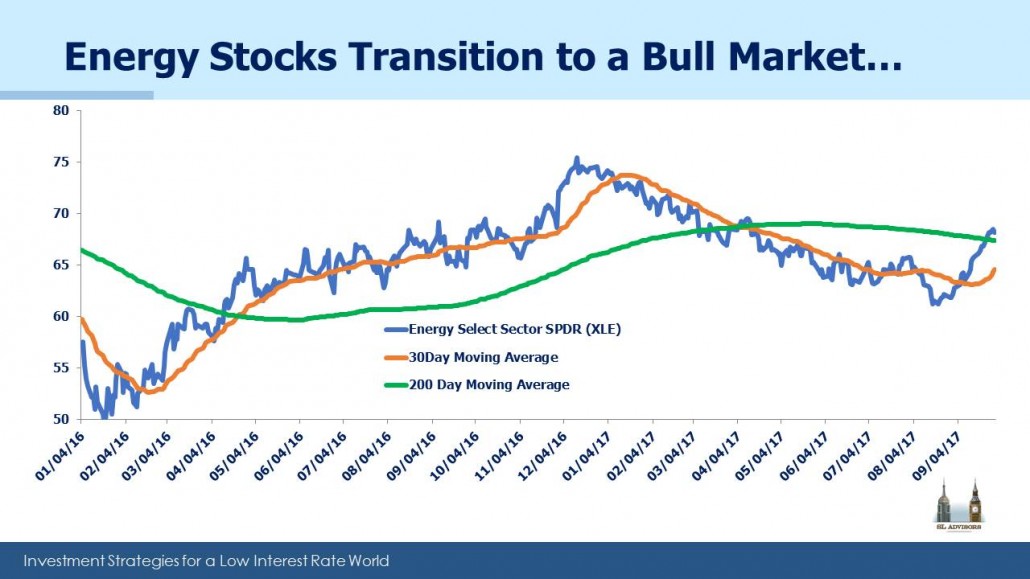

It’s not just crude oil that has developed a recent uptrend. The broader energy sector has also moved sharply higher, with prices now above the 200-day moving average. In 2015 a tough operating environment for exploration and production companies (i.e. the clients of MLPs) led to substantial weakness in the energy infrastructure sector. Although they are clearly not synchronized, recent strength in crude and energy stocks would seem likely to improve sentiment among MLP investors. Performance between the two sectors is unlikely to diverge for long.

On a different topic, Alerian announced last week that they’d be capping individual constituents at 10% in the Alerian MLP Index (AMZ). This is a sensible move that brings this index into line with the Alerian MLP Infrastructure Index (AMZI). Enterprise Products Partners (EPD) was most impacted because it was previously 20% and was the cause for the change.

EPD’s share has risen in part because their market cap has risen relative to their peers but also because some MLPs have simplified their structure and been dropped from the index. The most recent example was Oneok (OKE), which merged its GP-owning C-corp OKE with its MLP, Oneok Partners (formerly OKS). Many people think of Kinder Morgan (KMI) as an MLP but following their simplification in 2014 which saw the assets of Kinder Morgan Partners absorbed into KMI, they have no longer been part of the AMZ (although still in AMZI). There’s more to energy infrastructure nowadays than MLPs, and C-corps represent an increasingly significant element.

Although Alerian does a good job in managing their indices, they have an odd way of measuring distribution growth. The 6% average annual growth rate they report reflects trailing growth of the current constituents, not the actual growth of the constituents that were in the index at the time. So the recent change in EPD’s weighting, which will similarly boost the weighting of several other names, will alter the historic growth rate. The actual growth rate experienced by investors in the Alerian Index of course won’t change. Running an index is complicated.

Finally, we’re heading into the fourth quarter, a time when seasonal patterns around MLPs become more important. In last year’s blog post on the topic (see Give Your Loved One an MLP This Holiday Season) we explained which months were best for buying purely when considering seasonal patterns. It’s worth rereading if you’re thinking of investing over the next few months.

We are invested in EPD, KMI and OKE

Important Disclosures

The information provided is for informational purposes only and investors should determine for themselves whether a particular service, security or product is suitable for their investment needs. The information contained herein is not complete, may not be current, is subject to change, and is subject to, and qualified in its entirety by, the more complete disclosures, risk factors and other terms that are contained in the disclosure, prospectus, and offering. Certain information herein has been obtained from third party sources and, although believed to be reliable, has not been independently verified and its accuracy or completeness cannot be guaranteed. No representation is made with respect to the accuracy, completeness or timeliness of this information. Nothing provided on this site constitutes tax advice. Individuals should seek the advice of their own tax advisor for specific information regarding tax consequences of investments. Investments in securities entail risk and are not suitable for all investors. This site is not a recommendation nor an offer to sell (or solicitation of an offer to buy) securities in the United States or in any other jurisdiction.

References to indexes and benchmarks are hypothetical illustrations of aggregate returns and do not reflect the performance of any actual investment. Investors cannot invest in an index and do not reflect the deduction of the advisor’s fees or other trading expenses. There can be no assurance that current investments will be profitable. Actual realized returns will depend on, among other factors, the value of assets and market conditions at the time of disposition, any related transaction costs, and the timing of the purchase. Indexes and benchmarks may not directly correlate or only partially relate to portfolios managed by SL Advisors as they have different underlying investments and may use different strategies or have different objectives than portfolios managed by SL Advisors (e.g. The Alerian index is a group MLP securities in the oil and gas industries. Portfolios may not include the same investments that are included in the Alerian Index. The S & P Index does not directly relate to investment strategies managed by SL Advisers.)

This site may contain forward-looking statements relating to the objectives, opportunities, and the future performance of the U.S. market generally. Forward-looking statements may be identified by the use of such words as; “believe,” “expect,” “anticipate,” “should,” “planned,” “estimated,” “potential” and other similar terms. Examples of forward-looking statements include, but are not limited to, estimates with respect to financial condition, results of operations, and success or lack of success of any particular investment strategy. All are subject to various factors, including, but not limited to general and local economic conditions, changing levels of competition within certain industries and markets, changes in interest rates, changes in legislation or regulation, and other economic, competitive, governmental, regulatory and technological factors affecting a portfolio’s operations that could cause actual results to differ materially from projected results. Such statements are forward-looking in nature and involves a number of known and unknown risks, uncertainties and other factors, and accordingly, actual results may differ materially from those reflected or contemplated in such forward-looking statements. Prospective investors are cautioned not to place undue reliance on any forward-looking statements or examples. None of SL Advisors LLC or any of its affiliates or principals nor any other individual or entity assumes any obligation to update any forward-looking statements as a result of new information, subsequent events or any other circumstances. All statements made herein speak only as of the date that they were made. r

Certain hyperlinks or referenced websites on the Site, if any, are for your convenience and forward you to third parties’ websites, which generally are recognized by their top level domain name. Any descriptions of, references to, or links to other products, publications or services does not constitute an endorsement, authorization, sponsorship by or affiliation with SL Advisors LLC with respect to any linked site or its sponsor, unless expressly stated by SL Advisors LLC. Any such information, products or sites have not necessarily been reviewed by SL Advisors LLC and are provided or maintained by third parties over whom SL Advisors LLC exercise no control. SL Advisors LLC expressly disclaim any responsibility for the content, the accuracy of the information, and/or quality of products or services provided by or advertised on these third-party sites.

All investment strategies have the potential for profit or loss. Different types of investments involve varying degrees of risk, and there can be no assurance that any specific investment will be suitable or profitable for a client’s investment portfolio.

Past performance of the American Energy Independence Index is not indicative of future returns.

Leave a Reply

Want to join the discussion?Feel free to contribute!