Activist hedge funds can be a positive force. Although this isn’t always true (Keith Meister of Convergex so abused ADT investors that his actions caused us to apply the “Corvex Discount” to other stocks in his viewfinder), it’s probably more often than not beneficial to existing investors when a hedge fund shows up.

The most recent case involves Tetra Technologies (TTI), about which we wrote a few weeks ago as an example of the power of the MLP General Partner. Dimitri Balyasny just filed a 13G (indicating a passive stake) in TTI and a 5.3% investment. Acquiring 4.3 million shares of TTI is quite a trick, considering their average daily volume of under 1 million shares.

Other activist-owned stocks of interest to us that were recently in the news include Dow Chemical (DOW), which last week announced the sale of its chlorine business (DOW shareholders will own 50.5% of the resulting chlorine business with Olin Corp). Hedge fund Third Point has been a long-time advocate for value-enhancing moves. Another is Hertz (HTZ), which is owned by a virtual who’s who of hedge funds including funds run by Carl Icahn, Larry Robbins, Jeffrey Tannenbaum and Barry Rosenstein. HTZ has been recovering from some self inflicted wounds including accounting mistakes, poor pricing strategy and the relocation of its headquarters to Naples, Florida so as to be close to the (now former) CEO’s golf club. The persistent lethargy in HTZ’s stock price shows that it takes more than four activist investors to raise the price. However, moves in recent months to hire new management are positive signs. Today Morgan Stanley lifted its sell recommendation.

Although the equity research business is dominated by large, sell-side firms hoping to generate trading commissions from their (usually bullish) recommendations, there are alternate business models out there. Prescience Point is a hitherto unheard of research firm with no known location (so presumably outside the U.S. since they’re not registered) and no publicly disclosed employees. They focus on research uncovering companies’ fraudulent activities. Although they write about what they find, so as to (presumably) sell their research to subscribers, they also short the stocks they cover.

Short sellers are a fascinating bunch. The odds are stacked against them. Company managements and sell side research (both of which are generally bullish) are in the opposite corner from them. In addition, short positions have almost unlimited potential loss with gains limited by the proceeds received for the sale of the stock. Markets generally rise over time, so these headwinds to success mean that short sellers need to carry out pretty detailed work, and they need to be right.

What Prescience can do (based on their website) is:

(1) Produce a bearish report

(2) Share it privately with paying subscribers

(3) Short the stock themselves prior to its public release

(4) Buy back the shorted stock when the report is out

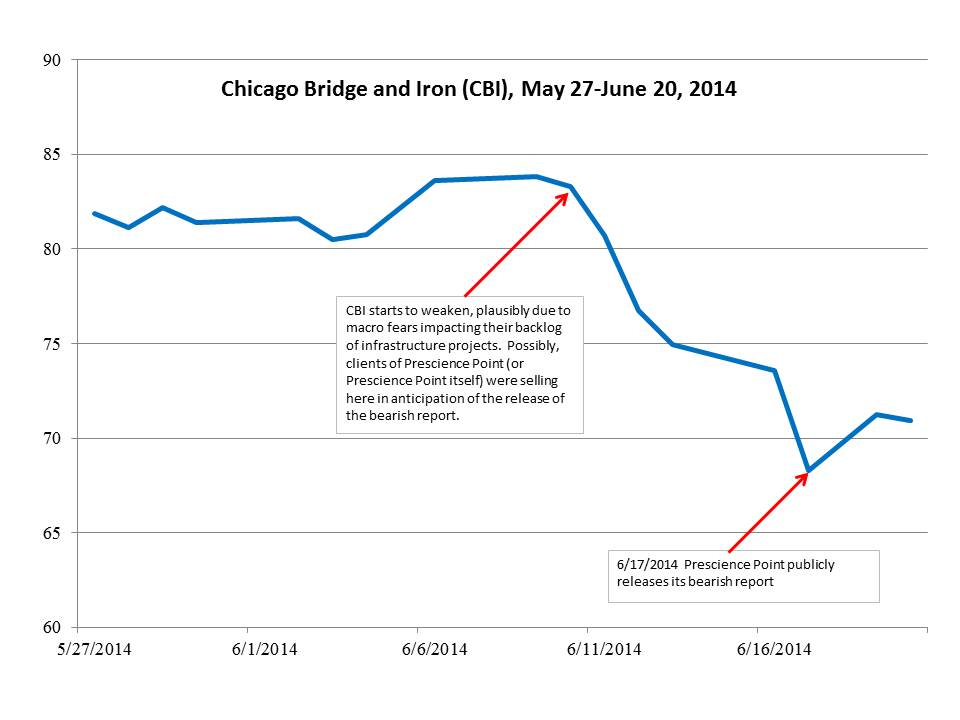

Chicago Bridge and Iron (CBI) is a $7.5 billion market cap company that builds energy infrastructure. Nuclear plants, oil pipelines, LNG plants (for transporting liquid natural gas) and other related projects. Their contracts are lumpy since completion can take many years. They recently acquired a competitor, Shaw Group, almost doubling their revenues.

CBI’s stock recently behaved as if Prescience had imposed its business model described above on it. When CBI began to weaken in early June on no apparent news, we assumed perhaps investors were becoming more wary of their backlog of infrastructure orders given the developing tumult in the Middle East. The stock weakened further (as shown in the chart below) until Prescience released their report. At this point reasons for the earlier weakness became clear, and additional sellers unwilling to subscribe but now finally aware of the report’s insight, were convinced to sell.

There doesn’t seem to be anything illegal with this. In any event, Prescience appears to be outside the U.S. and their website is pretty clear in warning that they trade both before and after releasing their reports. And it’s not obvious that there’s even anything wrong with what they’re doing. They have a point of view; they share it with clients; they act on it; they publicize their view. And they tell you this is what they’re doing.

In fact, their research doesn’t even need to be right. To be valuable, all that’s required is for the stock price to drop after Prescience and its clients have sold. What’s needed is a group of sellers who will sell after the report is public, for it’s this last drop that creates the profit opportunity. As long as there are enough uninformed sellers willing to sell the stock on the public release of the report so that the earlier, informed sellers can cover their positions, the business model will work. This presumably limits the number of subscribers because too many of them might cause the stock to rally on the report’s publication as they overwhelmed the fewer sellers involved. It’s quite an interesting business model; not quite God’s Work, as Goldman’s CEO Lloyd Blankfein so regrettably once described what his company does, but it’s a living of sorts I guess.

We’ve held a small long position in CBI for some time. We were puzzled by the early June sell off, but when the report was published on June 17th,the reason for the stock’s weakness became clear. Warren Buffett has famously said that in a poker game, if you don’t know who the patsy is, you’re the patsy. June 17th was a day during which we guess that patsies were unusually active in CBI. We just don’t know if the patsies were the sellers (late to the party, having missed the opportunity to sell at higher prices during the prior few days) or the buyers (willfully ignoring the now public short thesis offered by Prescience).

For our part, we didn’t find much compelling in their report and so bought more CBI on June 17th. We just don’t know yet if we’re the patsies or not.

https://sl-advisors.com/wp-content/uploads/2013/04/logo1.jpg00Simon Lackhttps://sl-advisors.com/wp-content/uploads/2013/04/logo1.jpgSimon Lack2014-06-23 14:31:572014-06-23 14:31:57How to Short A Stock and Get Others to Join You

On Tuesday I attended the morning session of Agrium’s (AGU) Investor Day in NY (the second part was scheduled for Memphis to visit a couple of their facilities). We’re invested in Agrium, having been first drawn to the stock by Jana’s Barry Rosenstein. Last year Jana published a detailed criticism of the company, highlighting both its natural advantages in the production of Nitrogen-based fertilizer and its poorly performing retail division. AGU does look cheap, trading at an Enterprise Value to EBITDA multiple of around 6X, or about 10X earnings.

Natural gas is a significant input into the production of Nitrogen-based fertilizers, around 40% of AGU’s 2012 EBITDA. Like other North American based producers, cheap domestic natural gas has created a cost advantage versus foreign producers. Owning AGU is a good way to invest in the benefits of this cheap North American resource. Jana’s criticisms focused on the Retail division, which they argue is inefficiently run and has made some overpriced acquisitions. Earlier this year a bitter proxy fight broke out as Jana attempted to elect new board members that it felt would be more qualified to oversee the running of the company. The upshot of Jana’s interest was that it lost the proxy fight although perhaps not coincidentally AGU did take some steps to return money to shareholders through a newly instituted dividend and share buyback. However, the stock price has slumped since the proxy fight.

The investor presentation was a useful opportunity to see the company’s leadership team present its strategy. Although Barry Rosenstein was not there, his presence could be felt throughout the morning. The company went to great lengths to justify its retail strategy, to highlight their successful prior acquisitions but also to reassure that no major new acquisitions would be forthcoming and to explain that it would maintain its recently found focus on returning capital to shareholders. Their wholesale business has some solid advantages even while prices for its commodities remain under pressure. Its retail business continues to seek operating efficiencies so as to improve returns. The company’s stock price still seems to suffer from a conglomerate discount.

Michael Wilson will be retiring as CEO at the end of the year; no doubt having seen off the threat from Jana it feels like a good time to move on. The new CEO Chuck Magro seems a smart guy but the obvious question is why they didn’t select one of the two Presidents of their main operating divisions (Wholesale and Retail), both of whom have extensive careers with the company. Chuck Magro has far less operating experience than his two key direct reports, having spent much of his career in staff functions such as Internal Audit, Risk Management and Corporate Development and Strategy. He was only recently appointed to his current role of Chief Operating Officer (COO), in November 2012, creating the impression of a somewhat hasty decision on succession management by CEO Wilson. Chuck’s younger than Ron Wilkinson (Wholesale President) and Richard Gearheard (Retail President), and while that need not be a problem by itself, one can’t help but think that his relative youth and limited operating experience will be noted by the two presidents. In fact, the obvious question is why one of them wasn’t chosen to be CEO. While Retail President Gearheard might have been a controversial choice to run the company given the focus on Retail performance, he and Wilkinson must surely believe themselves to be qualified for the top spot. Both having been passed over for a younger candidate suggests perceived shortcomings in each of them.

The presentations by each division president were informative and interesting. They were also notable for what was not said. In both content and style, the impression was given of two entirely separate businesses that happened to share the same corporate owner. It was as if Agrium is a holding company with two unrelated enterprises. Neither president spoke even in passing about the other division and although Agrium claims to have an integrated strategy there was little integration in evidence down at the divisional level. Perhaps unfairly, this was somewhat exacerbated by cultural differences; the current and new CEO are both Canadian, as is the Wholesale head Wilkinson. Retail is run by Americans from southern states such as Oklahoma and Mississippi. In response to a question on identifying synergies between the two divisions, CEO Wilson noted that much of what the Retail division sells is sourced from Wholesale although Jana has previously asserted that 90% of Retail’s products are sourced from third parties.

Although AGU’s stock sold off following the investor day, possibly on cautious guidance for wholesale or maybe because others perceived the issues noted above, we continue to be invested in Agrium. The company has some clear advantages and its stock price is attractive. Barry Rosenstein’s previously articulated concerns hold some substance. We’ll see if the new management can rise to the opportunity their business model holds.

https://sl-advisors.com/wp-content/uploads/2013/04/logo1.jpg00Simon Lackhttps://sl-advisors.com/wp-content/uploads/2013/04/logo1.jpgSimon Lack2013-10-10 14:07:132013-10-10 14:07:13Agrium's Investor Day

Who thought that Canadian equity markets operated with shareholder protections that would bring even a developing country’s regulator to shame? Here’s the story: Agrium (AGU), a poorly managed producer and distributor of agricultural products in Calgary, is engaged in a proxy fight with Jana Partners, an activist investor with some very good ideas on how AGU could improve its performance. Jana has proposed its own slate of five nominees for the Board of Directors, people who it believes will improve the Board’s ability to run its retail business. AGU hasn’t welcomed Jana’s interest, and in the upcoming vote it transpires that AGU will be paying Canadian financial advisers who vote their clients’ shares in favor of AGU’s nominees.

It’d be bad enough to pay individual shareholders to vote a certain way, but paying their advisers? Are the Canadian managers of client assets really up for sale? Are they really the world’s oldest profession?

It’s a quite extraordinary set of circumstances, surely not a way of doing business that Canadian regulators can defend. We are invested in AGU. Jana’s interest piqued ours. AGU’s vote-buying makes it a more attractive investment, since it confirms the poor judgment of current management. Their continued tenure is surely now more tenuous.

https://sl-advisors.com/wp-content/uploads/2013/04/logo1.jpg00Simon Lackhttps://sl-advisors.com/wp-content/uploads/2013/04/logo1.jpgSimon Lack2013-04-02 15:41:592013-04-02 15:41:59Agrium Shows Morals Are Optional

Nice piece today on BBBY. We’ve liked this stock for a while, strong balance sheet, reasonably priced and exposed to the improving housing market. Barrons probably goes a little overboard in speculating that it’s the kind of name Berkshire (BRK) might choose to acquire, but we think it’s a good investment with plenty of opportunity to generate an attractive return.

https://sl-advisors.com/wp-content/uploads/2013/04/logo1.jpg00Simon Lackhttps://sl-advisors.com/wp-content/uploads/2013/04/logo1.jpgSimon Lack2013-03-09 11:35:512013-03-09 11:35:51Barrons Covers Bed, Bath and Beyond

Cincinnati Bell (CBB) will celebrate 140 years since its founding this July. It has long provided phone and data communications to residents and businesses in Ohio, Kentucky and Indiana. We have been invested in them for the tiniest sliver of their history, and today endured our very first quarterly earnings release. We were lambs to the slaughter.

The bull case on CBB is that they own a data center (Cyrusone; NYSE:CONE) which represents an undervalued asset. Although their fixed line business is in decline, they have been investing in the data center and in January sold 31% of the company in an IPO. The 69% of CONE that CBB retains is itself worth $975MM, more than the market cap of CBB itself.

The genius in the CONE IPO was that it relieved CBB of the need to continue funding CONE’s CAPEX allowing CBB to pay out excess cash flow as dividends while raising enough capital for the independent datastorage business to self fund growth. The $390MM of EBITDA that CBB expects to generate in 2013 should need to cover even less capex than 2012 for its legacy business and even after interest and pension fund contributions ought to provide for $100MM to be distributed to shareholders. Since CBB doesn’t pay a dividend, even a $0.25 cent annual dividend ($50MM) on a $4.25 stock would provide almost a 6% yield and draw in dividend investors to drive the stock higher. The once ophan stock of the legacy telco that pays no dividend while investing in datastorage becomes appealing to income seeking investors while their investment in CONE is rewarded in the market by REIT investors seeking growth.

But instead, the company disclosed in its earnings release that it projects 2013 capex at $180-190MM for the non-CONE businesses. The equivalent number in 2012 was $140MM, so they’re increasing their investment into a declining business. The value creation they promised with one hand through the CONE IPO is being hijacked by management with the other. In addition to which, they’re paying certain employees $40-50MM in “IPO success payments”. So far, those are the only people who have made any money out of the IPO.

Fortunately we were not bold and our investment was very small (indeed, smaller after today’s rout). The good news is that the equity in CBB’s remaining business excluding the 69% of CONE they retain is valued at negative $320MM. That’s how the market assesses their decision to quicken the pace of fiber-optic investments and the odds that they’ll generate a return above their cost of capital.

So now it’s over to the activists to impose a taste of corporate democracy on a management team that’s lost the plot. As of December 31 holders included Marcato Capital Management, Gabelli and Lonestar Capital Management. Assuming they retain an investment they can’t be happy with today’s developments. The IPO Success Fee especially grates. We’re holding our small position in the knowledge that more value exists than the company’s current valuation implies while we await a 13-D filing. It might well be an interesting story to follow.

https://sl-advisors.com/wp-content/uploads/2013/04/logo1.jpg00Simon Lackhttps://sl-advisors.com/wp-content/uploads/2013/04/logo1.jpgSimon Lack2013-02-27 16:57:162013-02-27 16:57:16Reminding CBB's Management Who They Work For

This call and webcast ended a little while ago. David Einhorn did a very good job of explaining his idea behind ingeniously named iPrefs, only slightly marred by the brain dead questioners who began the Q&A segment. We think the theme of perpetual preferreds is applicable to many companies including tech names such as Microsoft (MSFT) about which I wrote last week. Einhorn’s suggestion highlights the still unmet demand for yield. We certainly hope MSFT takes note but it’s an interesting theme for other companies to consider as well.

https://sl-advisors.com/wp-content/uploads/2013/04/logo1.jpg00Simon Lackhttps://sl-advisors.com/wp-content/uploads/2013/04/logo1.jpgSimon Lack2013-02-21 17:40:532013-02-21 17:40:53David Einhorn's Conference Call on Apple

This morning David Einhorn on CNBC elegantly highlighted the inconsistency in pricing of different asset classes, specifically in the case of Apple (AAPL), which he owns. Einhorn believes AAPL should exploit the low yields/high prices of preferred equity to the advantage of stockholders.

You can read the transcript of Einhorn’s interview here so we won’t repeat what he said. We don’t own AAPL, but his suggestion isn’t limited to them. In fact, any company with a strong balance sheet, predictable earnings and a low P/E could avail itself of the same strategy.

So we’ve applied it to Microsoft (MSFT), another tech giant that we believe is attractively priced. The basic concept is for the company to distribute preferred equity shares to existing shareholders. No cash would change hands; each shareholder would just receive preferred shares proportionate to their shareholdings. But even though no cash has changed hands, we believe it illustrates how value would be unlocked.

Here’s how it works (my colleague Henry Hoffman crunched the numbers for this example): MSFT has 8.4 billion shares outstanding for a market cap of $228 BN. It has $43BN of cash net of debt (further assuming a 20% haircut to repatriate the cash from outside the U.S.). So the whole company is priced at $185BN ($228BN-$43BN). MSFT pays a quarterly dividend of $0.23, which costs $7.8BN annually. Suppose the company diverted this dividend fully to pay dividends on the preferred shares, which are all owned by existing stockholders. Assuming a 4% yield on these preferreds would value them at $195BN (7.8 divided by 0.04). So the shareholders would own new securities of this approximate value which they could keep or sell in the marketplace. But they’d still own the common equity. Consensus expectations are for MSFT to earn $24BN in the fiscal year 2013 (ending in June). MSFT’s P/E is 7.7X (excluding Cash).

Diverting $7.8BN to pay preferred dividends reduces the net income available to common equity to $16.2BN. Assuming the same P/E multiple on these reduced earnings would value the equity at $125BN. Combined with the preferred equity, the shareholders would now own securities worth $320BN. On this basis each common share would be worth $37.86 on the day MSFT announced its intention to distribute preferred equity securities to every holder of common equity.

It wouldn’t alter the leverage of the company because the preferred would count as equity and would sit just above common in the capital structure. It also wouldn’t alter the company’s dividend expense, since the dividends that were being paid on the common have simply been diverted to the preferreds. It would highlight the large disparity between the valuation of common equity, with an earnings yield of almost 13% (inverse of the 7.7 P/E ratio) and the 4% yield on a security that sits immediately above common equity in the capital structure.

The P/E on the common equity might fall following the distribution of the preferred equity, but even in the absurd case of the common equity being worthless (hard to imagine given $16.2BN of FY 2013 earnings) the preferred equity’s value is still higher than today’s market cap (ex-cash).

You can play around with the assumptions endlessly. One we like is to further assume that money spent on stock buybacks is additionally diverted to preferred dividends. Buybacks count as cash returned to shareholders in the same way as dividends. MSFT’s five year average buyback expenditure is $9.9BN. Adding this to dividends of $7.8BN creates a preferred dividend of $17.7BN and a value on this class of securities of $442BN. Net income left to common shareholders in this case would be$6.3BN in FY 2013.

David Einhorn made a clever suggestion. It’s a neat way to illustrate the discrepancy in asset markets between fixed income yields and earnings yields.

We hope Steve Ballmer was watching CNBC this morning.

Disclosure: We are long MSFT

https://sl-advisors.com/wp-content/uploads/2013/04/logo1.jpg00Simon Lackhttps://sl-advisors.com/wp-content/uploads/2013/04/logo1.jpgSimon Lack2013-02-07 13:46:222013-02-07 13:46:22Unlocking Value In Microsoft The Einhorn Way

One opinion shared by many investors nowadays is that stocks are risky, and the near term outlook is especially unclear. Today’s Wall Street Journal profiles a financial adviser in Chicago, Jeffrey Smith, who spends much of his time persuading clients that they should remain in equities in order to achieve their long term investment goals. One client apparently found his mind wandering to Edvard Munch’s painting titled, “Scream” as he contemplated the many potential disasters waiting in the wings. Mr. Smith’s cause can’t be helped by daily headlines from Washington which largely serve to remind investors what a dysfunctional place it is. The very creation of a Fiscal Cliff was ill-considered, representing as it does a totally blunt instrument to control future deficits. While the original intent was to force tough decisions on a reluctant Congress so as to avoid automatic tax hikes and spending cuts, in fact the focus is really just on avoiding its consequences. News reports show that the most likely outcome is higher taxes on the 2%, some spending cuts and no doubt solemn commitments to do the heavy lifting of budgetary discipline next year.

It’s not what was intended but is the best we can expect. Congress created the cliff and Congress can modify it. It’s not really a tool to force action.

In fact, there’s little reason to be long term optimistic on the U.S. fiscal outlook. Opinion polls regularly expose the incongruity of voters’ desires for improved fiscal prudence combined with broadly unaltered tax policies and entitlements. On top of which, while there’s much hand wringing about the future there’s little visible cost to current policies. If Congress and the Administration did miraculously come together on a meaningful plan to achieve annual deficits of 2.5% of GDP (thought by many to be a long term sustainable target) bond yields could hardly fall very far in response. When Clinton raised taxes in the 90s to reduce the deficit interest rates fell and softened the blow somewhat. No such payback is likely today. So low expectations on this issue are appropriate.

Nonetheless the Math of equities remains compelling. $22 in the S&P 500 will deliver the same after tax return as ten year treasury notes held to maturity, assuming 4% dividend growth on the former. You can make your own synthetic bond with $78 in 0% yielding cash and $22 in 2% yielding equities. Even a disastrous 50% collapse in stocks would cause an $11 fall in your portfolio value or 11%. It would only take a 1.25% rise in bond yields to cause a similar 11% loss in ten year treasuries.

Choosing the stocks/cash combination with its range of possible outcomes instead of the fairly certain loss of purchasing power through bonds requires a long term perspective. However, that is the most reliable way to maintain the purchasing power of your savings.

Most recently we invested in Dollar General (DG). For some time we’ve followed this company as a comparison to Family Dollar (FDO) which we have owned in the past (although not at present). DG has better sales per square foot, operating margins and growth than FDO, but in recent months its valuation has slipped to where it’s now comparable to FDO. These businesses tend to hold up fairly well during tough economic times and although DG is weaker today following its earnings release we think it represents an attractive investment.

https://sl-advisors.com/wp-content/uploads/2013/04/logo1.jpg00Simon Lackhttps://sl-advisors.com/wp-content/uploads/2013/04/logo1.jpgSimon Lack2012-12-11 12:06:182012-12-11 12:06:18Holding Stocks Without Screaming

This morning’s news that Freeport McMoran is acquiring two E&P businesses (Plains Exploration and McMoran Exploration) is the first real M&A activity since BHP’s acquisition of Petrohawk in the middle of last year. Subsequently BHP had to take significant write downs on their newly acquired assets and the fervor for buying E&P names steadily cooled.

Some names in the sector are relatively attractively priced. Devon Energy (DVN) trades below the price of its proved reserves and is 100% U.S. so no geopolitical risk. At some point they could represent an attractive way to supplement depleting energy reserves for one of the major integrated oil companies. Range Resources (RRC) has also been weak lately and offers some significant upside if they can successfuly extract a good percentage of their 50 Trillion Cubic Feet Equivalent (TCFE) of potential natural gas reserves. Comstock Resources (CRK) is also at the low end of its recent range. With a market cap of less than $1BN it would be an easy acquisition for many big companies. The 25% short interest in CRK also reveals some healthy skepticism.

We are long DVN, RRC and CRK.

https://sl-advisors.com/wp-content/uploads/2013/04/logo1.jpg00Simon Lackhttps://sl-advisors.com/wp-content/uploads/2013/04/logo1.jpgSimon Lack2012-12-05 11:17:332012-12-05 11:17:33Freeport McMoran Returns to the Oil Business

By clicking the OK button below, you will be connected to a website maintained by a third party. We are providing a link to the third party’s website solely as a convenience to you, because we believe that website may provide useful content. We do not control the content on the third-party website; we do not guarantee any claims made on it; nor do we endorse the website, its sponsor, or any of the content, policies, activities, products or services offered on the website or by any advertiser on the site. We disclaim any responsibility for the website’s performance or interaction with your computer, its security and privacy policies and practices, and any consequences that may result from visiting it. The link is not intended to create an offer to sell, recommend, or a solicitation of an offer to buy or hold, any securities.

By clicking the OK button below, you will be connected to a website maintained by a third party. We are providing a link to the third party’s website solely as a convenience to you, because we believe that website may provide useful content. We do not control the content on the third-party website; we do not guarantee any claims made on it; nor do we endorse the website, its sponsor, or any of the content, policies, activities, products or services offered on the website or by any advertiser on the site. We disclaim any responsibility for the website’s performance or interaction with your computer, its security and privacy policies and practices, and any consequences that may result from visiting it. The link is not intended to create an offer to sell, recommend, or a solicitation of an offer to buy or hold, any securities.

By clicking the OK button below, you will be connected to a website maintained by a third party. We are providing a link to the third party’s website solely as a convenience to you, because we believe that website may provide useful content. We do not control the content on the third-party website; we do not guarantee any claims made on it; nor do we endorse the website, its sponsor, or any of the content, policies, activities, products or services offered on the website or by any advertiser on the site. We disclaim any responsibility for the website’s performance or interaction with your computer, its security and privacy policies and practices, and any consequences that may result from visiting it. The link is not intended to create an offer to sell, recommend, or a solicitation of an offer to buy or hold, any securities.

By clicking the OK button below, you will be connected to a website maintained by a third party. We are providing a link to the third party’s website solely as a convenience to you, because we believe that website may provide useful content. We do not control the content on the third-party website; we do not guarantee any claims made on it; nor do we endorse the website, its sponsor, or any of the content, policies, activities, products or services offered on the website or by any advertiser on the site. We disclaim any responsibility for the website’s performance or interaction with your computer, its security and privacy policies and practices, and any consequences that may result from visiting it. The link is not intended to create an offer to sell, recommend, or a solicitation of an offer to buy or hold, any securities.

By clicking the OK button below, you will be connected to a website maintained by a third party. We are providing a link to the third party’s website solely as a convenience to you, because we believe that website may provide useful content. We do not control the content on the third-party website; we do not guarantee any claims made on it; nor do we endorse the website, its sponsor, or any of the content, policies, activities, products or services offered on the website or by any advertiser on the site. We disclaim any responsibility for the website’s performance or interaction with your computer, its security and privacy policies and practices, and any consequences that may result from visiting it. The link is not intended to create an offer to sell, recommend, or a solicitation of an offer to buy or hold, any securities.